What is Global Neomycin Sulfate API Market?

The Global Neomycin Sulfate API Market refers to the worldwide trade and utilization of Neomycin Sulfate, an antibiotic primarily used to treat bacterial infections. Neomycin Sulfate is an aminoglycoside antibiotic that works by inhibiting bacterial protein synthesis, making it effective against a broad spectrum of bacteria. This market encompasses the production, distribution, and application of Neomycin Sulfate in various sectors, including pharmaceuticals, veterinary medicine, and research. The demand for Neomycin Sulfate API is driven by its widespread use in treating infections caused by gram-negative bacteria, particularly in settings where other antibiotics may not be effective. The market is influenced by factors such as regulatory approvals, advancements in antibiotic formulations, and the prevalence of bacterial infections. Additionally, the market dynamics are shaped by the competitive landscape, with numerous pharmaceutical companies involved in the production and distribution of Neomycin Sulfate API. The global reach of this market highlights its significance in addressing bacterial infections and contributing to public health.

Veterinary Use, Human Use in the Global Neomycin Sulfate API Market:

Neomycin Sulfate API is extensively used in both veterinary and human medicine, reflecting its versatility and effectiveness in treating bacterial infections. In veterinary medicine, Neomycin Sulfate is commonly used to treat infections in livestock, pets, and other animals. It is particularly effective against gram-negative bacteria, making it a valuable tool in managing infections in animals. Veterinary formulations of Neomycin Sulfate are available in various forms, including oral solutions, topical ointments, and injectable solutions, allowing for flexible administration depending on the type of infection and the animal being treated. The use of Neomycin Sulfate in veterinary medicine helps maintain the health and productivity of livestock, which is crucial for the agricultural industry. In human medicine, Neomycin Sulfate is used to treat a variety of bacterial infections, particularly those affecting the skin, eyes, and gastrointestinal tract. It is often included in topical ointments and creams for treating skin infections and wounds, as well as in eye drops for ocular infections. Additionally, Neomycin Sulfate is used in combination with other antibiotics to enhance its effectiveness and broaden its spectrum of activity. The use of Neomycin Sulfate in human medicine is regulated by health authorities to ensure its safety and efficacy. Despite its widespread use, it is important to note that Neomycin Sulfate is not effective against all types of bacteria. For instance, Pseudomonas aeruginosa and anaerobic bacteria are resistant to Neomycin Sulfate, limiting its use in certain infections. The development of antibiotic resistance is a significant concern in both veterinary and human medicine, necessitating the prudent use of Neomycin Sulfate to minimize the risk of resistance. Overall, the use of Neomycin Sulfate API in veterinary and human medicine underscores its importance in managing bacterial infections and supporting public health.

Biopharmaceutical, Research in the Global Neomycin Sulfate API Market:

In the biopharmaceutical industry, Neomycin Sulfate API plays a crucial role in the development and production of various pharmaceutical products. It is used as an active ingredient in the formulation of antibiotics, particularly those intended for topical and ophthalmic applications. The ability of Neomycin Sulfate to effectively target gram-negative bacteria makes it a valuable component in the treatment of skin infections, eye infections, and other localized bacterial infections. Biopharmaceutical companies leverage the properties of Neomycin Sulfate to develop products that address specific medical needs, ensuring that patients receive effective and targeted treatments. Additionally, Neomycin Sulfate is used in the production of combination antibiotic therapies, where it is paired with other antibiotics to enhance the overall efficacy and broaden the spectrum of activity. This approach is particularly useful in treating infections caused by multiple bacterial strains or those that are resistant to single antibiotics. In the research sector, Neomycin Sulfate API is utilized in various scientific studies and experiments. It is commonly used in microbiology and molecular biology research to study bacterial resistance mechanisms, antibiotic efficacy, and the genetic basis of bacterial infections. Researchers use Neomycin Sulfate to create selective environments that allow for the growth of specific bacterial strains while inhibiting others, facilitating the study of bacterial behavior and interactions. Furthermore, Neomycin Sulfate is used in genetic engineering and biotechnology applications, where it serves as a selective agent in the development of genetically modified organisms (GMOs). By incorporating Neomycin resistance genes into the genetic material of organisms, researchers can identify and isolate successfully modified cells, advancing the field of genetic research. The use of Neomycin Sulfate in both biopharmaceutical and research settings highlights its versatility and importance in advancing medical science and improving public health outcomes.

Global Neomycin Sulfate API Market Outlook:

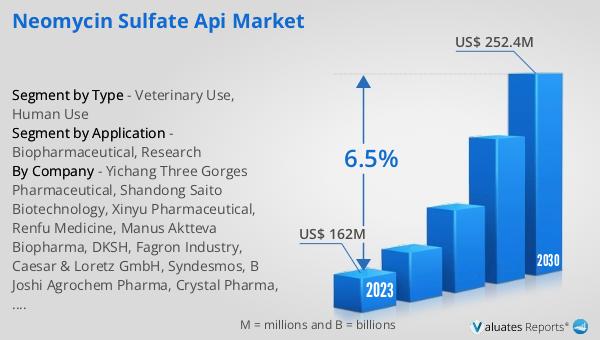

Pseudomonas aeruginosa and anaerobic bacteria are known to be resistant to Neomycin Sulfate, which limits its effectiveness against these types of infections. Despite this limitation, the global Neomycin Sulfate API market has shown significant growth. In 2023, the market was valued at approximately US$ 162 million. Projections indicate that by 2030, the market is expected to reach around US$ 252.4 million, reflecting a compound annual growth rate (CAGR) of 6.5% during the forecast period from 2024 to 2030. This growth can be attributed to the continued demand for effective antibiotics in both human and veterinary medicine, as well as ongoing research and development efforts aimed at improving antibiotic formulations and addressing bacterial resistance. The market's expansion underscores the importance of Neomycin Sulfate in the global healthcare landscape, despite the challenges posed by bacterial resistance.

| Report Metric | Details |

| Report Name | Neomycin Sulfate API Market |

| Accounted market size in 2023 | US$ 162 million |

| Forecasted market size in 2030 | US$ 252.4 million |

| CAGR | 6.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Yichang Three Gorges Pharmaceutical, Shandong Saito Biotechnology, Xinyu Pharmaceutical, Renfu Medicine, Manus Aktteva Biopharma, DKSH, Fagron Industry, Caesar & Loretz GmbH, Syndesmos, B Joshi Agrochem Pharma, Crystal Pharma, Sichuan Long March Pharmaceuticals |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |