What is Global Fuel Cell Electric Vehicles Market?

The Global Fuel Cell Electric Vehicles (FCEV) market is a rapidly evolving sector within the automotive industry. FCEVs are vehicles that use hydrogen fuel cells to generate electricity, which then powers an electric motor. Unlike traditional internal combustion engine vehicles, FCEVs emit only water vapor and heat, making them an environmentally friendly alternative. The market for these vehicles is expanding due to increasing concerns about air pollution and the need for sustainable transportation solutions. Governments and private companies are investing heavily in hydrogen infrastructure, which is crucial for the widespread adoption of FCEVs. Additionally, advancements in fuel cell technology are making these vehicles more efficient and affordable. The global push towards reducing carbon emissions and the growing interest in renewable energy sources are key drivers for the growth of the FCEV market. As more countries commit to zero-emission targets, the demand for FCEVs is expected to rise significantly.

Passenger Vehicles, Commercial Vehicles in the Global Fuel Cell Electric Vehicles Market:

In the Global Fuel Cell Electric Vehicles market, passenger vehicles and commercial vehicles play distinct yet complementary roles. Passenger vehicles, which include cars and SUVs, are primarily designed for personal use. These vehicles are gaining popularity among environmentally conscious consumers who are looking for sustainable alternatives to traditional gasoline-powered cars. The convenience of refueling hydrogen in a matter of minutes, compared to the longer charging times required for battery electric vehicles, makes FCEVs an attractive option for daily commuting and long-distance travel. On the other hand, commercial vehicles, such as buses, trucks, and delivery vans, are essential for public transportation and logistics. The adoption of FCEVs in the commercial sector is driven by the need to reduce operational costs and comply with stringent emission regulations. Hydrogen fuel cells offer a longer range and faster refueling times compared to battery electric vehicles, making them ideal for commercial applications that require high uptime and efficiency. Moreover, the use of FCEVs in public transportation can significantly reduce urban air pollution and improve public health. As cities around the world grapple with traffic congestion and air quality issues, the deployment of hydrogen-powered buses and trucks is seen as a viable solution. Both passenger and commercial FCEVs benefit from the growing hydrogen infrastructure, which includes refueling stations and production facilities. Governments are providing incentives and subsidies to encourage the adoption of FCEVs, further boosting market growth. In summary, while passenger FCEVs cater to individual consumers seeking eco-friendly transportation, commercial FCEVs address the needs of businesses and public services aiming to reduce their carbon footprint and enhance operational efficiency.

For Sales, For Public Lease in the Global Fuel Cell Electric Vehicles Market:

The usage of Global Fuel Cell Electric Vehicles (FCEVs) in sales and public lease markets is gaining traction as more stakeholders recognize the benefits of hydrogen-powered transportation. For sales, FCEVs are being marketed to both individual consumers and businesses. Car manufacturers are highlighting the environmental benefits, such as zero emissions and reduced carbon footprint, to attract eco-conscious buyers. Additionally, the long driving range and quick refueling times are significant selling points compared to battery electric vehicles. Dealerships are also offering attractive financing options and government incentives to make FCEVs more accessible to a broader audience. On the commercial side, companies are investing in FCEV fleets to reduce operational costs and meet sustainability goals. For instance, logistics companies are adopting hydrogen-powered trucks to ensure timely deliveries while minimizing environmental impact. The ability to cover long distances without frequent refueling makes FCEVs ideal for long-haul transportation. In the public lease market, FCEVs are being introduced as a sustainable alternative for public transportation and shared mobility services. Cities are leasing hydrogen-powered buses to provide cleaner and more efficient public transit options. These buses not only reduce air pollution but also offer a quieter and smoother ride compared to traditional diesel buses. Ride-sharing companies are also exploring FCEVs to offer eco-friendly options to their customers. Leasing FCEVs allows these companies to test the technology and infrastructure without the high upfront costs associated with purchasing the vehicles. Moreover, public leasing programs often come with government support, including subsidies and grants, to encourage the adoption of FCEVs. This support helps offset the initial costs and makes it easier for public and private entities to transition to hydrogen-powered transportation. Overall, the use of FCEVs in sales and public lease markets is a promising development that aligns with global efforts to promote sustainable and clean energy solutions.

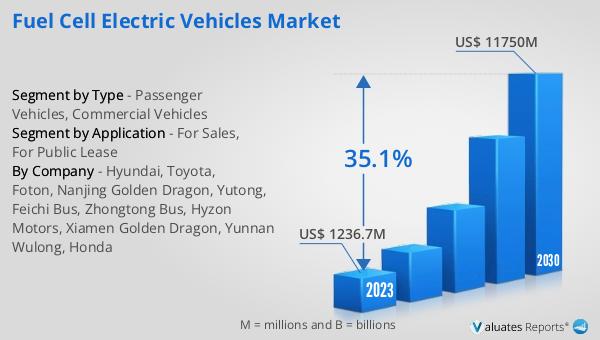

Global Fuel Cell Electric Vehicles Market Outlook:

The global Fuel Cell Electric Vehicles market is anticipated to expand significantly, growing from an estimated US$ 1936.1 million in 2024 to approximately US$ 11750 million by 2030. This growth represents a Compound Annual Growth Rate (CAGR) of 35.1% over the forecast period. Notably, the market is highly concentrated, with the top two manufacturers commanding a substantial share of over 70%. This indicates a competitive landscape where a few key players dominate the market, driving innovation and setting industry standards. The rapid growth of the FCEV market can be attributed to several factors, including advancements in fuel cell technology, increased government support, and a growing awareness of the environmental benefits of hydrogen-powered vehicles. As more countries and companies commit to reducing carbon emissions, the demand for FCEVs is expected to rise, further accelerating market growth. The dominance of the top manufacturers also suggests that these companies are likely to continue leading the way in terms of research and development, production capacity, and market penetration. This concentrated market structure could lead to economies of scale, making FCEVs more affordable and accessible to a broader audience. Overall, the outlook for the global FCEV market is highly optimistic, with significant growth expected in the coming years.

| Report Metric | Details |

| Report Name | Fuel Cell Electric Vehicles Market |

| Accounted market size in 2024 | US$ 1936.1 million |

| Forecasted market size in 2030 | US$ 11750 million |

| CAGR | 35.1 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Hyundai, Toyota, Foton, Nanjing Golden Dragon, Yutong, Feichi Bus, Zhongtong Bus, Hyzon Motors, Xiamen Golden Dragon, Yunnan Wulong, Honda |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |