What is Global Lipid Microbubble Contrast Agent Market?

The global Lipid Microbubble Contrast Agent market is a specialized segment within the broader medical imaging and diagnostic industry. Lipid microbubble contrast agents are tiny bubbles encapsulated by a lipid shell, used primarily in ultrasound imaging to enhance the clarity and detail of the images. These agents improve the visualization of blood flow and tissue structures, making it easier for healthcare professionals to diagnose and monitor various medical conditions. The market for these agents is driven by the increasing prevalence of chronic diseases, advancements in ultrasound technology, and the growing demand for non-invasive diagnostic procedures. Additionally, the rising geriatric population and the increasing number of diagnostic imaging centers worldwide contribute to the market's growth. The market is characterized by continuous research and development activities aimed at improving the efficacy and safety of these contrast agents. Key players in the market are focusing on strategic collaborations, mergers, and acquisitions to expand their product portfolios and geographical presence. Overall, the global Lipid Microbubble Contrast Agent market is poised for significant growth in the coming years, driven by technological advancements and the increasing need for accurate and efficient diagnostic tools.

Micron, Nanoscale in the Global Lipid Microbubble Contrast Agent Market:

Micron and nanoscale technologies play a crucial role in the development and application of lipid microbubble contrast agents in the global market. Micron-sized lipid microbubbles are typically used in conventional ultrasound imaging due to their ability to enhance image contrast effectively. These microbubbles, usually ranging from 1 to 10 micrometers in diameter, are designed to resonate at specific ultrasound frequencies, thereby improving the visualization of blood vessels and tissue structures. The lipid shell of these microbubbles provides stability and biocompatibility, ensuring that they can circulate in the bloodstream without causing adverse reactions. On the other hand, nanoscale lipid microbubbles, which are smaller than 1 micrometer, are gaining attention for their potential in advanced imaging techniques and targeted drug delivery. These nanoscale agents can penetrate deeper into tissues and provide higher resolution images, making them suitable for detecting early-stage diseases and monitoring treatment responses. Moreover, the smaller size of nanoscale microbubbles allows for better circulation and longer imaging times, which is particularly beneficial in dynamic studies of blood flow and tissue perfusion. The development of both micron and nanoscale lipid microbubble contrast agents involves sophisticated manufacturing processes to ensure uniform size distribution, stability, and functionalization. Researchers are exploring various methods to enhance the targeting capabilities of these agents, such as attaching ligands or antibodies to the lipid shell to bind to specific biomarkers or disease sites. This targeted approach not only improves the diagnostic accuracy but also opens up possibilities for theranostic applications, where the same agent can be used for both diagnosis and therapy. For instance, drug-loaded nanoscale microbubbles can be directed to a tumor site and then burst using focused ultrasound, releasing the therapeutic payload directly at the target. This method minimizes systemic side effects and enhances treatment efficacy. The integration of micron and nanoscale technologies in lipid microbubble contrast agents is also paving the way for personalized medicine. By tailoring the size, composition, and functionalization of these agents to individual patient profiles, healthcare providers can achieve more precise and effective diagnostic and therapeutic outcomes. Furthermore, advancements in imaging modalities, such as high-frequency ultrasound and photoacoustic imaging, are complementing the capabilities of these contrast agents, enabling multi-modal imaging approaches that provide comprehensive insights into disease mechanisms. The global market for lipid microbubble contrast agents is witnessing a surge in demand for both micron and nanoscale products, driven by their diverse applications and the continuous innovation in imaging technologies. Companies operating in this market are investing heavily in research and development to stay ahead of the competition and meet the evolving needs of healthcare professionals. Regulatory approvals and clinical trials play a significant role in the commercialization of these agents, ensuring their safety and efficacy for clinical use. As the healthcare industry moves towards more precise and personalized diagnostic solutions, the role of micron and nanoscale lipid microbubble contrast agents is expected to become increasingly prominent. In conclusion, the integration of micron and nanoscale technologies in the global lipid microbubble contrast agent market is revolutionizing the field of medical imaging and diagnostics. These advanced agents offer enhanced imaging capabilities, targeted delivery options, and the potential for personalized medicine, making them invaluable tools in the fight against various diseases.

Hospital, Clinic, Other in the Global Lipid Microbubble Contrast Agent Market:

The usage of global lipid microbubble contrast agents spans across various healthcare settings, including hospitals, clinics, and other medical facilities. In hospitals, these contrast agents are primarily used in radiology and cardiology departments for diagnostic imaging procedures. The enhanced imaging capabilities provided by lipid microbubble contrast agents allow radiologists and cardiologists to obtain clearer and more detailed images of blood vessels, heart chambers, and other internal structures. This improved visualization aids in the accurate diagnosis of conditions such as cardiovascular diseases, tumors, and organ abnormalities. Additionally, lipid microbubble contrast agents are used in interventional procedures, such as guiding catheter placements and monitoring the success of treatments like angioplasty or stent placements. The ability to visualize blood flow in real-time during these procedures enhances the precision and safety of the interventions, ultimately improving patient outcomes. In clinics, lipid microbubble contrast agents are utilized for a variety of diagnostic purposes, including routine check-ups and specialized imaging studies. Clinics often serve as the first point of contact for patients experiencing symptoms that require further investigation. The use of lipid microbubble contrast agents in ultrasound imaging enables clinicians to quickly and non-invasively assess the condition of organs and tissues, facilitating early detection and timely referral to specialists if needed. For example, in obstetrics and gynecology clinics, these agents can be used to evaluate fetal health and monitor pregnancy progress. In urology clinics, they assist in diagnosing kidney stones, bladder tumors, and other urinary tract conditions. The versatility and safety profile of lipid microbubble contrast agents make them suitable for use in a wide range of clinical applications, enhancing the diagnostic capabilities of clinics and improving patient care. Beyond hospitals and clinics, lipid microbubble contrast agents find applications in other medical settings, such as research institutions and specialized diagnostic centers. In research institutions, these agents are used in preclinical studies to investigate disease mechanisms, evaluate new therapeutic approaches, and develop innovative imaging techniques. The ability to visualize molecular and cellular processes in vivo using lipid microbubble contrast agents provides valuable insights that drive scientific advancements and contribute to the development of new medical technologies. Specialized diagnostic centers, which focus on specific medical conditions or advanced imaging techniques, also benefit from the use of these contrast agents. For instance, centers specializing in oncology may use lipid microbubble contrast agents to enhance the detection and characterization of tumors, while centers focused on vascular diseases may utilize them to assess blood flow and vessel integrity. The adoption of lipid microbubble contrast agents in these settings underscores their importance in advancing medical research and improving diagnostic accuracy. In conclusion, the usage of global lipid microbubble contrast agents extends across hospitals, clinics, and other medical facilities, playing a vital role in enhancing diagnostic imaging and patient care. Their ability to provide clear and detailed images of internal structures, coupled with their safety and versatility, makes them indispensable tools in various medical applications. As the demand for accurate and non-invasive diagnostic procedures continues to grow, the adoption of lipid microbubble contrast agents is expected to increase, further solidifying their position in the healthcare industry.

Global Lipid Microbubble Contrast Agent Market Outlook:

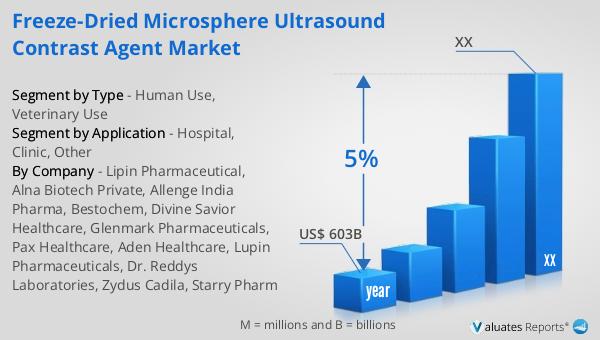

The global Lipid Microbubble Contrast Agent market was valued at US$ 565 million in 2023 and is anticipated to reach US$ 797.4 million by 2030, witnessing a CAGR of 5.0% during the forecast period from 2024 to 2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% over the next six years. This growth is driven by the increasing demand for advanced diagnostic tools and the rising prevalence of chronic diseases worldwide. The lipid microbubble contrast agents market, in particular, is benefiting from advancements in ultrasound technology and the growing preference for non-invasive imaging techniques. The market is also supported by the expanding geriatric population, which is more susceptible to various medical conditions requiring diagnostic imaging. Additionally, the increasing number of diagnostic imaging centers and the continuous research and development activities aimed at improving the efficacy and safety of these contrast agents are contributing to the market's growth. Overall, the global Lipid Microbubble Contrast Agent market is poised for significant expansion, driven by technological advancements and the increasing need for accurate and efficient diagnostic tools.

| Report Metric |

Details |

| Report Name |

Lipid Microbubble Contrast Agent Market |

| Accounted market size in 2023 |

US$ 565 million |

| Forecasted market size in 2030 |

US$ 797.4 million |

| CAGR |

5.0% |

| Base Year |

2023 |

| Forecasted years |

2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

Lantheus Medical Imaging, Bracco SpA, GE Healthcare, Daiichi Sankyo Company, Bayer, Guerbet Group, Hengrui Medicine, BeiLu Pharmaceutical, Qihui Biology |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |