What is Global Hands-free Power Liftgate Market?

The Global Hands-free Power Liftgate Market refers to the industry focused on the development, production, and sale of vehicle liftgates that can be operated without the use of hands. These liftgates are typically found on the rear of vehicles and can be opened or closed automatically through various mechanisms such as sensors, remote controls, or foot-activated systems. The primary advantage of hands-free power liftgates is the convenience they offer to users, allowing them to access the trunk or cargo area without having to manually lift or lower the gate. This feature is particularly useful when carrying heavy items or when both hands are occupied. The market for these advanced liftgates has been growing steadily due to increasing consumer demand for convenience and technological advancements in the automotive industry. Additionally, the rise in the production of SUVs and crossovers, which often come equipped with such features, has further fueled the market's expansion.

Kicking, Non-kicking in the Global Hands-free Power Liftgate Market:

In the Global Hands-free Power Liftgate Market, there are primarily two types of systems: kicking and non-kicking. The kicking system is the most prevalent and widely adopted type. It operates through a sensor placed under the rear bumper of the vehicle. When a user makes a kicking motion with their foot under the sensor, the liftgate automatically opens or closes. This system is particularly advantageous for users who have their hands full, as it allows them to access the trunk without needing to put down their belongings. The kicking system is highly favored for its ease of use and reliability, making it a popular choice among consumers and manufacturers alike. On the other hand, the non-kicking system operates through alternative methods such as remote controls, buttons, or proximity sensors. These systems may require the user to press a button on the key fob or the vehicle itself, or they may automatically open when the user approaches the vehicle with the key fob in their possession. While the non-kicking systems also offer hands-free convenience, they may not be as intuitive or user-friendly as the kicking systems. However, they can be beneficial in situations where the kicking motion might not be practical or possible, such as in tight parking spaces or for users with mobility issues. Both kicking and non-kicking systems have their own set of advantages and are designed to cater to different user needs and preferences. The choice between the two often depends on factors such as the vehicle model, user convenience, and cost considerations. As the market continues to evolve, manufacturers are constantly innovating and improving these systems to enhance user experience and meet the growing demand for advanced automotive features.

Sedan, SUV, Other in the Global Hands-free Power Liftgate Market:

The usage of hands-free power liftgates in different types of vehicles such as sedans, SUVs, and others varies based on the specific needs and preferences of the users. In sedans, hands-free power liftgates are particularly useful for urban drivers who often find themselves in situations where they need to access the trunk quickly and conveniently. For instance, when shopping or carrying groceries, the ability to open the trunk without using hands can be a significant advantage. Sedans, being smaller in size compared to SUVs, benefit from the compact and efficient design of hands-free liftgates, which do not require much space to operate. In SUVs, the usage of hands-free power liftgates is even more pronounced. SUVs are often used for family trips, outdoor activities, and transporting larger items. The hands-free feature allows users to easily load and unload cargo without the hassle of manually opening and closing the liftgate. This is especially beneficial when carrying bulky items such as sports equipment, camping gear, or luggage. The higher ground clearance of SUVs also makes the kicking motion more ergonomic and convenient for users. Additionally, the larger cargo space in SUVs means that the liftgate is used more frequently, making the hands-free feature a valuable addition. In other types of vehicles, such as minivans and crossovers, hands-free power liftgates offer similar benefits. Minivans, often used by families, can greatly benefit from the convenience of hands-free liftgates when loading and unloading children, strollers, and other family-related items. Crossovers, which combine features of both sedans and SUVs, also find hands-free liftgates advantageous for their versatility and ease of use. Overall, the adoption of hands-free power liftgates across different vehicle types is driven by the need for convenience, efficiency, and enhanced user experience. As automotive technology continues to advance, the integration of such features is becoming increasingly common, catering to the diverse needs of modern drivers.

Global Hands-free Power Liftgate Market Outlook:

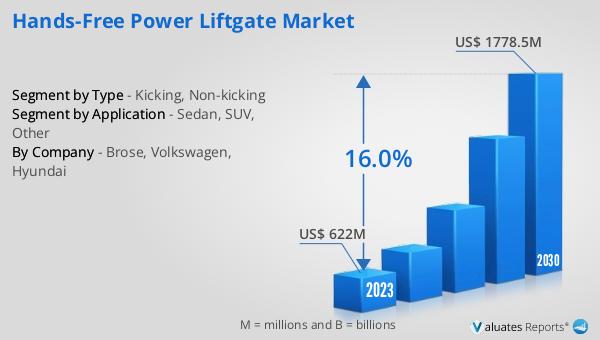

The global Hands-free Power Liftgate market is anticipated to expand significantly, with projections indicating growth from US$ 730 million in 2024 to US$ 1778.5 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 16.0% during the forecast period. The market is dominated by the top two manufacturers, who collectively hold a share exceeding 70%. Europe emerges as the largest market, accounting for approximately 45% of the global share, followed by Asia and North America, each holding around 50% of the market share. Among the various product types, the kicking segment stands out as the largest, commanding a share of over 80%. This robust growth can be attributed to the increasing consumer demand for convenience and advanced automotive features, as well as the rising production of SUVs and crossovers that often come equipped with hands-free power liftgates. The market's expansion is further supported by continuous technological advancements and innovations aimed at enhancing user experience and meeting the evolving needs of modern drivers.

| Report Metric | Details |

| Report Name | Hands-free Power Liftgate Market |

| Accounted market size in 2024 | US$ 730 million |

| Forecasted market size in 2030 | US$ 1778.5 million |

| CAGR | 16.0 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Brose, Volkswagen, Hyundai |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |