What is Global Fire Proof Medium Density Fiberboard Market?

The Global Fire Proof Medium Density Fiberboard (MDF) Market is a specialized segment within the broader MDF market, focusing on products that offer enhanced fire resistance. MDF is a type of engineered wood product made by breaking down hardwood or softwood residuals into wood fibers, combining it with wax and a resin binder, and forming panels by applying high temperature and pressure. Fireproof MDF is treated with fire-retardant chemicals to improve its resistance to ignition and slow the spread of flames. This makes it an ideal choice for applications where fire safety is a critical concern. The market for fireproof MDF is driven by stringent building codes and regulations, increasing awareness about fire safety, and the growing demand for safer building materials in both residential and commercial construction. The market is also influenced by advancements in fire-retardant technologies and the development of new, more effective fireproofing treatments. As a result, the Global Fire Proof Medium Density Fiberboard Market is expected to see significant growth in the coming years, driven by these factors and the increasing adoption of fireproof MDF in various applications.

<10mm, 10-20mm, >20mm in the Global Fire Proof Medium Density Fiberboard Market:

In the Global Fire Proof Medium Density Fiberboard Market, the product is categorized based on thickness into three main segments: less than 10mm, 10-20mm, and greater than 20mm. Each of these categories serves different purposes and meets various industry requirements. MDF boards with a thickness of less than 10mm are typically used in applications where lightweight and flexibility are crucial. These thinner boards are often employed in the production of lightweight furniture, decorative panels, and other applications where ease of handling and installation are important. Despite their thinness, these boards still offer significant fire resistance, making them suitable for use in environments where fire safety is a concern. The 10-20mm thickness range is the most commonly used in the market, offering a balance between strength, durability, and fire resistance. These boards are widely used in the construction industry for wall paneling, partitions, and other structural applications. They are also popular in the furniture industry for making cabinets, shelves, and other sturdy furniture pieces. The fireproof properties of these boards make them an ideal choice for use in public buildings, schools, hospitals, and other places where fire safety regulations are stringent. Boards with a thickness greater than 20mm are used in heavy-duty applications where maximum strength and durability are required. These thick boards are often used in the construction of load-bearing structures, industrial applications, and other areas where high mechanical strength is necessary. The fireproof nature of these boards adds an extra layer of safety, making them suitable for use in high-risk environments such as factories, warehouses, and other industrial settings. In summary, the Global Fire Proof Medium Density Fiberboard Market offers a range of products with varying thicknesses to meet the diverse needs of different industries. Each thickness category has its unique advantages and applications, making fireproof MDF a versatile and valuable material in the market.

Furniture Industry, Building Materials, Interior Decoration, Others in the Global Fire Proof Medium Density Fiberboard Market:

The usage of Global Fire Proof Medium Density Fiberboard (MDF) spans across various industries, including the furniture industry, building materials, interior decoration, and others. In the furniture industry, fireproof MDF is highly valued for its combination of fire resistance, strength, and versatility. It is used to manufacture a wide range of furniture items such as cabinets, shelves, tables, and chairs. The fireproof properties of MDF provide an added layer of safety, making it an ideal choice for furniture used in public spaces, schools, hospitals, and other areas where fire safety is a priority. Additionally, fireproof MDF can be easily machined and finished, allowing for the creation of aesthetically pleasing and functional furniture pieces. In the realm of building materials, fireproof MDF is extensively used for wall paneling, partitions, and ceiling tiles. Its fire-resistant properties make it a preferred choice for constructing fire-rated walls and ceilings in residential, commercial, and industrial buildings. The use of fireproof MDF in building materials helps to enhance the overall fire safety of structures, providing occupants with more time to evacuate in the event of a fire. Moreover, fireproof MDF is often used in the construction of doors and windows, offering an additional layer of protection against fire spread. Interior decoration is another area where fireproof MDF finds significant application. It is used to create decorative wall panels, moldings, and trims that not only enhance the aesthetic appeal of interiors but also contribute to fire safety. Fireproof MDF can be easily painted, laminated, or veneered, allowing for a wide range of design possibilities. This makes it a popular choice for interior designers and architects who seek to combine safety with style. In addition to the above-mentioned areas, fireproof MDF is also used in various other applications. For instance, it is employed in the production of acoustic panels, which are used in theaters, auditoriums, and recording studios to improve sound quality while ensuring fire safety. Fireproof MDF is also used in the manufacturing of signage, exhibition displays, and other custom-made products where fire resistance is a critical requirement. Overall, the versatility and fire-resistant properties of MDF make it a valuable material across multiple industries, contributing to enhanced safety and functionality in various applications.

Global Fire Proof Medium Density Fiberboard Market Outlook:

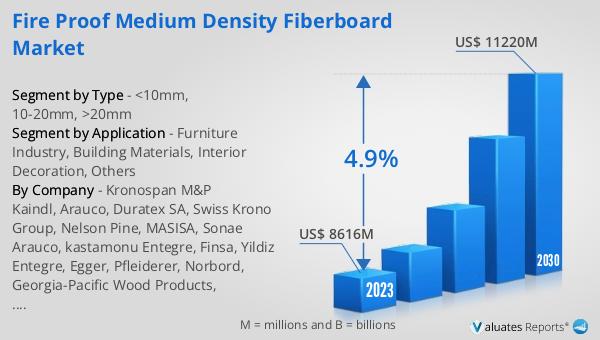

The global Fire Proof Medium Density Fiberboard market was valued at US$ 8616 million in 2023 and is anticipated to reach US$ 11220 million by 2030, witnessing a CAGR of 4.9% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by increasing demand for fire-resistant building materials across various industries. The rising awareness about fire safety, coupled with stringent building codes and regulations, is expected to fuel the demand for fireproof MDF in the coming years. The market's growth is also supported by advancements in fire-retardant technologies and the development of new, more effective fireproofing treatments. As a result, the Global Fire Proof Medium Density Fiberboard Market is poised for significant growth, with a projected increase in market value over the forecast period.

| Report Metric | Details |

| Report Name | Fire Proof Medium Density Fiberboard Market |

| Accounted market size in 2023 | US$ 8616 million |

| Forecasted market size in 2030 | US$ 11220 million |

| CAGR | 4.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Kronospan M&P Kaindl, Arauco, Duratex SA, Swiss Krono Group, Nelson Pine, MASISA, Sonae Arauco, kastamonu Entegre, Finsa, Yildiz Entegre, Egger, Pfleiderer, Norbord, Georgia-Pacific Wood Products, Swedspan, Dongwha, Yonglin Group, Furen Group, DareGlobal Wood, Quanyou |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |