What is Global Egg-free Flu Vaccine Market?

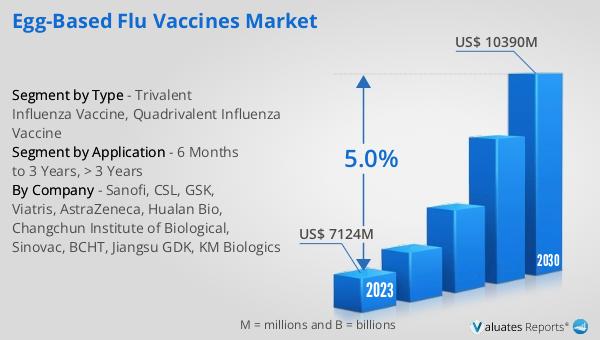

The Global Egg-free Flu Vaccine Market refers to the market for influenza vaccines that are produced without the use of eggs. Traditional flu vaccines are typically grown in chicken eggs, which can be problematic for people with egg allergies and can also be less effective due to the potential for egg-adapted changes in the virus. Egg-free flu vaccines are developed using alternative methods such as cell culture or recombinant DNA technology, which do not involve eggs at any stage of production. These vaccines offer a safer and potentially more effective option for individuals with egg allergies and can also be produced more quickly and efficiently, which is crucial during flu pandemics. The market for these vaccines is growing as awareness of their benefits increases and as more people seek out alternatives to traditional egg-based vaccines.

Cell Culture-based Flu Vaccine, Recombinant Influenza Vaccine in the Global Egg-free Flu Vaccine Market:

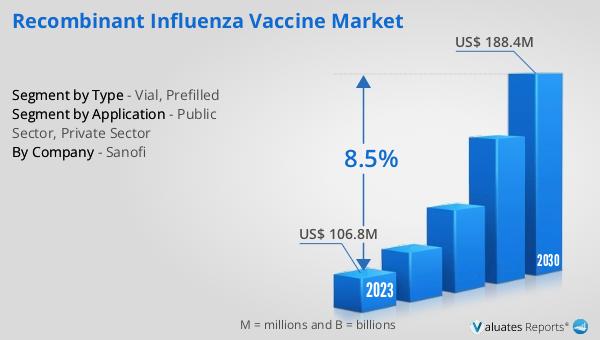

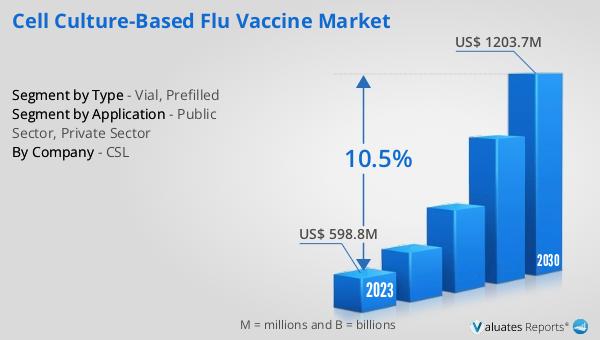

Cell culture-based flu vaccines and recombinant influenza vaccines are two primary types of egg-free flu vaccines that have gained prominence in the Global Egg-free Flu Vaccine Market. Cell culture-based flu vaccines are produced by growing the influenza virus in mammalian cells, such as Madin-Darby Canine Kidney (MDCK) cells, instead of chicken eggs. This method allows for a more controlled and consistent production process, reducing the risk of egg-adapted mutations that can occur with egg-based vaccines. Additionally, cell culture-based vaccines can be produced more rapidly, which is particularly advantageous during a flu pandemic when quick vaccine availability is critical. On the other hand, recombinant influenza vaccines are created using recombinant DNA technology. This involves inserting the gene for a specific influenza virus protein into a different virus or bacterium, which then produces the protein in large quantities. The protein is then purified and used to create the vaccine. Recombinant vaccines do not require the use of live influenza virus or eggs, making them a suitable option for individuals with egg allergies and those seeking a more modern approach to vaccination. Both cell culture-based and recombinant influenza vaccines offer significant advantages over traditional egg-based vaccines, including faster production times, reduced risk of allergic reactions, and potentially higher efficacy. As the demand for safer and more effective flu vaccines continues to grow, the Global Egg-free Flu Vaccine Market is expected to expand, with these innovative vaccine types playing a crucial role in meeting the needs of diverse populations.

Public Sector, Private Sector in the Global Egg-free Flu Vaccine Market:

The usage of egg-free flu vaccines in the Global Egg-free Flu Vaccine Market spans both the public and private sectors, each with its unique applications and benefits. In the public sector, egg-free flu vaccines are often utilized in government-funded vaccination programs aimed at protecting public health. These programs prioritize vulnerable populations, such as the elderly, young children, and individuals with chronic health conditions, who are at higher risk of severe influenza complications. By incorporating egg-free flu vaccines into these programs, governments can ensure that individuals with egg allergies are not excluded from receiving essential flu protection. Additionally, the rapid production capabilities of cell culture-based and recombinant vaccines make them valuable assets during flu pandemics, enabling governments to respond swiftly to emerging threats. In the private sector, egg-free flu vaccines are increasingly being adopted by healthcare providers, employers, and private health organizations. Healthcare providers, including hospitals and clinics, offer these vaccines to patients who may have egg allergies or prefer egg-free options. Employers, particularly those in industries with high employee interaction, such as healthcare, education, and retail, may provide egg-free flu vaccines as part of workplace wellness programs to reduce absenteeism and maintain a healthy workforce. Private health organizations, including pharmacies and urgent care centers, also play a role in distributing egg-free flu vaccines to the general public, making them accessible to a broader audience. The collaboration between public and private sectors in promoting and distributing egg-free flu vaccines is essential for maximizing their impact and ensuring that all individuals, regardless of their allergy status, have access to effective flu protection.

Global Egg-free Flu Vaccine Market Outlook:

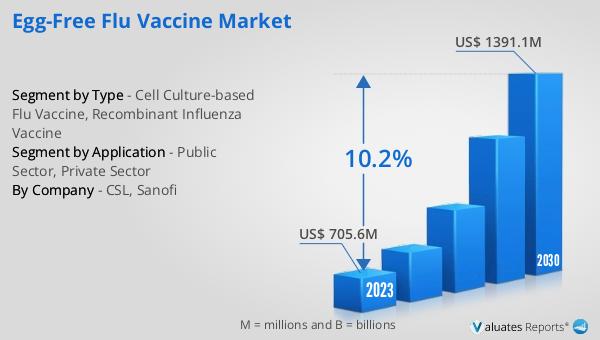

The global Egg-free Flu Vaccine market was valued at US$ 705.6 million in 2023 and is anticipated to reach US$ 1391.1 million by 2030, witnessing a CAGR of 10.2% during the forecast period 2024-2030. This significant growth reflects the increasing demand for safer and more effective flu vaccines that do not rely on eggs for production. The rising awareness of egg allergies and the limitations of traditional egg-based vaccines have driven the adoption of egg-free alternatives. Additionally, the advantages of cell culture-based and recombinant influenza vaccines, such as faster production times and reduced risk of allergic reactions, have contributed to their growing popularity. As the market continues to expand, it is expected that more healthcare providers, governments, and private organizations will incorporate egg-free flu vaccines into their vaccination programs, further driving market growth. The projected increase in market value underscores the importance of continued innovation and investment in egg-free flu vaccine technologies to meet the evolving needs of global populations.

| Report Metric | Details |

| Report Name | Egg-free Flu Vaccine Market |

| Accounted market size in 2023 | US$ 705.6 million |

| Forecasted market size in 2030 | US$ 1391.1 million |

| CAGR | 10.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | CSL, Sanofi |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |