What is Global Smart Wireless Mouse Market?

The Global Smart Wireless Mouse Market refers to the worldwide industry focused on the production, distribution, and sale of smart wireless mice. These devices are advanced versions of traditional computer mice, featuring wireless connectivity and often incorporating additional smart features such as customizable buttons, ergonomic designs, and enhanced sensitivity for better precision. The market encompasses various types of wireless mice, including those that use Bluetooth technology and those that operate on a 2.4G wireless frequency. The demand for smart wireless mice is driven by the increasing need for convenience and efficiency in both professional and personal computing environments. As more people work remotely and engage in digital activities, the adoption of smart wireless mice is expected to grow. This market includes a wide range of products catering to different user preferences and requirements, from basic models for everyday use to high-end versions designed for gaming and professional applications. The global reach of this market means that manufacturers and retailers must consider diverse consumer needs and preferences across different regions.

Wireless 2.4G, Bluetooth in the Global Smart Wireless Mouse Market:

Wireless 2.4G and Bluetooth technologies are pivotal in the Global Smart Wireless Mouse Market, each offering unique advantages that cater to different user needs. Wireless 2.4G technology operates on a 2.4 GHz frequency, providing a stable and reliable connection with minimal interference. This technology is particularly favored for its low latency, making it ideal for gaming and other high-precision tasks where immediate response times are crucial. Users appreciate the plug-and-play nature of 2.4G wireless mice, which typically come with a USB receiver that can be easily connected to a computer. This simplicity and reliability make 2.4G wireless mice a popular choice for both casual and professional users. On the other hand, Bluetooth technology offers the advantage of not requiring a dedicated USB receiver, freeing up USB ports for other devices. Bluetooth mice can connect directly to any Bluetooth-enabled device, making them highly versatile and convenient for users who switch between multiple devices, such as laptops, tablets, and smartphones. This flexibility is particularly beneficial in modern work environments where mobility and multi-device usage are common. Bluetooth mice also tend to have longer battery life compared to their 2.4G counterparts, as Bluetooth technology is designed to be more energy-efficient. However, Bluetooth connections can sometimes be less stable and have higher latency compared to 2.4G, which might be a consideration for users engaged in activities requiring high precision. Despite these differences, both technologies have their place in the market, and many manufacturers offer models that support both 2.4G and Bluetooth connectivity, giving users the best of both worlds. The choice between 2.4G and Bluetooth ultimately depends on the specific needs and preferences of the user, whether they prioritize low latency and simplicity or versatility and energy efficiency. As the Global Smart Wireless Mouse Market continues to evolve, advancements in both 2.4G and Bluetooth technologies are expected to further enhance the performance and user experience of these devices.

Online Sales, Offline Sales in the Global Smart Wireless Mouse Market:

The usage of smart wireless mice in the Global Smart Wireless Mouse Market spans both online and offline sales channels, each with its unique dynamics and consumer behaviors. Online sales have become increasingly significant, driven by the convenience and wide selection available to consumers. E-commerce platforms like Amazon, eBay, and specialized tech retailers offer a vast array of smart wireless mice, allowing consumers to compare features, prices, and reviews before making a purchase. The online sales channel also benefits from targeted advertising and personalized recommendations, which can help consumers discover products that best meet their needs. Additionally, online sales often feature promotions and discounts that can attract price-sensitive buyers. The ability to shop from the comfort of one's home and have products delivered directly to the doorstep is a major advantage, especially in the current era where remote work and digital lifestyles are prevalent. On the other hand, offline sales channels, such as brick-and-mortar electronics stores, provide a tactile shopping experience that many consumers still value. In physical stores, customers can try out different models, assess the ergonomics, and get a feel for the build quality of the mice before making a purchase. This hands-on experience can be crucial for consumers who prioritize comfort and usability, especially for devices they will use extensively. Moreover, offline sales channels often have knowledgeable staff who can offer personalized advice and recommendations, enhancing the shopping experience. Retailers may also offer in-store promotions and bundle deals that can be appealing to shoppers. Despite the rise of online shopping, offline sales remain a significant part of the market, particularly in regions where internet penetration is lower, or consumers prefer traditional shopping methods. Both online and offline sales channels play a complementary role in the Global Smart Wireless Mouse Market, catering to different consumer preferences and ensuring that a wide range of products is accessible to a diverse audience. As the market continues to grow, the integration of online and offline strategies, such as click-and-collect services and omnichannel marketing, is likely to become more prevalent, providing consumers with even more flexibility and convenience in their purchasing decisions.

Global Smart Wireless Mouse Market Outlook:

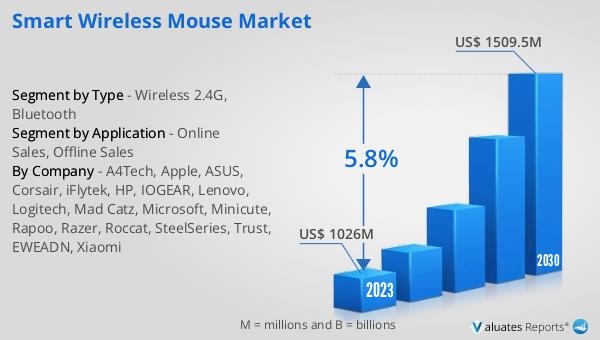

The global Smart Wireless Mouse market was valued at US$ 1026 million in 2023 and is anticipated to reach US$ 1509.5 million by 2030, witnessing a CAGR of 5.8% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the smart wireless mouse industry, driven by increasing demand for advanced computing peripherals. The projected growth reflects the rising adoption of smart wireless mice across various sectors, including gaming, professional workspaces, and personal use. The market's expansion is also supported by technological advancements in wireless connectivity and ergonomic design, which enhance user experience and functionality. As consumers continue to seek more efficient and convenient computing solutions, the smart wireless mouse market is poised to capitalize on these trends. The anticipated growth underscores the importance of innovation and adaptability in meeting evolving consumer needs and preferences. Manufacturers and retailers in this market must stay attuned to these trends to remain competitive and capture a larger share of the growing market.

| Report Metric | Details |

| Report Name | Smart Wireless Mouse Market |

| Accounted market size in 2023 | US$ 1026 million |

| Forecasted market size in 2030 | US$ 1509.5 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | A4Tech, Apple, ASUS, Corsair, iFlytek, HP, IOGEAR, Lenovo, Logitech, Mad Catz, Microsoft, Minicute, Rapoo, Razer, Roccat, SteelSeries, Trust, EWEADN, Xiaomi |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |