What is Global Dental Laboratory Workstations Market?

The Global Dental Laboratory Workstations Market refers to the industry that manufactures and supplies workstations specifically designed for dental laboratories. These workstations are essential for dental technicians as they provide a dedicated space equipped with the necessary tools and features to perform various dental procedures, such as creating dental prosthetics, crowns, bridges, and other dental appliances. The market encompasses a wide range of products, including single tables, double tables, and other specialized workstations, each tailored to meet the specific needs of dental professionals. The demand for these workstations is driven by the growing dental industry, advancements in dental technology, and the increasing focus on improving the efficiency and ergonomics of dental laboratories. As dental care becomes more advanced and accessible, the need for high-quality dental laboratory workstations continues to rise, making this market a crucial component of the broader dental industry.

Single Tables, Double Tables, Other in the Global Dental Laboratory Workstations Market:

Single tables, double tables, and other types of workstations play a significant role in the Global Dental Laboratory Workstations Market. Single tables are designed for individual use, providing a compact and efficient workspace for dental technicians. These tables are equipped with essential features such as storage drawers, adjustable lighting, and ergonomic design to ensure comfort and productivity. Single tables are ideal for smaller dental laboratories or for technicians who prefer a dedicated workspace. On the other hand, double tables are designed to accommodate two technicians simultaneously. These tables are larger and often come with additional features such as shared storage space, dual lighting systems, and separate work areas to ensure that both technicians can work efficiently without interfering with each other. Double tables are suitable for larger dental laboratories where multiple technicians need to work together on different tasks. Apart from single and double tables, there are other specialized workstations available in the market. These include modular workstations that can be customized to meet the specific needs of a dental laboratory. Modular workstations offer flexibility in terms of configuration and can be easily expanded or reconfigured as the needs of the laboratory change. Additionally, there are mobile workstations that come with wheels, allowing technicians to move them around the laboratory as needed. These mobile workstations are particularly useful in larger laboratories where technicians need to move between different work areas. Another type of workstation is the technician bench, which is designed to provide a comfortable and efficient workspace for dental technicians. Technician benches are equipped with features such as adjustable height, built-in storage, and ergonomic design to ensure that technicians can work comfortably for extended periods. In addition to these, there are also specialized workstations designed for specific tasks such as casting, polishing, and finishing. These workstations come with specialized tools and features to ensure that the specific task can be performed efficiently and accurately. Overall, the variety of workstations available in the Global Dental Laboratory Workstations Market ensures that dental laboratories can find the right solution to meet their specific needs. Whether it is a single table for individual use, a double table for collaborative work, or a specialized workstation for a specific task, the market offers a wide range of options to choose from. This diversity in product offerings is a testament to the importance of dental laboratory workstations in ensuring the efficiency and productivity of dental laboratories.

Hospital, Clinic in the Global Dental Laboratory Workstations Market:

The usage of Global Dental Laboratory Workstations Market products in hospitals and clinics is crucial for the efficient functioning of dental departments. In hospitals, dental laboratory workstations are used to support a wide range of dental procedures, from routine check-ups to complex surgeries. These workstations provide a dedicated space for dental technicians to create and customize dental prosthetics, crowns, bridges, and other dental appliances. The ergonomic design and specialized features of these workstations ensure that technicians can work comfortably and efficiently, reducing the risk of errors and improving the overall quality of dental care. In addition to supporting dental procedures, these workstations also play a vital role in the training and education of dental professionals. Hospitals often have dental training programs, and having access to high-quality workstations allows students to gain hands-on experience and develop their skills in a real-world setting. In clinics, dental laboratory workstations are equally important. Clinics often have smaller spaces compared to hospitals, and having compact and efficient workstations is essential to maximize the use of available space. Single tables are particularly popular in clinics as they provide a dedicated workspace for individual technicians without taking up too much space. These workstations are equipped with essential features such as storage drawers, adjustable lighting, and ergonomic design to ensure that technicians can work comfortably and efficiently. In addition to single tables, clinics also use double tables and other specialized workstations to support various dental procedures. For example, a clinic may have a dedicated workstation for casting, polishing, or finishing dental appliances. These specialized workstations come with the necessary tools and features to ensure that the specific task can be performed accurately and efficiently. The use of high-quality workstations in clinics not only improves the efficiency and productivity of dental technicians but also enhances the overall patient experience. Patients can receive high-quality dental care in a timely manner, which is essential for maintaining good oral health. Overall, the usage of Global Dental Laboratory Workstations Market products in hospitals and clinics is essential for the efficient functioning of dental departments. These workstations provide a dedicated space for dental technicians to perform various tasks, support the training and education of dental professionals, and improve the overall quality of dental care. Whether it is a hospital with a large dental department or a small clinic with limited space, having access to high-quality dental laboratory workstations is crucial for ensuring the efficiency and productivity of dental technicians and enhancing the overall patient experience.

Global Dental Laboratory Workstations Market Outlook:

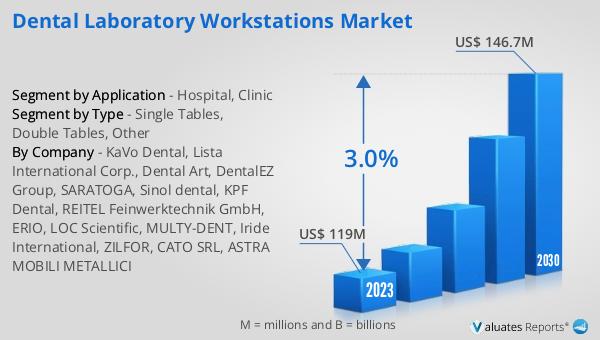

The global Dental Laboratory Workstations market is anticipated to expand from US$ 122.9 million in 2024 to US$ 146.7 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 3.0% during the forecast period. The top four global manufacturers dominate the market, holding approximately 55% of the market share. Europe emerges as the largest market, accounting for around 50% of the total share, followed by China and North America, each holding about 35% of the market. Among the various product segments, Single Tables stand out as the largest, capturing over 55% of the market share. This growth trajectory underscores the increasing demand for dental laboratory workstations, driven by advancements in dental technology and the growing emphasis on improving the efficiency and ergonomics of dental laboratories. The dominance of Europe in this market can be attributed to the region's advanced healthcare infrastructure and the high adoption rate of innovative dental technologies. Similarly, the significant market shares held by China and North America highlight the growing importance of dental care in these regions. The preference for Single Tables indicates a trend towards more compact and efficient workspaces, which are essential for maximizing productivity in dental laboratories. Overall, the projected growth of the global Dental Laboratory Workstations market reflects the ongoing advancements in dental care and the increasing need for high-quality workstations to support the work of dental professionals.

| Report Metric | Details |

| Report Name | Dental Laboratory Workstations Market |

| Accounted market size in 2024 | US$ 122.9 million |

| Forecasted market size in 2030 | US$ 146.7 million |

| CAGR | 3.0 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Dental Art, DentalEZ Group, SARATOGA, Sinol dental, KPF Dental, REITEL Feinwerktechnik GmbH, ERIO, LOC Scientific, MULTY-DENT, Iride International, ZILFOR, CATO SRL, ASTRA MOBILI METALLICI |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |