What is Global Gas Barbecues Market?

The Global Gas Barbecues Market refers to the worldwide industry focused on the production, distribution, and sale of gas-powered barbecue grills. These grills use propane or natural gas as fuel, offering a convenient and efficient alternative to traditional charcoal grills. The market encompasses a wide range of products, from portable models suitable for small gatherings to large, high-end units designed for serious grilling enthusiasts and commercial use. Factors driving the growth of this market include the increasing popularity of outdoor cooking, advancements in grill technology, and a growing preference for gas grills due to their ease of use and quick heating capabilities. Additionally, the market is influenced by regional preferences, with different types of grills being more popular in certain areas. For instance, North America and Europe have a high demand for gas barbecues, while other regions may still prefer charcoal or electric options. The market also sees innovation in features such as automatic ignition systems, temperature control, and multi-functional cooking capabilities, which enhance the user experience and cater to a diverse range of consumer needs.

Automatic Ignition BBQ, Other BBQ in the Global Gas Barbecues Market:

Automatic Ignition BBQs are a significant segment within the Global Gas Barbecues Market. These grills come equipped with an automatic ignition system, which allows users to start the grill with the push of a button, eliminating the need for matches or lighters. This feature not only adds convenience but also enhances safety, making it easier for users to ignite the grill without the risk of accidental burns. Automatic ignition systems are typically powered by batteries or piezoelectric mechanisms, which generate a spark to ignite the gas. These systems are designed to be reliable and durable, ensuring that the grill can be started quickly and efficiently every time. Other BBQs in the market include traditional gas grills without automatic ignition, which require manual lighting. These grills may be preferred by some users who enjoy the traditional grilling experience or who are looking for a more budget-friendly option. Both types of grills offer various features such as multiple burners, temperature control, and built-in thermometers, catering to different grilling needs and preferences. The choice between automatic ignition and manual lighting often comes down to personal preference, with some users valuing the convenience and ease of use of automatic systems, while others may prefer the simplicity and control of manual lighting. Additionally, the market sees a range of other BBQ options, including portable grills, built-in models for outdoor kitchens, and hybrid grills that combine gas and charcoal capabilities. These options provide consumers with a wide array of choices to suit their specific needs, whether they are looking for a compact grill for camping trips or a high-end model for backyard entertaining. The diversity of products in the Global Gas Barbecues Market ensures that there is a grill to meet every consumer's requirements, from casual weekend grillers to professional chefs.

Family Use, Commercial and Outdoor Activities in the Global Gas Barbecues Market:

The Global Gas Barbecues Market finds extensive usage across various areas, including family use, commercial settings, and outdoor activities. For family use, gas barbecues are a popular choice due to their convenience and ease of operation. Families appreciate the quick start-up and consistent heat that gas grills provide, making it easy to prepare meals for gatherings and everyday dinners. The ability to control the temperature precisely also allows for a wide range of cooking techniques, from searing steaks to slow-cooking ribs. Gas barbecues are often a centerpiece for family gatherings, providing a social and enjoyable cooking experience. In commercial settings, such as restaurants and catering businesses, gas barbecues are valued for their efficiency and reliability. Professional chefs and caterers rely on the consistent heat and large cooking surfaces of commercial-grade gas grills to prepare food quickly and efficiently for large groups. These grills are designed to withstand heavy use and are often equipped with advanced features such as multiple burners, rotisseries, and smoker boxes, allowing for versatile cooking options. The durability and performance of commercial gas barbecues make them a preferred choice for businesses that require high-quality and dependable equipment. Outdoor activities, such as camping, tailgating, and picnics, also benefit from the use of gas barbecues. Portable gas grills are lightweight and easy to transport, making them ideal for outdoor enthusiasts who want to enjoy grilled food on the go. These grills are designed to be compact and easy to set up, with features such as foldable legs and carrying handles. The convenience of gas fuel, which is readily available in portable canisters, adds to the appeal of gas barbecues for outdoor activities. Whether it's a family camping trip or a tailgate party before a big game, gas barbecues provide a convenient and enjoyable way to cook outdoors. Overall, the versatility and convenience of gas barbecues make them a popular choice for a wide range of applications, from family meals to commercial food preparation and outdoor adventures.

Global Gas Barbecues Market Outlook:

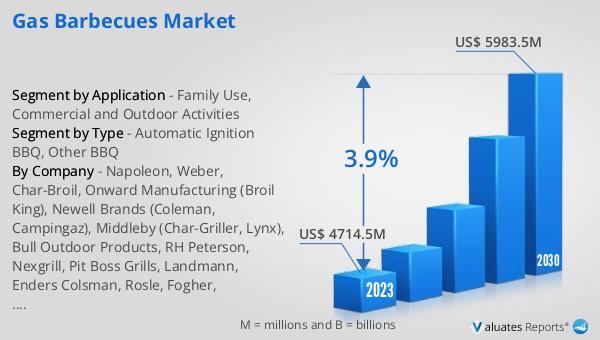

The global Gas Barbecues market is anticipated to expand from US$ 4756.2 million in 2024 to US$ 5983.5 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 3.9% over the forecast period. This growth indicates a steady increase in demand for gas barbecues, driven by factors such as the rising popularity of outdoor cooking and advancements in grill technology. The market is competitive, with the top three players holding approximately 46% of the market share. This concentration suggests that a few key companies dominate the market, likely due to their strong brand recognition, extensive product lines, and innovative features. These leading companies are well-positioned to capitalize on the growing demand for gas barbecues, leveraging their market presence to introduce new products and expand their customer base. The projected growth of the market also highlights the potential for new entrants and smaller players to gain a foothold by offering unique products or targeting niche segments. Overall, the global Gas Barbecues market is poised for steady growth, driven by consumer preferences for convenient and efficient grilling solutions.

| Report Metric | Details |

| Report Name | Gas Barbecues Market |

| Accounted market size in 2024 | US$ 4756.2 million |

| Forecasted market size in 2030 | US$ 5983.5 million |

| CAGR | 3.9 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Char-Broil, Onward Manufacturing (Broil King), Newell Brands (Coleman, Campingaz), Middleby (Char-Griller, Lynx), Bull Outdoor Products, RH Peterson, Nexgrill, Pit Boss Grills, Landmann, Enders Colsman, Rosle, Fogher, Outdoorchef, Electrolux (BeefEater) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |