What is Global Hyaluronic Acid Based Dermal Fillers Market?

The Global Hyaluronic Acid Based Dermal Fillers Market refers to the worldwide industry focused on the production, distribution, and application of dermal fillers that use hyaluronic acid as their primary ingredient. Hyaluronic acid is a naturally occurring substance in the human body, primarily found in connective tissues, skin, and eyes. It is known for its ability to retain moisture, making it an ideal component for dermal fillers aimed at reducing wrinkles, fine lines, and other signs of aging. These fillers are injected into the skin to restore volume, improve skin texture, and provide a more youthful appearance. The market encompasses a wide range of products, including single-phase and duplex products, each designed to address specific cosmetic and medical needs. The demand for hyaluronic acid-based dermal fillers is driven by the growing awareness of aesthetic treatments, advancements in cosmetic procedures, and the increasing aging population seeking non-surgical solutions for skin rejuvenation.

Single-phase Product, Duplex Products in the Global Hyaluronic Acid Based Dermal Fillers Market:

Single-phase products and duplex products are two main categories within the Global Hyaluronic Acid Based Dermal Fillers Market, each offering unique benefits and applications. Single-phase products are composed of a homogeneous mixture of hyaluronic acid, which provides a smooth and consistent texture. These fillers are typically used for superficial to moderate wrinkles and fine lines, as they can be easily molded and integrated into the skin. The uniform consistency of single-phase products allows for precise application, making them ideal for areas requiring subtle enhancements, such as the lips and under-eye regions. On the other hand, duplex products consist of a combination of cross-linked and non-cross-linked hyaluronic acid. This dual composition provides a more robust and long-lasting effect, making duplex products suitable for deeper wrinkles, facial contouring, and volumizing larger areas of the face. The cross-linked hyaluronic acid in duplex products offers greater resistance to enzymatic degradation, ensuring that the filler remains effective for an extended period. Additionally, the presence of non-cross-linked hyaluronic acid in duplex products helps to maintain hydration and elasticity in the treated areas. Both single-phase and duplex products are designed to be biocompatible and biodegradable, minimizing the risk of adverse reactions and ensuring that the fillers are gradually absorbed by the body over time. The choice between single-phase and duplex products depends on the specific needs and preferences of the patient, as well as the expertise of the practitioner administering the treatment.

Bootlegging, Sculpting, Fill Scars, Others in the Global Hyaluronic Acid Based Dermal Fillers Market:

The Global Hyaluronic Acid Based Dermal Fillers Market finds extensive usage in various cosmetic and medical applications, including bootlegging, sculpting, filling scars, and other treatments. Bootlegging, in the context of dermal fillers, refers to the enhancement of the buttocks to achieve a fuller and more contoured appearance. Hyaluronic acid-based fillers are injected into the buttocks to add volume and shape, providing a non-surgical alternative to traditional buttock augmentation procedures. Sculpting involves the use of dermal fillers to enhance and define facial features, such as the cheeks, jawline, and chin. By strategically injecting hyaluronic acid-based fillers, practitioners can create a more balanced and harmonious facial profile, addressing issues like asymmetry and loss of volume due to aging. Filling scars is another significant application of hyaluronic acid-based dermal fillers. These fillers can be used to treat various types of scars, including acne scars, surgical scars, and traumatic scars. The hyaluronic acid helps to plump up the depressed areas of the skin, making the scars less noticeable and improving the overall texture and appearance of the skin. Other applications of hyaluronic acid-based dermal fillers include lip augmentation, hand rejuvenation, and the treatment of fine lines and wrinkles around the mouth and eyes. The versatility and effectiveness of hyaluronic acid-based dermal fillers make them a popular choice for individuals seeking minimally invasive cosmetic treatments to enhance their appearance and boost their confidence.

Global Hyaluronic Acid Based Dermal Fillers Market Outlook:

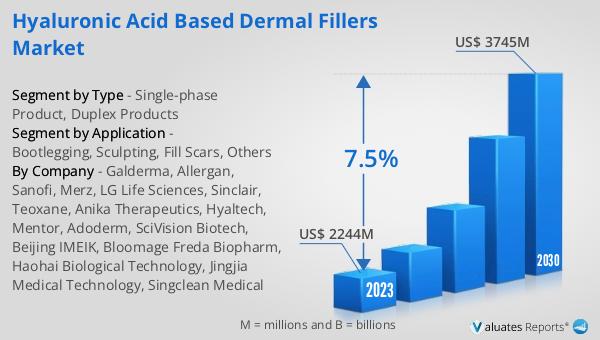

The global Hyaluronic Acid Based Dermal Fillers market is anticipated to expand from US$ 2426.6 million in 2024 to US$ 3745 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 7.5% during the forecast period. The top three global manufacturers collectively hold nearly 45% of the market share. Among the various product types, single-phase products dominate the market, accounting for over 60% of the total share. This growth is driven by the increasing demand for non-surgical aesthetic treatments, advancements in filler technology, and the rising awareness of the benefits of hyaluronic acid-based dermal fillers. The market's expansion is also supported by the growing aging population and the desire for minimally invasive procedures that offer quick results with minimal downtime. As the market continues to evolve, manufacturers are focusing on developing innovative products that cater to the diverse needs of consumers, ensuring that hyaluronic acid-based dermal fillers remain a preferred choice for cosmetic and medical applications.

| Report Metric | Details |

| Report Name | Hyaluronic Acid Based Dermal Fillers Market |

| Accounted market size in 2024 | US$ 2426.6 million |

| Forecasted market size in 2030 | US$ 3745 million |

| CAGR | 7.5 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Galderma, Allergan, Sanofi, Merz, LG Life Sciences, Sinclair, Teoxane, Anika Therapeutics, Hyaltech, Mentor, Adoderm, SciVision Biotech, Beijing IMEIK, Bloomage Freda Biopharm, Haohai Biological Technology, Jingjia Medical Technology, Singclean Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |