What is Global Paint Test Equipment Market?

The Global Paint Test Equipment Market is a specialized segment within the broader testing and measurement industry, focusing on tools and devices used to evaluate the quality and performance of paint and coatings. These instruments are essential for ensuring that paints meet specific standards and perform as expected in various applications. The market encompasses a wide range of equipment, including devices for measuring paint thickness, adhesion, gloss, and color consistency. These tools are used across multiple industries, such as automotive, aerospace, construction, and manufacturing, to ensure that painted surfaces are durable, aesthetically pleasing, and compliant with regulatory standards. The market is driven by the increasing demand for high-quality finishes and the need for compliance with stringent industry regulations. Technological advancements have also played a significant role in the market's growth, with modern paint test equipment offering greater accuracy, ease of use, and advanced features like digital readouts and data logging capabilities. As industries continue to prioritize quality and compliance, the demand for reliable paint test equipment is expected to remain strong.

Visual Test Equipment, Optical Test Equipment, Electronic Test Equipment in the Global Paint Test Equipment Market:

Visual Test Equipment, Optical Test Equipment, and Electronic Test Equipment are three primary categories within the Global Paint Test Equipment Market, each serving distinct functions but collectively ensuring comprehensive paint quality assessment. Visual Test Equipment includes tools like magnifying glasses, microscopes, and visual inspection booths that allow inspectors to examine paint surfaces for defects such as bubbles, cracks, or uneven application. These tools are crucial for identifying visible flaws that could affect the aesthetic and functional quality of the paint job. Optical Test Equipment, on the other hand, involves more sophisticated devices like spectrophotometers, gloss meters, and colorimeters. These instruments measure the optical properties of paint, such as color consistency, gloss level, and transparency. Spectrophotometers, for instance, can analyze the color of paint with high precision, ensuring that it matches the desired specifications. Gloss meters measure the shine or luster of a painted surface, which is particularly important in industries like automotive and consumer electronics where appearance is critical. Electronic Test Equipment includes devices like thickness gauges, adhesion testers, and hardness testers. Thickness gauges measure the thickness of paint layers to ensure they meet specified standards, which is vital for both protective and aesthetic purposes. Adhesion testers evaluate how well the paint adheres to the substrate, which is crucial for durability and longevity. Hardness testers assess the paint's resistance to scratching and wear, providing insights into its durability under various conditions. Together, these categories of test equipment provide a comprehensive toolkit for assessing the quality and performance of paint, ensuring that it meets the required standards and performs as expected in its intended application.

Construction, Automobile, Aerospace in the Global Paint Test Equipment Market:

The usage of Global Paint Test Equipment Market spans several critical industries, including construction, automobile, and aerospace, each with unique requirements and standards for paint quality. In the construction industry, paint test equipment is used to ensure that coatings on buildings and infrastructure are durable, weather-resistant, and aesthetically pleasing. For instance, thickness gauges and adhesion testers are commonly used to verify that paint layers are applied correctly and adhere well to surfaces, which is essential for long-term durability and protection against environmental factors like moisture and UV radiation. In the automobile industry, paint quality is paramount for both aesthetic and functional reasons. Automakers use a variety of paint test equipment to ensure that vehicle coatings are not only visually appealing but also resistant to scratches, chips, and corrosion. Gloss meters and colorimeters are frequently used to maintain consistent color and gloss levels across different parts of a vehicle, while hardness testers and adhesion testers ensure that the paint can withstand the rigors of daily use. In the aerospace industry, the stakes are even higher, as paint not only contributes to the appearance of aircraft but also plays a crucial role in protecting against corrosion and reducing drag. Aerospace manufacturers use advanced paint test equipment to ensure that coatings meet stringent performance standards. Thickness gauges, for example, are used to verify that paint layers are applied uniformly, while spectrophotometers ensure that colors meet precise specifications. Adhesion testers and hardness testers are also essential for ensuring that the paint can withstand the extreme conditions encountered during flight. Across these industries, the use of paint test equipment is essential for maintaining high standards of quality and performance, ensuring that painted surfaces are both functional and visually appealing.

Global Paint Test Equipment Market Outlook:

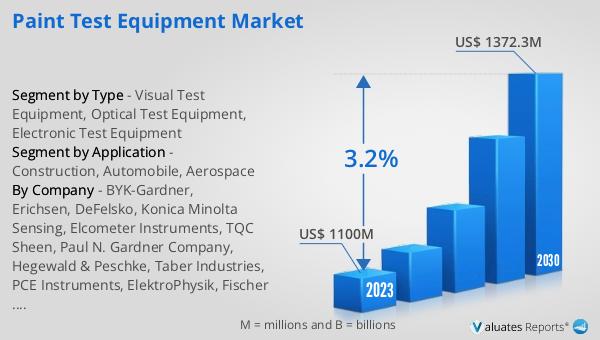

The global Paint Test Equipment market was valued at US$ 1100 million in 2023 and is anticipated to reach US$ 1372.3 million by 2030, witnessing a CAGR of 3.2% during the forecast period 2024-2030. This growth reflects the increasing demand for high-quality paint finishes across various industries, driven by the need for compliance with stringent regulatory standards and the desire for aesthetically pleasing and durable coatings. The market's expansion is also fueled by technological advancements in paint test equipment, which offer greater accuracy, ease of use, and advanced features like digital readouts and data logging capabilities. As industries such as automotive, aerospace, and construction continue to prioritize quality and compliance, the demand for reliable paint test equipment is expected to remain strong. The market's growth trajectory indicates a robust future, with ongoing innovations and increasing adoption of advanced testing tools playing a significant role in shaping its development.

| Report Metric | Details |

| Report Name | Paint Test Equipment Market |

| Accounted market size in 2023 | US$ 1100 million |

| Forecasted market size in 2030 | US$ 1372.3 million |

| CAGR | 3.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | BYK-Gardner, Erichsen, DeFelsko, Konica Minolta Sensing, Elcometer Instruments, TQC Sheen, Paul N. Gardner Company, Hegewald & Peschke, Taber Industries, PCE Instruments, ElektroPhysik, Fischer Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |