What is Global Ophthalmic Operating Microscopes Market?

The Global Ophthalmic Operating Microscopes Market is a specialized segment within the broader medical devices industry, focusing on microscopes used in eye surgeries. These microscopes are essential tools for ophthalmologists, providing high magnification and illumination to perform intricate procedures on the eye. The market encompasses a variety of products designed to meet the specific needs of different types of eye surgeries, such as cataract, glaucoma, and retinal surgeries. These devices are crucial for enhancing the precision and outcomes of surgical interventions, thereby improving patient care. The market is driven by factors such as the increasing prevalence of eye disorders, advancements in technology, and the growing demand for minimally invasive surgeries. Additionally, the aging population and rising awareness about eye health contribute to the market's growth. The global reach of this market means that it caters to a diverse range of healthcare settings, from well-established hospitals in developed countries to emerging healthcare facilities in developing regions. Overall, the Global Ophthalmic Operating Microscopes Market plays a vital role in the field of ophthalmology, supporting the delivery of high-quality eye care worldwide.

On Casters, Wall Mount, Table Top, Ceiling Mounted in the Global Ophthalmic Operating Microscopes Market:

In the Global Ophthalmic Operating Microscopes Market, various mounting options are available to cater to different surgical environments and preferences. On casters, wall mount, table top, and ceiling mounted are the primary types of mounting configurations for these microscopes. On casters microscopes are mobile units equipped with wheels, allowing for easy movement and repositioning within the operating room. This flexibility is particularly beneficial in multi-functional surgical suites where space and equipment need to be reconfigured frequently. Wall mount microscopes, on the other hand, are fixed to the wall, providing a stable and space-saving solution. These are ideal for smaller operating rooms where floor space is limited, ensuring that the microscope is always in a ready-to-use position without occupying valuable floor area. Table top microscopes are compact units designed to be placed on a table or a dedicated stand. These are often used in outpatient settings or smaller surgical centers where portability and ease of setup are crucial. They offer a balance between mobility and stability, making them suitable for a variety of surgical procedures. Ceiling mounted microscopes are installed on the ceiling, providing maximum floor space and eliminating any obstructions in the operating area. This configuration is particularly advantageous in high-traffic operating rooms where multiple pieces of equipment need to be accommodated. Ceiling mounted units also offer the benefit of being easily adjustable, allowing surgeons to position the microscope precisely where needed without any hindrance. Each of these mounting options has its own set of advantages and is chosen based on the specific requirements of the surgical environment, the type of procedures performed, and the preferences of the surgical team. The availability of these diverse mounting configurations ensures that ophthalmic operating microscopes can be effectively integrated into various healthcare settings, enhancing the efficiency and effectiveness of eye surgeries.

Hospitals, Ambulatory Surgical Centers, Others in the Global Ophthalmic Operating Microscopes Market:

The usage of Global Ophthalmic Operating Microscopes Market extends across various healthcare settings, including hospitals, ambulatory surgical centers, and other specialized medical facilities. In hospitals, these microscopes are a critical component of the ophthalmology department, supporting a wide range of surgical procedures. Hospitals often have dedicated ophthalmic surgery units equipped with advanced microscopes to handle complex cases such as cataract removal, retinal detachment repair, and corneal transplants. The high patient volume and the need for comprehensive eye care services make hospitals a significant market for these devices. Ambulatory surgical centers (ASCs) are another key area where ophthalmic operating microscopes are extensively used. ASCs are specialized facilities that focus on providing same-day surgical care, including diagnostic and preventive procedures. These centers are designed to offer a more convenient and cost-effective alternative to hospital-based surgeries. Ophthalmic operating microscopes in ASCs are used for procedures like LASIK, cataract surgery, and other minimally invasive eye surgeries. The portability and ease of use of these microscopes make them ideal for the fast-paced environment of ASCs, where efficiency and quick turnaround times are crucial. Other settings where these microscopes are utilized include private clinics, research institutions, and educational facilities. Private clinics often cater to patients seeking specialized eye care services, and having advanced operating microscopes enhances the quality of care provided. Research institutions use these microscopes for studying eye diseases and developing new surgical techniques, contributing to the advancement of ophthalmology. Educational facilities, such as medical schools and training centers, use these microscopes to train the next generation of ophthalmologists, ensuring that they are well-equipped with the skills and knowledge needed to perform intricate eye surgeries. Overall, the versatility and advanced features of ophthalmic operating microscopes make them indispensable tools in various healthcare settings, supporting the delivery of high-quality eye care and improving surgical outcomes.

Global Ophthalmic Operating Microscopes Market Outlook:

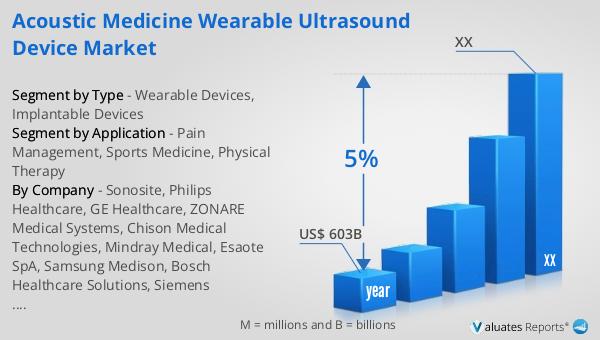

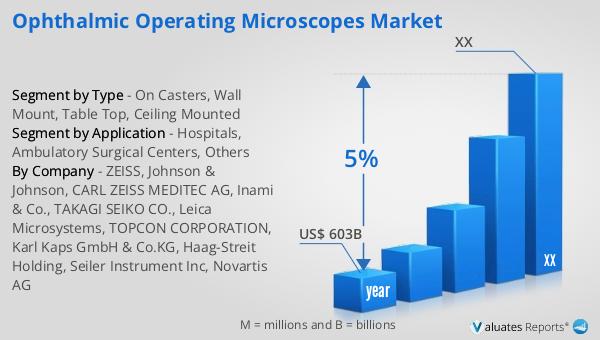

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth trajectory underscores the increasing demand for advanced medical technologies and devices across various healthcare sectors. The expanding market reflects the continuous advancements in medical technology, the rising prevalence of chronic diseases, and the growing emphasis on improving patient outcomes. As healthcare systems worldwide strive to enhance the quality of care, the adoption of innovative medical devices is expected to play a crucial role. The ophthalmic operating microscopes market, as a part of this broader medical devices market, is poised to benefit from these trends. The increasing focus on eye health, coupled with technological advancements in surgical equipment, is likely to drive the demand for ophthalmic operating microscopes. These devices are essential for performing precise and minimally invasive eye surgeries, which are becoming more common as the global population ages and the prevalence of eye disorders rises. The projected growth in the medical devices market highlights the importance of continued innovation and investment in this sector to meet the evolving needs of healthcare providers and patients. Overall, the positive outlook for the medical devices market bodes well for the future of ophthalmic operating microscopes, supporting their critical role in advancing eye care and improving surgical outcomes.

| Report Metric | Details |

| Report Name | Ophthalmic Operating Microscopes Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | ZEISS, Johnson & Johnson, CARL ZEISS MEDITEC AG, Inami & Co., TAKAGI SEIKO CO., Leica Microsystems, TOPCON CORPORATION, Karl Kaps GmbH & Co.KG, Haag-Streit Holding, Seiler Instrument Inc, Novartis AG |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |