What is Global Aluminum Counterflow Heat Exchanger Market?

The Global Aluminum Counterflow Heat Exchanger Market refers to the worldwide industry focused on the production, distribution, and utilization of aluminum counterflow heat exchangers. These devices are essential in various applications where heat transfer is required, such as in HVAC systems, industrial processes, and automotive industries. Aluminum counterflow heat exchangers are preferred due to their high thermal conductivity, lightweight nature, and resistance to corrosion. They work by allowing two fluids to flow in opposite directions, thereby maximizing the heat exchange efficiency. The market encompasses a wide range of products, from small-scale units used in residential settings to large industrial systems. The demand for these heat exchangers is driven by the need for energy-efficient solutions and the growing emphasis on reducing carbon footprints across different sectors. As industries continue to seek ways to optimize energy use and enhance system performance, the Global Aluminum Counterflow Heat Exchanger Market is expected to see significant growth.

Area below 0.1 Sq.m, Area 0.1-0.2 Sq.m, Area 0.2-0.5 Sq.m, Area above 0.5 Sq.m in the Global Aluminum Counterflow Heat Exchanger Market:

In the Global Aluminum Counterflow Heat Exchanger Market, products are categorized based on their surface area, which directly impacts their heat exchange capacity. The first category includes heat exchangers with an area below 0.1 square meters. These are typically used in small-scale applications where space is limited, such as in residential HVAC systems or compact industrial equipment. Despite their small size, they are highly efficient and can handle significant heat loads relative to their surface area. The next category, with an area between 0.1 and 0.2 square meters, is often found in medium-sized applications. These units strike a balance between size and performance, making them suitable for commercial buildings and mid-sized industrial processes. They offer enhanced heat transfer capabilities while still being relatively compact. Moving up, heat exchangers with an area between 0.2 and 0.5 square meters are designed for larger applications. These are commonly used in large commercial buildings, extensive industrial processes, and even some automotive applications. Their larger surface area allows for greater heat exchange, making them ideal for systems that require substantial thermal management. Finally, heat exchangers with an area above 0.5 square meters are used in the most demanding applications. These include large industrial plants, power generation facilities, and extensive HVAC systems in large commercial complexes. Their vast surface area enables them to handle extremely high heat loads, ensuring efficient thermal management even in the most challenging environments. Each category of heat exchanger plays a crucial role in its respective application, contributing to the overall efficiency and performance of the systems they are integrated into.

Commercial and Residential, Industrial in the Global Aluminum Counterflow Heat Exchanger Market:

The usage of Global Aluminum Counterflow Heat Exchangers spans across various sectors, including commercial, residential, and industrial applications. In commercial and residential settings, these heat exchangers are primarily used in HVAC systems to regulate indoor temperatures efficiently. They help in maintaining a comfortable environment by transferring heat between the incoming and outgoing air streams, thereby reducing the energy required for heating or cooling. This not only enhances energy efficiency but also contributes to lower utility bills and a reduced carbon footprint. In residential buildings, smaller units are often installed in individual HVAC systems, while larger commercial buildings may use more extensive systems to manage the thermal needs of the entire structure. In the industrial sector, aluminum counterflow heat exchangers are used in a variety of processes that require precise temperature control. They are essential in industries such as chemical processing, power generation, and manufacturing, where maintaining optimal temperatures is crucial for both safety and efficiency. For instance, in chemical plants, these heat exchangers help in controlling the temperature of reactants and products, ensuring that reactions occur under optimal conditions. In power plants, they are used to manage the heat generated during electricity production, improving overall efficiency and reducing waste. Additionally, in manufacturing, they help in cooling machinery and equipment, preventing overheating and ensuring smooth operations. The versatility and efficiency of aluminum counterflow heat exchangers make them indispensable in both commercial and industrial applications, driving their demand across various sectors.

Global Aluminum Counterflow Heat Exchanger Market Outlook:

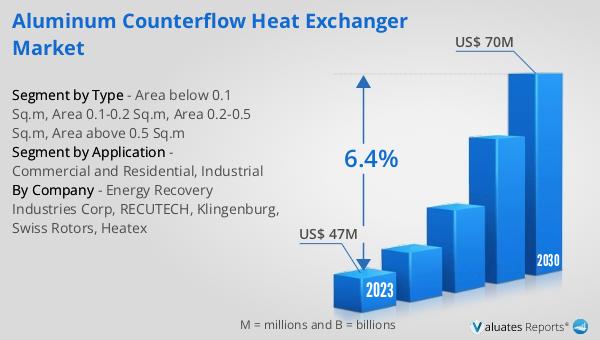

The global Aluminum Counterflow Heat Exchanger market was valued at US$ 47 million in 2023 and is anticipated to reach US$ 70 million by 2030, witnessing a CAGR of 6.4% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for energy-efficient solutions and the need to reduce carbon emissions across various industries. The market's expansion is also supported by advancements in technology, which have led to the development of more efficient and durable heat exchangers. As industries continue to prioritize sustainability and energy efficiency, the demand for aluminum counterflow heat exchangers is expected to rise. These devices play a crucial role in optimizing energy use and enhancing system performance, making them a valuable asset in both commercial and industrial applications. The projected growth of the market reflects the ongoing efforts to improve energy efficiency and reduce environmental impact, highlighting the importance of aluminum counterflow heat exchangers in achieving these goals.

| Report Metric | Details |

| Report Name | Aluminum Counterflow Heat Exchanger Market |

| Accounted market size in 2023 | US$ 47 million |

| Forecasted market size in 2030 | US$ 70 million |

| CAGR | 6.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Energy Recovery Industries Corp, RECUTECH, Klingenburg, Swiss Rotors, Heatex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |