What is Global POC Diagnostics Market?

The Global Point-of-Care (POC) Diagnostics Market refers to the segment of the healthcare industry that focuses on medical diagnostic testing performed at or near the site of patient care. This market encompasses a wide range of tests that can be conducted outside traditional laboratory settings, such as in clinics, hospitals, and even at home. The primary advantage of POC diagnostics is the rapid turnaround time for test results, which facilitates quicker clinical decision-making and treatment. These tests are designed to be user-friendly, often requiring minimal training to operate, making them accessible to a broader range of healthcare providers. The market includes various types of diagnostic tests, such as blood glucose testing, infectious disease testing, cardiac markers testing, and more. The growing demand for immediate diagnostic results, coupled with advancements in technology, has significantly contributed to the expansion of the Global POC Diagnostics Market. This market is crucial for improving patient outcomes, especially in emergency and critical care settings where timely diagnosis is essential.

Blood Glucose Testing, Infectious Diseases Testing, Cardiac Markers Testing, Coagulation Testing, Pregnancy and Fertility Testing, Blood Gas or Electrolytes Testing, Tumor Markers Testing, Urinalysis Testing, Cholesterol Testing, Others in the Global POC Diagnostics Market:

Blood glucose testing is a cornerstone of the Global POC Diagnostics Market, primarily used by individuals with diabetes to monitor their blood sugar levels. This test is vital for managing diabetes and preventing complications. Infectious diseases testing includes rapid tests for conditions like HIV, influenza, and COVID-19, enabling swift isolation and treatment to curb the spread of infections. Cardiac markers testing is essential for diagnosing heart-related conditions, such as myocardial infarction, by detecting specific proteins released into the bloodstream during a heart attack. Coagulation testing helps in monitoring blood clotting disorders and the effectiveness of anticoagulant therapy. Pregnancy and fertility testing are widely used for confirming pregnancy and assessing fertility status, respectively. Blood gas or electrolytes testing is crucial in critical care settings to evaluate a patient's acid-base balance and electrolyte levels, which are vital for maintaining bodily functions. Tumor markers testing aids in the detection and monitoring of various cancers by identifying specific proteins associated with tumor growth. Urinalysis testing is a common diagnostic tool for detecting urinary tract infections, kidney disease, and other metabolic conditions. Cholesterol testing is essential for assessing cardiovascular risk by measuring the levels of different types of cholesterol in the blood. Other tests in the POC diagnostics market include those for drug abuse, hematology, and infectious diseases, among others. These diverse testing options highlight the versatility and importance of POC diagnostics in modern healthcare.

Clinics, Hospitals, Laboratory, Others in the Global POC Diagnostics Market:

The usage of Global POC Diagnostics Market in clinics is transformative, allowing healthcare providers to deliver immediate and accurate diagnostic results. This rapid turnaround is particularly beneficial in primary care settings, where timely diagnosis can significantly impact patient management and treatment plans. For instance, a patient presenting with symptoms of a respiratory infection can be quickly tested for influenza or COVID-19, enabling the clinician to initiate appropriate treatment without delay. In hospitals, POC diagnostics play a critical role in emergency departments and intensive care units. The ability to perform tests such as blood gas analysis, cardiac markers, and coagulation tests at the bedside ensures that critically ill patients receive prompt and precise care. This immediacy can be life-saving, particularly in acute situations like heart attacks or severe infections. Laboratory settings also benefit from POC diagnostics by streamlining workflows and reducing the burden on central laboratories. While traditional labs handle complex and high-volume testing, POC devices can manage routine and urgent tests, improving overall efficiency. Additionally, POC diagnostics are invaluable in remote or resource-limited settings where access to full-scale laboratory facilities is restricted. Mobile clinics and field hospitals often rely on these portable and easy-to-use devices to provide essential diagnostic services to underserved populations. The versatility and accessibility of POC diagnostics make them a crucial component of modern healthcare delivery, enhancing patient outcomes across various settings.

Global POC Diagnostics Market Outlook:

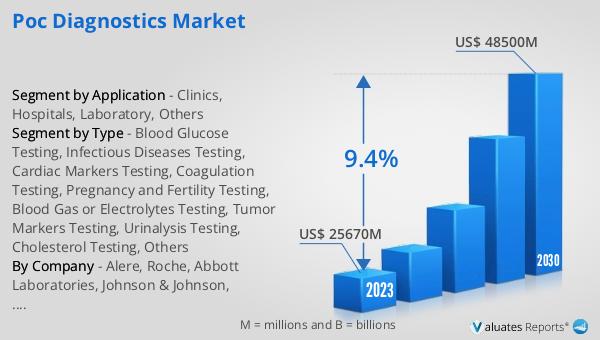

The global POC Diagnostics market is anticipated to expand significantly, growing from US$ 28,290 million in 2024 to US$ 48,500 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 9.4% during the forecast period. This growth trajectory underscores the increasing demand for rapid and accurate diagnostic solutions across the healthcare spectrum. Notably, the market is dominated by the top four manufacturers, who collectively hold a market share exceeding 50%. Among the various product segments, blood glucose testing stands out as the largest, accounting for over 45% of the market share. This dominance is attributed to the widespread prevalence of diabetes and the critical need for continuous blood glucose monitoring to manage the condition effectively. The robust growth of the POC diagnostics market highlights the pivotal role these tests play in enhancing patient care by providing timely and actionable diagnostic information.

| Report Metric | Details |

| Report Name | POC Diagnostics Market |

| Accounted market size in 2024 | US$ 28290 million |

| Forecasted market size in 2030 | US$ 48500 million |

| CAGR | 9.4 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Abbott Laboratories, Johnson & Johnson, Siemens Healthcare, Danaher, Bayer Healthcare, Beckman Coulter, Nipro Diagnostics, Bio-Rad Laboratories, Nova Biomedical, BioMerieux, Quidel, Helena Laboratories, OraSure Technologies, Accriva, Abaxis, Chembio Diagnostics, Trinity Biotech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |