What is Global Solder Resist Ink Market?

The Global Solder Resist Ink Market is a specialized segment within the broader electronics industry, focusing on the production and application of solder resist inks. These inks are essential in the manufacturing of printed circuit boards (PCBs), which are the backbone of virtually all electronic devices. Solder resist ink, also known as solder mask, is a protective layer applied to the surface of PCBs to prevent solder bridges from forming between closely spaced solder pads. This ensures that the electrical connections are precise and reliable, which is crucial for the functionality of electronic devices. The market for solder resist ink is driven by the increasing demand for electronic devices, advancements in PCB technology, and the need for high-performance and durable electronic components. The market encompasses various types of solder resist inks, including photoimageable, thermal curable, and UV curable inks, each with its unique properties and applications. The growth of the global solder resist ink market is also influenced by the expansion of the electronics industry in emerging economies, technological innovations, and the increasing complexity of electronic devices.

Photoimageable Solder Resist Ink, Thermal Curable Solder Resist Ink, UV Curable Solder Resist Ink in the Global Solder Resist Ink Market:

Photoimageable Solder Resist Ink, Thermal Curable Solder Resist Ink, and UV Curable Solder Resist Ink are the three primary types of solder resist inks used in the global market, each catering to specific needs and applications within the electronics industry. Photoimageable Solder Resist Ink is designed to be sensitive to light, allowing for precise patterning on PCBs through a photolithographic process. This type of ink is particularly useful for high-density and high-precision applications, such as in advanced consumer electronics and communication devices. The photolithographic process involves coating the PCB with the photoimageable ink, exposing it to UV light through a photomask, and then developing the exposed areas to create the desired pattern. This method ensures high accuracy and fine resolution, making it ideal for complex circuit designs. Thermal Curable Solder Resist Ink, on the other hand, requires heat to cure and harden. This type of ink is known for its excellent adhesion, chemical resistance, and durability, making it suitable for applications that demand robust performance under harsh conditions. Thermal curable inks are often used in automotive electronics, industrial equipment, and other applications where reliability and longevity are critical. The curing process involves applying the ink to the PCB and then subjecting it to high temperatures to achieve the desired hardness and protective properties. UV Curable Solder Resist Ink is cured using ultraviolet light, offering a fast and efficient curing process. This type of ink is favored for its quick turnaround time, making it ideal for high-volume production environments. UV curable inks provide good adhesion, flexibility, and resistance to chemicals and abrasion, making them suitable for a wide range of applications, including consumer electronics, communication devices, and IC packaging. The UV curing process involves exposing the applied ink to UV light, which initiates a photochemical reaction that hardens the ink almost instantly. Each type of solder resist ink has its advantages and is chosen based on the specific requirements of the application, such as the desired level of precision, durability, and production speed. The global market for solder resist inks continues to evolve, driven by technological advancements and the increasing complexity of electronic devices, leading to the development of new formulations and improved performance characteristics.

Computers, Communications, Consumer Electronics, IC Packaging in the Global Solder Resist Ink Market:

The usage of Global Solder Resist Ink Market spans across various sectors, including computers, communications, consumer electronics, and IC packaging, each with its unique requirements and applications. In the computer industry, solder resist inks are crucial for the manufacturing of motherboards, graphics cards, and other critical components. These inks ensure that the intricate circuitry on PCBs is protected from solder bridges, which can cause short circuits and malfunctions. The high precision and reliability offered by solder resist inks are essential for the performance and longevity of computer components, which are becoming increasingly complex and powerful. In the communications sector, solder resist inks are used in the production of devices such as smartphones, routers, and network infrastructure equipment. The demand for high-speed and reliable communication devices drives the need for advanced PCBs with precise and durable solder masks. Solder resist inks help in maintaining the integrity of the circuitry, ensuring that the devices can handle high-frequency signals and provide consistent performance. Consumer electronics, including televisions, gaming consoles, and wearable devices, also rely heavily on solder resist inks. These inks protect the delicate circuitry within these devices, ensuring that they can withstand everyday use and environmental factors such as moisture and dust. The versatility and durability of solder resist inks make them ideal for consumer electronics, where both performance and aesthetics are important. In the field of IC packaging, solder resist inks play a vital role in protecting the delicate connections between the integrated circuits and the PCBs. The inks provide a protective barrier that prevents solder from bridging the fine pitch connections, ensuring the reliability and performance of the packaged ICs. This is particularly important in applications such as automotive electronics, medical devices, and industrial equipment, where the reliability of the electronic components is critical. The global solder resist ink market continues to grow, driven by the increasing demand for advanced electronic devices and the need for high-performance and reliable PCBs across various industries.

Global Solder Resist Ink Market Outlook:

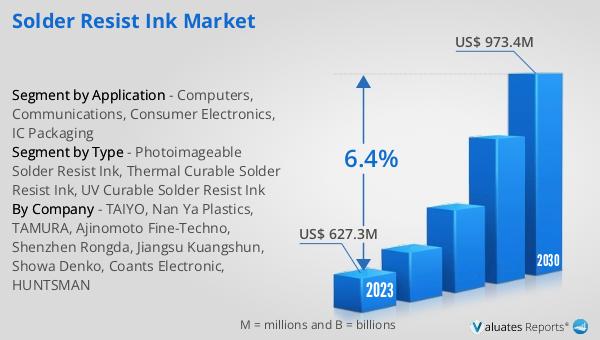

The global Solder Resist Ink market is anticipated to expand from $670.9 million in 2024 to $973.4 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 6.4% over the forecast period. TAIYO stands out as the leading manufacturer in this market, commanding a revenue market share that exceeds 50% as of 2019. This significant market presence underscores TAIYO's dominance and influence within the industry. The projected growth of the solder resist ink market is indicative of the increasing demand for high-quality and reliable electronic components across various sectors, including consumer electronics, communications, and industrial applications. The advancements in PCB technology and the growing complexity of electronic devices further drive the need for innovative and efficient solder resist inks. As the market continues to evolve, manufacturers are likely to focus on developing new formulations and improving the performance characteristics of solder resist inks to meet the ever-changing demands of the electronics industry. The expansion of the market also highlights the importance of solder resist inks in ensuring the reliability and functionality of electronic devices, which are integral to modern life.

| Report Metric | Details |

| Report Name | Solder Resist Ink Market |

| Accounted market size in 2024 | US$ 670.9 million |

| Forecasted market size in 2030 | US$ 973.4 million |

| CAGR | 6.4 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | TAIYO, Nan Ya Plastics, TAMURA, Ajinomoto Fine-Techno, Shenzhen Rongda, Jiangsu Kuangshun, Showa Denko, Coants Electronic, HUNTSMAN |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |