What is Global Flow Cytometry Analyser Market?

The Global Flow Cytometry Analyser Market is a rapidly evolving sector within the field of biotechnology and medical diagnostics. Flow cytometry is a powerful technique used to analyze the physical and chemical characteristics of particles in a fluid as it passes through at least one laser. This technology is widely used in various applications such as immunology, cell biology, cancer research, and clinical diagnostics. The market for flow cytometry analyzers is driven by the increasing prevalence of chronic diseases, advancements in technology, and the growing demand for early and accurate disease diagnosis. These analyzers are essential tools in both research and clinical settings, providing detailed information about cell populations and their functions. The global market is characterized by a diverse range of products, including benchtop and high-throughput analyzers, each designed to meet specific needs and applications. As the demand for personalized medicine and targeted therapies continues to grow, the importance of flow cytometry analyzers in the global healthcare landscape is expected to increase.

Benchtop Flow Cytometer, High-throughput Flow Cytometer, Multicolor Flow Cytometer, Cell Sorting Flow Cytometer, Microfluidic Flow Cytometer in the Global Flow Cytometry Analyser Market:

Benchtop Flow Cytometers are compact and versatile instruments designed for routine laboratory use. They are ideal for small to medium-sized laboratories that require reliable and accurate cell analysis. These devices are user-friendly and offer a range of features such as multi-parameter analysis, high sensitivity, and flexibility in sample handling. High-throughput Flow Cytometers, on the other hand, are designed for large-scale studies and clinical trials. They can process thousands of samples in a short period, making them suitable for high-volume laboratories and research institutions. These analyzers are equipped with advanced automation and data management capabilities, allowing for efficient and streamlined workflows. Multicolor Flow Cytometers are specialized instruments that can simultaneously detect multiple fluorescent markers on a single cell. This capability is crucial for complex studies involving multiple cell populations and biomarkers. These analyzers are widely used in immunology, oncology, and stem cell research, providing detailed insights into cellular functions and interactions. Cell Sorting Flow Cytometers are advanced instruments that not only analyze but also physically separate cells based on their characteristics. This feature is essential for applications such as stem cell research, cancer research, and regenerative medicine, where specific cell populations need to be isolated for further study or therapeutic use. Microfluidic Flow Cytometers represent the latest innovation in the field, utilizing microfluidic technology to miniaturize and integrate various functions of traditional flow cytometers. These devices offer several advantages, including reduced sample and reagent consumption, faster analysis times, and the ability to handle small sample volumes. They are particularly useful in point-of-care diagnostics and resource-limited settings. Each type of flow cytometer plays a crucial role in the global flow cytometry analyzer market, catering to the diverse needs of researchers and clinicians. The continuous advancements in technology and the growing demand for precise and efficient cell analysis are expected to drive the growth and development of this market in the coming years.

Hospitals, Diagnostic Centers, Pharmaceutical, Academic Research Institutes in the Global Flow Cytometry Analyser Market:

The usage of Global Flow Cytometry Analyser Market spans across various sectors, including hospitals, diagnostic centers, pharmaceutical companies, and academic research institutes. In hospitals, flow cytometry analyzers are primarily used for clinical diagnostics and patient monitoring. They play a crucial role in diagnosing and managing diseases such as leukemia, lymphoma, and HIV/AIDS. By providing detailed information about the patient's immune status and cell populations, these analyzers help clinicians make informed decisions about treatment plans and monitor the effectiveness of therapies. Diagnostic centers also rely heavily on flow cytometry analyzers for routine and specialized testing. These centers perform a wide range of tests, including immunophenotyping, cell cycle analysis, and apoptosis detection. The high sensitivity and specificity of flow cytometry make it an invaluable tool for accurate and early disease detection. Pharmaceutical companies use flow cytometry analyzers in drug discovery and development. These instruments are essential for screening potential drug candidates, studying their effects on cell populations, and understanding the mechanisms of action. Flow cytometry provides critical data that helps researchers identify promising compounds and optimize their therapeutic potential. Academic research institutes utilize flow cytometry analyzers for basic and applied research. These instruments are used in various fields, including immunology, cancer research, stem cell research, and microbiology. They enable researchers to study complex cellular processes, identify new biomarkers, and develop innovative therapies. The versatility and precision of flow cytometry make it a valuable tool for advancing scientific knowledge and improving healthcare outcomes. Overall, the widespread adoption of flow cytometry analyzers in these sectors highlights their importance in modern medicine and research. The continuous advancements in technology and the growing demand for accurate and efficient cell analysis are expected to drive the growth of the global flow cytometry analyzer market in the coming years.

Global Flow Cytometry Analyser Market Outlook:

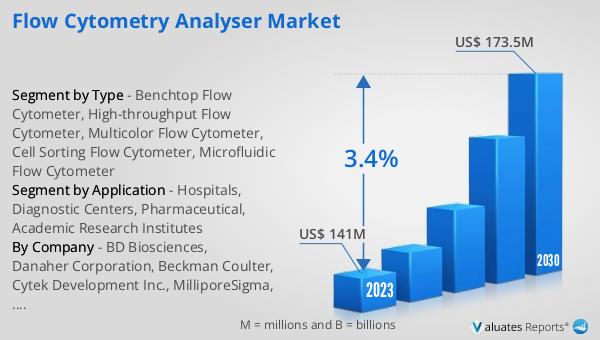

The global Flow Cytometry Analyser market was valued at US$ 141 million in 2023 and is anticipated to reach US$ 173.5 million by 2030, witnessing a CAGR of 3.4% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by various factors such as technological advancements, increasing prevalence of chronic diseases, and the growing demand for early and accurate disease diagnosis. The market's expansion is also supported by the rising adoption of flow cytometry analyzers in clinical and research settings. As healthcare providers and researchers continue to seek more precise and efficient tools for cell analysis, the demand for flow cytometry analyzers is expected to increase. The market's growth is further fueled by the continuous development of new and innovative products that cater to the diverse needs of users. With the increasing focus on personalized medicine and targeted therapies, the importance of flow cytometry analyzers in the global healthcare landscape is set to rise. This market outlook underscores the significant potential for growth and development in the global flow cytometry analyzer market over the forecast period.

| Report Metric | Details |

| Report Name | Flow Cytometry Analyser Market |

| Accounted market size in 2023 | US$ 141 million |

| Forecasted market size in 2030 | US$ 173.5 million |

| CAGR | 3.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | BD Biosciences, Danaher Corporation, Beckman Coulter, Cytek Development Inc., MilliporeSigma, Miltenyi Biotec, Sony Biotechnology Inc., Bio-Rad Laboratories Inc., Luminex Corporation, Agilent |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |