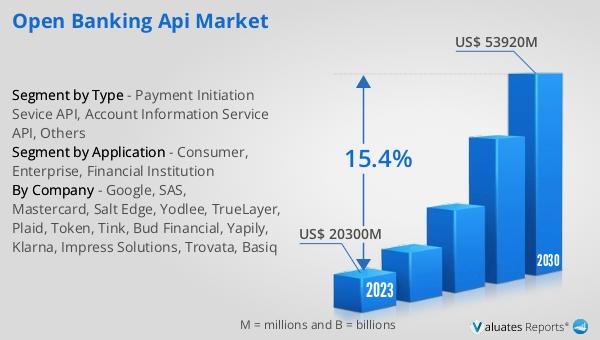

What is Global Circumcision Surgical Stapler Market?

The Global Circumcision Surgical Stapler Market refers to the worldwide industry focused on the production, distribution, and utilization of surgical staplers specifically designed for circumcision procedures. These devices are used to perform circumcisions more efficiently and with less risk of complications compared to traditional methods. The market encompasses various types of staplers, including those designed for use in children and adults. The demand for these devices is driven by factors such as the increasing prevalence of circumcision for medical, cultural, and religious reasons, as well as advancements in medical technology that make these procedures safer and more accessible. The market is also influenced by regional differences in circumcision practices and healthcare infrastructure. Overall, the Global Circumcision Surgical Stapler Market is a specialized segment within the broader medical devices industry, offering innovative solutions to improve patient outcomes and streamline surgical procedures.

Child Type, Adult Type in the Global Circumcision Surgical Stapler Market:

In the Global Circumcision Surgical Stapler Market, devices are categorized based on their intended use for different age groups, primarily children and adults. Child-type circumcision staplers are specifically designed to accommodate the anatomical and physiological differences of younger patients. These staplers are typically smaller in size and may feature additional safety mechanisms to ensure precision and minimize the risk of injury. The design considerations for child-type staplers also include ease of use for healthcare providers, as pediatric patients may require quicker and less invasive procedures to reduce stress and discomfort. On the other hand, adult-type circumcision staplers are engineered to handle the larger and more developed anatomy of adult patients. These staplers often have a more robust construction to ensure they can effectively manage the thicker and more resilient tissue found in adults. Additionally, adult-type staplers may offer adjustable settings to accommodate variations in tissue thickness and patient anatomy, providing a more customized and effective surgical experience. Both child and adult-type staplers are designed to improve the efficiency and safety of circumcision procedures, reducing the risk of complications such as bleeding, infection, and prolonged recovery times. The choice between child and adult-type staplers depends on the patient's age and specific medical needs, with healthcare providers selecting the appropriate device to ensure optimal outcomes. The development and refinement of these staplers are driven by ongoing research and innovation in the medical field, aiming to enhance the overall quality of care for patients undergoing circumcision.

Hospitals, Clinics in the Global Circumcision Surgical Stapler Market:

The usage of Global Circumcision Surgical Staplers in hospitals and clinics is a significant aspect of modern medical practice. In hospitals, these staplers are often used in surgical departments where circumcision procedures are performed as part of routine medical care or for specific medical indications. Hospitals typically have the infrastructure and resources to support the use of advanced surgical devices, including circumcision staplers. The availability of trained surgical staff and comprehensive post-operative care facilities in hospitals ensures that patients receive high-quality care throughout the circumcision process. The use of surgical staplers in hospitals can lead to shorter procedure times, reduced risk of complications, and faster recovery for patients. In clinics, circumcision surgical staplers are used in a more localized and often less resource-intensive setting. Clinics may offer circumcision as an outpatient procedure, providing a convenient option for patients who do not require hospitalization. The use of staplers in clinics allows for efficient and minimally invasive circumcision procedures, which can be particularly beneficial in regions with limited access to advanced medical facilities. Clinics often serve as the primary point of care for many patients, making the availability of circumcision staplers an important factor in ensuring access to safe and effective surgical options. Both hospitals and clinics benefit from the use of circumcision surgical staplers by improving the overall efficiency and safety of the procedure, ultimately enhancing patient outcomes and satisfaction.

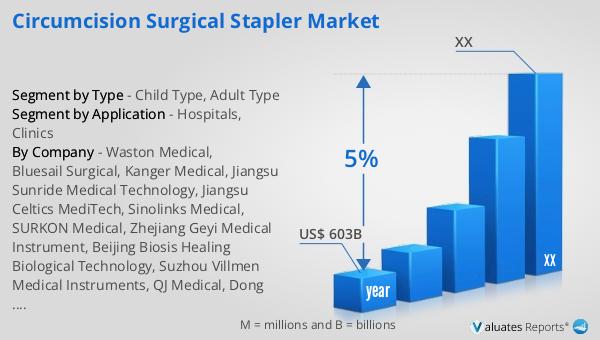

Global Circumcision Surgical Stapler Market Outlook:

According to our research, the global market for medical devices is projected to reach approximately $603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by various factors, including advancements in medical technology, increasing demand for healthcare services, and the rising prevalence of chronic diseases that require medical intervention. The medical devices market encompasses a wide range of products, from diagnostic equipment and surgical instruments to implantable devices and wearable health monitors. The continuous innovation in this field is aimed at improving patient care, enhancing the accuracy of diagnoses, and providing more effective treatment options. As the healthcare industry evolves, the demand for sophisticated medical devices is expected to grow, contributing to the overall expansion of the market. This growth trajectory highlights the importance of ongoing research and development in the medical devices sector, as well as the need for regulatory frameworks that ensure the safety and efficacy of new products. The global market for medical devices plays a crucial role in shaping the future of healthcare, offering new opportunities for improving patient outcomes and addressing the diverse needs of populations worldwide.

| Report Metric | Details |

| Report Name | Circumcision Surgical Stapler Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Waston Medical, Bluesail Surgical, Kanger Medical, Jiangsu Sunride Medical Technology, Jiangsu Celtics MediTech, Sinolinks Medical, SURKON Medical, Zhejiang Geyi Medical Instrument, Beijing Biosis Healing Biological Technology, Suzhou Villmen Medical Instruments, QJ Medical, Dong Feng YiHe Technology, Victor Medical Instruments, Surgaid Medical, Safir Medical, ZSR Biomedical Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |