What is Global Sata Portable SSD Market?

The Global SATA Portable SSD Market refers to the worldwide industry focused on the production, distribution, and sale of portable solid-state drives (SSDs) that use the SATA (Serial ATA) interface. These devices are known for their high-speed data transfer capabilities, durability, and compact size, making them a popular choice for both personal and professional use. Unlike traditional hard drives, SSDs have no moving parts, which significantly reduces the risk of mechanical failure and enhances performance. The market encompasses a wide range of products, from entry-level models to high-end versions designed for intensive applications. Factors driving the growth of this market include the increasing demand for faster data storage solutions, the growing need for reliable and portable storage devices, and advancements in SSD technology. As more consumers and businesses recognize the benefits of SATA portable SSDs, the market is expected to continue expanding, offering new opportunities for manufacturers and retailers alike.

<500 GB, 500GB-1TB, >1TB in the Global Sata Portable SSD Market:

In the Global SATA Portable SSD Market, storage capacities are typically categorized into three main segments: less than 500 GB, 500 GB to 1 TB, and greater than 1 TB. Each of these segments caters to different user needs and preferences. SSDs with less than 500 GB of storage are generally aimed at casual users who need a reliable and fast storage solution for everyday tasks such as storing documents, photos, and small applications. These drives are often more affordable, making them an attractive option for budget-conscious consumers. On the other hand, SSDs with storage capacities ranging from 500 GB to 1 TB are designed for users who require more space for larger files, such as high-resolution videos, extensive photo libraries, and more demanding software applications. This segment is popular among professionals and enthusiasts who need a balance between storage capacity and performance. Finally, SSDs with capacities greater than 1 TB are targeted at power users, including gamers, video editors, and enterprise users who need substantial storage for large datasets, complex applications, and high-performance computing tasks. These high-capacity SSDs offer the best performance and reliability, making them ideal for intensive use cases. As technology continues to advance, the cost of higher-capacity SSDs is expected to decrease, making them more accessible to a broader range of users. Each segment of the SATA portable SSD market plays a crucial role in meeting the diverse storage needs of consumers and businesses, driving the overall growth and development of the market.

Enterprise, Personal in the Global Sata Portable SSD Market:

The usage of Global SATA Portable SSDs varies significantly between enterprise and personal applications, each with its unique requirements and benefits. In the enterprise sector, SATA portable SSDs are invaluable for their speed, reliability, and portability. Businesses use these drives for a variety of purposes, including data backup, disaster recovery, and the transfer of large files between different locations. The high-speed data transfer capabilities of SSDs enable enterprises to quickly access and move critical data, which is essential for maintaining operational efficiency and minimizing downtime. Additionally, the durability and reliability of SSDs make them a preferred choice for storing sensitive and important business data, as they are less prone to failure compared to traditional hard drives. In personal use, SATA portable SSDs offer a convenient and efficient solution for individuals who need to store and access their data on the go. Whether it's for storing personal documents, photos, music, or videos, these drives provide a fast and reliable way to manage digital content. The compact size and lightweight nature of portable SSDs make them easy to carry, allowing users to take their data with them wherever they go. Moreover, the plug-and-play functionality of these drives ensures that they can be easily connected to various devices, such as laptops, desktops, and gaming consoles, without the need for additional software or drivers. This versatility makes SATA portable SSDs a popular choice among tech-savvy consumers who value performance and convenience. Overall, the widespread adoption of SATA portable SSDs in both enterprise and personal applications highlights their importance in today's digital age, where fast and reliable data storage solutions are essential for both work and leisure.

Global Sata Portable SSD Market Outlook:

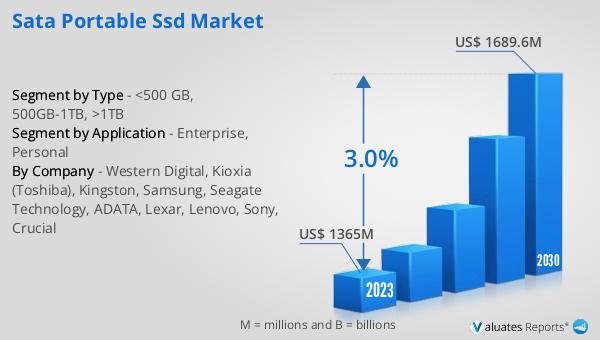

The global SATA Portable SSD market was valued at US$ 1365 million in 2023 and is anticipated to reach US$ 1689.6 million by 2030, witnessing a CAGR of 3.0% during the forecast period from 2024 to 2030. This market outlook indicates a steady growth trajectory for the industry, driven by increasing demand for high-speed, reliable, and portable data storage solutions. The projected growth reflects the expanding adoption of SATA portable SSDs across various sectors, including enterprise and personal use. As more consumers and businesses recognize the benefits of these devices, such as faster data transfer speeds, enhanced durability, and compact design, the market is expected to continue its upward trend. The anticipated increase in market value also suggests that manufacturers and retailers will have ample opportunities to innovate and introduce new products that cater to the evolving needs of users. Overall, the positive market outlook underscores the growing importance of SATA portable SSDs in the global data storage landscape.

| Report Metric | Details |

| Report Name | Sata Portable SSD Market |

| Accounted market size in 2023 | US$ 1365 million |

| Forecasted market size in 2030 | US$ 1689.6 million |

| CAGR | 3.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Western Digital, Kioxia (Toshiba), Kingston, Samsung, Seagate Technology, ADATA, Lexar, Lenovo, Sony, Crucial |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |