What is Global Hemodialysis Concentrate and Dry Powder Market?

The global Hemodialysis Concentrate and Dry Powder market is a specialized segment within the broader medical device industry. Hemodialysis is a medical procedure used to treat patients with kidney failure by removing waste products and excess fluid from the blood. The concentrates and dry powders used in hemodialysis are essential components of the dialysis process. These products are mixed with purified water to create a dialysis solution that helps cleanse the blood. The market for these products is driven by the increasing prevalence of chronic kidney diseases, advancements in dialysis technology, and the growing number of dialysis centers worldwide. The market is characterized by a variety of products, including bicarbonate concentrates, acid concentrates, and dry powder formulations, each designed to meet specific clinical needs. The demand for these products is expected to grow steadily, driven by the rising number of patients requiring dialysis and the ongoing improvements in dialysis treatment protocols.

Concentrate, Dry Powder in the Global Hemodialysis Concentrate and Dry Powder Market:

Concentrates and dry powders are critical components in the hemodialysis process. Concentrates are typically liquid solutions that contain essential electrolytes and chemicals needed to create the dialysis solution. These solutions are mixed with purified water to achieve the desired concentration levels required for effective dialysis treatment. The primary types of concentrates used in hemodialysis include bicarbonate concentrates and acid concentrates. Bicarbonate concentrates help maintain the acid-base balance in the blood, while acid concentrates contain essential electrolytes such as sodium, potassium, and calcium. On the other hand, dry powders are solid formulations that are mixed with water to create the dialysis solution. These powders offer several advantages, including ease of storage, longer shelf life, and reduced transportation costs. Dry powder formulations are particularly beneficial in regions with limited access to liquid concentrates or where transportation infrastructure is underdeveloped. The use of dry powders also reduces the risk of contamination and allows for more precise control over the composition of the dialysis solution. Both concentrates and dry powders play a crucial role in ensuring the safety and efficacy of hemodialysis treatment, making them indispensable in the management of chronic kidney diseases.

Hospital, Clinic in the Global Hemodialysis Concentrate and Dry Powder Market:

In hospitals, the usage of hemodialysis concentrates and dry powders is integral to the treatment of patients with acute and chronic kidney failure. Hospitals often have dedicated dialysis units equipped with advanced dialysis machines and trained medical staff to administer hemodialysis treatments. The concentrates and dry powders are used to prepare the dialysis solution, which is then circulated through the dialysis machine to cleanse the patient's blood. The availability of high-quality concentrates and dry powders ensures that the dialysis solution is safe and effective, minimizing the risk of complications and improving patient outcomes. In clinics, the use of hemodialysis concentrates and dry powders is equally important. Clinics, especially those specializing in nephrology, provide outpatient dialysis services to patients with chronic kidney diseases. These clinics rely on a steady supply of concentrates and dry powders to prepare the dialysis solution for their patients. The use of these products in clinics allows for the efficient management of dialysis treatments, ensuring that patients receive the necessary care without the need for hospitalization. The availability of concentrates and dry powders in clinics also enables patients to receive regular dialysis treatments closer to their homes, improving their quality of life and reducing the burden on hospital resources.

Global Hemodialysis Concentrate and Dry Powder Market Outlook:

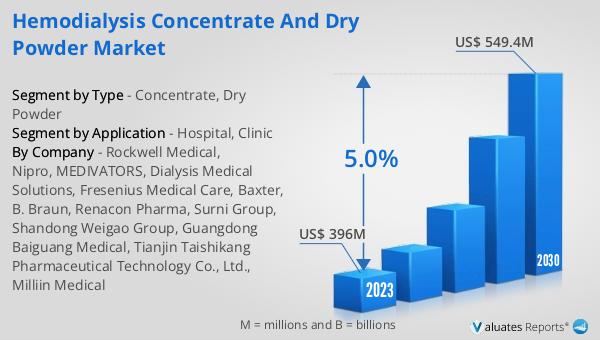

The global Hemodialysis Concentrate and Dry Powder market was valued at US$ 396 million in 2023 and is anticipated to reach US$ 549.4 million by 2030, witnessing a CAGR of 5.0% during the forecast period from 2024 to 2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% during the next six years. This growth is driven by the increasing prevalence of chronic diseases, advancements in medical technology, and the rising demand for healthcare services worldwide. The Hemodialysis Concentrate and Dry Powder market is expected to benefit from these trends, as the need for effective dialysis treatments continues to rise. The market's steady growth reflects the ongoing efforts to improve dialysis care and the increasing number of patients requiring dialysis treatment.

| Report Metric | Details |

| Report Name | Hemodialysis Concentrate and Dry Powder Market |

| Accounted market size in 2023 | US$ 396 million |

| Forecasted market size in 2030 | US$ 549.4 million |

| CAGR | 5.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Rockwell Medical, Nipro, MEDIVATORS, Dialysis Medical Solutions, Fresenius Medical Care, Baxter, B. Braun, Renacon Pharma, Surni Group, Shandong Weigao Group, Guangdong Baiguang Medical, Tianjin Taishikang Pharmaceutical Technology Co., Ltd., Milliin Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |