What is Global Pipeline In-Line Viscometer Market?

The Global Pipeline In-Line Viscometer Market refers to the industry focused on the production, distribution, and application of viscometers that are installed directly within pipelines to measure the viscosity of fluids in real-time. These devices are crucial for industries that require precise monitoring and control of fluid properties to ensure optimal processing and product quality. The market encompasses various types of viscometers, including vibration and rotational viscometers, each designed to meet specific industrial needs. The demand for these instruments is driven by their ability to provide continuous, accurate, and real-time data, which is essential for maintaining the efficiency and safety of industrial processes. As industries such as petroleum, chemical, pharmaceutical, and food processing continue to grow and evolve, the need for advanced viscometry solutions is expected to increase, further propelling the market. The global pipeline in-line viscometer market is characterized by technological advancements, increasing automation, and the integration of smart technologies, which enhance the functionality and reliability of these instruments.

Vibration Viscometer, Rotational Viscometer in the Global Pipeline In-Line Viscometer Market:

Vibration viscometers and rotational viscometers are two prominent types of instruments used in the Global Pipeline In-Line Viscometer Market. Vibration viscometers operate by measuring the damping of an oscillating object immersed in the fluid. The principle behind this is that the viscosity of the fluid affects the damping characteristics of the oscillating object. These viscometers are highly sensitive and can provide accurate measurements even in challenging conditions, such as high-pressure environments or with fluids that have varying compositions. They are particularly useful in applications where continuous monitoring is required, as they can deliver real-time data without interrupting the flow of the fluid. On the other hand, rotational viscometers measure viscosity by rotating a spindle within the fluid and measuring the torque required to maintain a constant rotational speed. The resistance encountered by the spindle is directly related to the viscosity of the fluid. Rotational viscometers are known for their versatility and can handle a wide range of fluid viscosities, making them suitable for various industrial applications. They are often used in quality control processes where precise viscosity measurements are critical. Both types of viscometers have their unique advantages and are chosen based on the specific requirements of the application. In the context of the Global Pipeline In-Line Viscometer Market, these instruments play a vital role in ensuring the efficiency and reliability of industrial processes by providing accurate and continuous viscosity measurements.

Petroleum, Chemical, Pharmaceutical, Food Processing in the Global Pipeline In-Line Viscometer Market:

The usage of Global Pipeline In-Line Viscometer Market in various industries such as petroleum, chemical, pharmaceutical, and food processing is extensive and multifaceted. In the petroleum industry, in-line viscometers are essential for monitoring the viscosity of crude oil and refined products. Accurate viscosity measurements are crucial for optimizing the refining process, ensuring the quality of the final product, and maintaining the efficiency of transportation pipelines. In the chemical industry, these viscometers are used to monitor the viscosity of various chemical compounds and mixtures. This is important for ensuring the consistency and quality of chemical products, as well as for optimizing production processes. In the pharmaceutical industry, in-line viscometers are used to monitor the viscosity of liquid medications and other pharmaceutical products. This is critical for ensuring the proper dosage and effectiveness of medications, as well as for maintaining the quality and safety of pharmaceutical products. In the food processing industry, in-line viscometers are used to monitor the viscosity of various food products, such as sauces, syrups, and dairy products. This is important for ensuring the consistency and quality of food products, as well as for optimizing production processes. Overall, the usage of in-line viscometers in these industries is essential for maintaining the quality, efficiency, and safety of industrial processes and products.

Global Pipeline In-Line Viscometer Market Outlook:

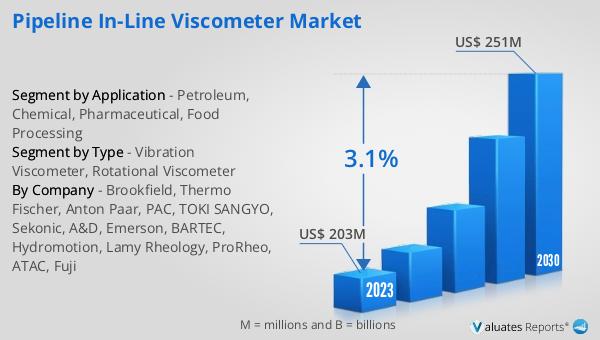

The global Pipeline In-Line Viscometer market was valued at US$ 203 million in 2023 and is anticipated to reach US$ 251 million by 2030, witnessing a CAGR of 3.1% during the forecast period 2024-2030. This growth can be attributed to the increasing demand for accurate and real-time viscosity measurements in various industries, such as petroleum, chemical, pharmaceutical, and food processing. The market is characterized by technological advancements, increasing automation, and the integration of smart technologies, which enhance the functionality and reliability of these instruments. As industries continue to grow and evolve, the need for advanced viscometry solutions is expected to increase, further propelling the market. The demand for these instruments is driven by their ability to provide continuous, accurate, and real-time data, which is essential for maintaining the efficiency and safety of industrial processes. The global pipeline in-line viscometer market is expected to witness significant growth during the forecast period, driven by the increasing demand for accurate and real-time viscosity measurements in various industries.

| Report Metric | Details |

| Report Name | Pipeline In-Line Viscometer Market |

| Accounted market size in 2023 | US$ 203 million |

| Forecasted market size in 2030 | US$ 251 million |

| CAGR | 3.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Brookfield, Thermo Fischer, Anton Paar, PAC, TOKI SANGYO, Sekonic, A&D, Emerson, BARTEC, Hydromotion, Lamy Rheology, ProRheo, ATAC, Fuji |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |