What is Global Carbodiimide Anti-Hydrolysis Agent Market?

The Global Carbodiimide Anti-Hydrolysis Agent Market refers to the worldwide industry focused on the production, distribution, and application of carbodiimide compounds that prevent hydrolysis. Hydrolysis is a chemical reaction where water breaks down materials, which can be detrimental to various products, especially polymers. Carbodiimide anti-hydrolysis agents are used to enhance the durability and longevity of materials by preventing this breakdown. These agents are crucial in industries where materials are exposed to moisture and need to maintain their structural integrity over time. The market encompasses a range of products, including monomeric and polymeric carbodiimides, each with specific applications and benefits. The demand for these agents is driven by their effectiveness in extending the life of materials, making them essential in sectors such as automotive, electronics, packaging, and textiles. As industries continue to seek ways to improve the performance and lifespan of their products, the global carbodiimide anti-hydrolysis agent market is expected to grow, reflecting the increasing need for advanced material protection solutions.

Monomeric Carbodiimide Anti-Hydrolysis Agents, Polymeric Carbodiimide Anti-Hydrolysis Agents in the Global Carbodiimide Anti-Hydrolysis Agent Market:

Monomeric carbodiimide anti-hydrolysis agents are single-molecule compounds that play a significant role in the global carbodiimide anti-hydrolysis agent market. These agents are particularly effective in applications where precise control over the chemical reaction is required. Monomeric carbodiimides are known for their ability to react quickly and efficiently with water, thereby preventing hydrolysis. They are often used in applications where a high degree of flexibility and reactivity is needed, such as in coatings, adhesives, and sealants. These agents are also favored in situations where the material needs to maintain its properties under varying environmental conditions. On the other hand, polymeric carbodiimide anti-hydrolysis agents consist of long-chain molecules that provide a more robust and durable solution for preventing hydrolysis. These agents are typically used in applications where long-term stability and resistance to harsh conditions are critical. Polymeric carbodiimides are commonly found in automotive parts, electronic components, and packaging materials, where they help to extend the lifespan of products by providing a strong barrier against moisture. The choice between monomeric and polymeric carbodiimides depends on the specific requirements of the application, including the desired level of protection, flexibility, and durability. Both types of agents are essential in the global carbodiimide anti-hydrolysis agent market, offering tailored solutions to meet the diverse needs of various industries. As technology advances and new applications emerge, the demand for both monomeric and polymeric carbodiimides is expected to continue growing, driven by the need for more effective and reliable anti-hydrolysis solutions.

TPU, PU, PET, PBT, Other in the Global Carbodiimide Anti-Hydrolysis Agent Market:

The usage of global carbodiimide anti-hydrolysis agents spans across various materials, including TPU (Thermoplastic Polyurethane), PU (Polyurethane), PET (Polyethylene Terephthalate), PBT (Polybutylene Terephthalate), and others. In TPU, these agents are used to enhance the material's resistance to hydrolysis, which is crucial for applications in automotive parts, footwear, and medical devices. TPU is known for its flexibility and durability, but exposure to moisture can degrade its properties over time. Carbodiimide anti-hydrolysis agents help to maintain TPU's performance by preventing water-induced breakdown. In PU, which is widely used in foams, coatings, and adhesives, these agents play a vital role in extending the material's lifespan. PU is susceptible to hydrolysis, especially in humid environments, and the addition of carbodiimide agents ensures that it retains its structural integrity and functionality. For PET, commonly used in packaging and textile industries, carbodiimide anti-hydrolysis agents provide essential protection against moisture, ensuring that the material remains strong and durable. PET's resistance to hydrolysis is particularly important in packaging applications, where it needs to maintain its barrier properties to protect the contents. In PBT, used in electrical and electronic components, these agents help to prevent hydrolysis, which can compromise the material's insulating properties and mechanical strength. The use of carbodiimide anti-hydrolysis agents in PBT ensures that electronic components remain reliable and safe over time. Other materials that benefit from these agents include various engineering plastics and elastomers, where hydrolysis resistance is crucial for maintaining performance and longevity. Overall, the application of carbodiimide anti-hydrolysis agents in these materials highlights their importance in enhancing the durability and reliability of products across multiple industries.

Global Carbodiimide Anti-Hydrolysis Agent Market Outlook:

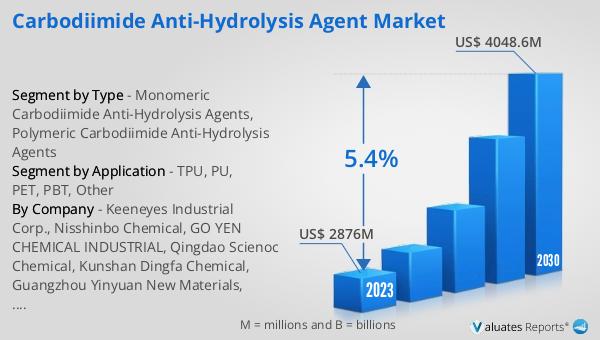

The global carbodiimide anti-hydrolysis agent market was valued at US$ 2876 million in 2023 and is anticipated to reach US$ 4048.6 million by 2030, witnessing a CAGR of 5.4% during the forecast period 2024-2030. This growth reflects the increasing demand for materials that can withstand hydrolysis, driven by the need for more durable and long-lasting products in various industries. The market's expansion is supported by advancements in technology and the development of new applications for carbodiimide anti-hydrolysis agents. As industries continue to seek ways to improve the performance and lifespan of their products, the demand for these agents is expected to rise. The market outlook indicates a positive trend, with significant opportunities for growth and innovation in the coming years. The increasing awareness of the benefits of carbodiimide anti-hydrolysis agents, coupled with the growing need for advanced material protection solutions, is likely to drive the market's expansion. Companies operating in this market are focusing on research and development to create more effective and efficient products, catering to the evolving needs of various industries. The global carbodiimide anti-hydrolysis agent market is poised for substantial growth, reflecting the ongoing demand for high-performance materials that can withstand the challenges posed by moisture and environmental conditions.

| Report Metric | Details |

| Report Name | Carbodiimide Anti-Hydrolysis Agent Market |

| Accounted market size in 2023 | US$ 2876 million |

| Forecasted market size in 2030 | US$ 4048.6 million |

| CAGR | 5.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Keeneyes Industrial Corp., Nisshinbo Chemical, GO YEN CHEMICAL INDUSTRIAL, Qingdao Scienoc Chemical, Kunshan Dingfa Chemical, Guangzhou Yinyuan New Materials, Nanjing Baitong New Material, LANXESS, Afine Chemicals, Shanghai LongTome International Trade, BASF SE, Shanghai Deborn, Shanghai Hengyuan Macromolecular Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |