What is Global Heat Recovery Steam Generator (HRSG) Market?

The Global Heat Recovery Steam Generator (HRSG) Market is a specialized segment within the broader energy and power generation industry. HRSGs are critical components used in combined cycle power plants to improve efficiency by recovering waste heat from gas turbines and converting it into steam, which can then be used to generate additional electricity. This process not only enhances the overall efficiency of power plants but also reduces fuel consumption and greenhouse gas emissions. The market for HRSGs is driven by the increasing demand for energy, the need for more efficient power generation technologies, and stringent environmental regulations. As countries around the world strive to meet their energy needs while minimizing their environmental impact, the adoption of HRSGs is expected to grow. The market encompasses various types of HRSGs, including those designed for different power capacities and applications, making it a diverse and dynamic sector within the energy industry.

Below 50MW, 50MW-100MW, 100MW-300MW, Over 300MW in the Global Heat Recovery Steam Generator (HRSG) Market:

In the Global Heat Recovery Steam Generator (HRSG) Market, HRSGs are categorized based on their power capacity, which includes Below 50MW, 50MW-100MW, 100MW-300MW, and Over 300MW. HRSGs with a capacity Below 50MW are typically used in smaller industrial applications and decentralized power generation systems. These units are compact and designed to meet the specific needs of small-scale operations, providing an efficient solution for recovering waste heat and generating steam. The 50MW-100MW segment caters to medium-sized industrial facilities and power plants. These HRSGs are versatile and can be used in a variety of applications, including cogeneration plants where both electricity and thermal energy are produced. The 100MW-300MW segment represents a significant portion of the HRSG market. These units are commonly used in large industrial complexes and combined cycle power plants. They offer a balance between capacity and efficiency, making them suitable for a wide range of applications. HRSGs in this category are designed to handle substantial amounts of waste heat and convert it into useful steam, thereby enhancing the overall efficiency of power generation systems. The Over 300MW segment includes the largest and most powerful HRSGs, which are used in major power generation facilities. These units are capable of handling massive amounts of waste heat and are integral to the operation of large combined cycle power plants. They play a crucial role in maximizing the efficiency of these plants by recovering waste heat from gas turbines and converting it into steam for additional power generation. Each of these segments has its own unique characteristics and applications, contributing to the overall diversity and growth of the Global HRSG Market.

Power Station, Industrial Production in the Global Heat Recovery Steam Generator (HRSG) Market:

The usage of Global Heat Recovery Steam Generators (HRSGs) in power stations and industrial production is pivotal for enhancing efficiency and reducing environmental impact. In power stations, HRSGs are primarily used in combined cycle power plants. These plants utilize both gas and steam turbines to generate electricity, with HRSGs playing a crucial role in recovering waste heat from the gas turbines. This recovered heat is then used to produce steam, which drives the steam turbines and generates additional electricity. This process significantly improves the overall efficiency of the power plant, reducing fuel consumption and lowering greenhouse gas emissions. The use of HRSGs in power stations is particularly important in regions with high energy demand and stringent environmental regulations, as they help meet energy needs while minimizing the environmental footprint. In industrial production, HRSGs are used in various applications to recover waste heat from industrial processes and convert it into useful steam. This steam can be used for various purposes, including driving turbines for electricity generation, providing process heat, or heating water. Industries such as chemical manufacturing, oil and gas, and food processing often generate significant amounts of waste heat, which can be effectively utilized with HRSGs. By recovering and reusing this waste heat, industries can improve their energy efficiency, reduce operational costs, and decrease their environmental impact. The versatility of HRSGs makes them suitable for a wide range of industrial applications, contributing to their growing adoption in the industrial sector. Overall, the use of HRSGs in power stations and industrial production is a key factor in promoting energy efficiency and sustainability in the global energy landscape.

Global Heat Recovery Steam Generator (HRSG) Market Outlook:

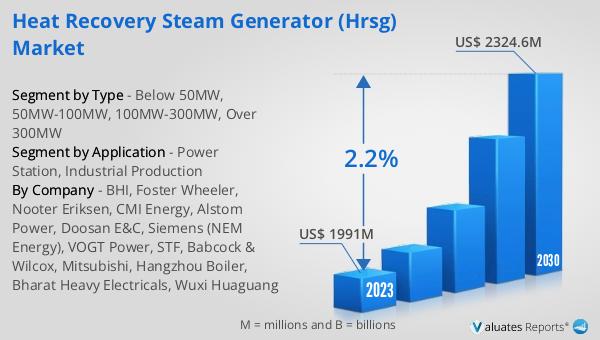

The global Heat Recovery Steam Generator (HRSG) market is anticipated to expand from US$ 2040.1 million in 2024 to US$ 2324.6 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 2.2% over the forecast period. The top four global manufacturers collectively hold a market share exceeding 30%. Among the various product segments, the 100MW-300MW category stands out as the largest, commanding a share of over 55%. This growth is driven by the increasing demand for efficient power generation solutions and the need to comply with stringent environmental regulations. The 100MW-300MW segment's dominance can be attributed to its versatility and suitability for a wide range of applications, including large industrial complexes and combined cycle power plants. These HRSGs offer a balance between capacity and efficiency, making them an attractive option for various stakeholders in the energy sector. As the market continues to evolve, the focus on enhancing efficiency and reducing environmental impact will likely drive further innovation and adoption of HRSGs across different regions and industries.

| Report Metric | Details |

| Report Name | Heat Recovery Steam Generator (HRSG) Market |

| Accounted market size in 2024 | US$ 2040.1 in million |

| Forecasted market size in 2030 | US$ 2324.6 million |

| CAGR | 2.2 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | BHI, Foster Wheeler, Nooter Eriksen, CMI Energy, Alstom Power, Doosan E&C, Siemens (NEM Energy), VOGT Power, STF, Babcock & Wilcox, Mitsubishi, Hangzhou Boiler, Bharat Heavy Electricals, Wuxi Huaguang |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |