What is Global Blood and Fluid Warmer Market?

The Global Blood and Fluid Warmer Market refers to the industry focused on devices designed to warm blood and other fluids before they are administered to patients. These devices are crucial in medical settings to prevent hypothermia, which can occur when cold fluids are introduced into the body. Hypothermia can lead to various complications, including impaired coagulation, increased risk of infection, and prolonged hospital stays. Blood and fluid warmers are used in a variety of medical environments, such as operating rooms, intensive care units (ICUs), emergency rooms, and even in military applications. The market for these devices is expanding due to the increasing number of surgeries, rising incidences of trauma cases, and growing awareness about the importance of maintaining normothermia in patients. Technological advancements and the development of portable and user-friendly devices are also contributing to the market's growth. The market is segmented based on product type, application, and region, with North America currently holding the largest share.

Portable Type, Fixed Type in the Global Blood and Fluid Warmer Market:

In the Global Blood and Fluid Warmer Market, products are generally categorized into two main types: Portable Type and Fixed Type. Portable blood and fluid warmers are designed for mobility and ease of use, making them ideal for emergency situations, military applications, and field hospitals. These devices are compact, lightweight, and often battery-operated, allowing healthcare providers to administer warm fluids quickly and efficiently in various settings. Portable warmers are particularly useful in ambulances and during patient transport, where immediate access to warming devices can be life-saving. On the other hand, Fixed Type blood and fluid warmers are typically installed in permanent medical facilities such as hospitals and clinics. These devices are usually more robust and can handle higher volumes of fluids, making them suitable for operating rooms, ICUs, and recovery rooms. Fixed warmers are often integrated into the hospital's infrastructure, providing a reliable and consistent source of warmed fluids. Both types of warmers play a crucial role in maintaining patient body temperature, but their applications differ based on the setting and specific medical needs. The choice between portable and fixed warmers depends on factors such as the volume of fluids to be warmed, the urgency of the situation, and the mobility required. Technological advancements have led to the development of more efficient and user-friendly devices in both categories, enhancing their effectiveness and ease of use.

Operating Room, Recovery Room (PACU), ICU, Emergency Room, Military Applications, Other in the Global Blood and Fluid Warmer Market:

The usage of blood and fluid warmers in various medical settings is essential for patient care and recovery. In operating rooms, these devices are used to warm blood and fluids before they are administered to patients undergoing surgery. This helps maintain the patient's body temperature, reducing the risk of hypothermia and associated complications. In recovery rooms, also known as Post-Anesthesia Care Units (PACU), blood and fluid warmers are used to stabilize patients' body temperatures as they recover from anesthesia. This is crucial for ensuring a smooth recovery process and preventing any post-operative complications. In Intensive Care Units (ICUs), blood and fluid warmers are used for critically ill patients who require continuous monitoring and care. These devices help maintain normothermia, which is vital for the patient's overall stability and recovery. In emergency rooms, blood and fluid warmers are used to quickly warm fluids for patients who have experienced trauma or severe blood loss. This rapid warming can be life-saving and is a critical component of emergency care. Military applications also rely heavily on portable blood and fluid warmers, as they are essential for treating injured soldiers in the field. These devices provide a quick and efficient way to administer warm fluids, which can be crucial in combat situations. Other settings where blood and fluid warmers are used include ambulances, outpatient clinics, and home healthcare environments. In all these settings, the primary goal is to maintain the patient's body temperature and prevent hypothermia, thereby improving patient outcomes and reducing the risk of complications.

Global Blood and Fluid Warmer Market Outlook:

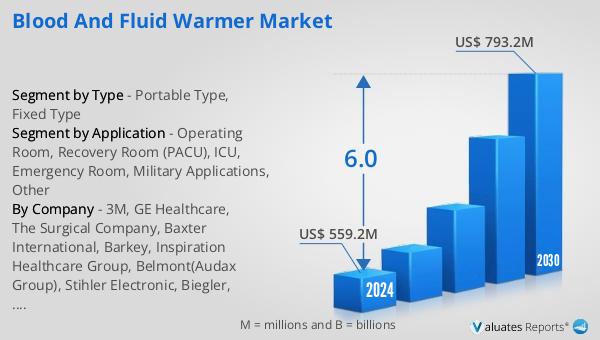

The global Blood and Fluid Warmer market is anticipated to expand from US$ 559.2 million in 2024 to US$ 793.2 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 6.0% during the forecast period. The top five global manufacturers collectively hold about 58% of the market share. North America stands as the largest market, accounting for approximately 50% of the total share, followed by Europe and China, which together hold over 40% of the market. Among the product types, the Portable Type segment is the largest, comprising over 62% of the market share. This growth can be attributed to the increasing demand for efficient and user-friendly medical devices, as well as the rising number of surgeries and trauma cases worldwide. The market's expansion is also driven by technological advancements and the growing awareness about the importance of maintaining normothermia in patients. As the market continues to grow, it is expected to see further innovations and improvements in both portable and fixed blood and fluid warmers, enhancing their effectiveness and ease of use in various medical settings.

| Report Metric | Details |

| Report Name | Blood and Fluid Warmer Market |

| Accounted market size in 2024 | US$ 559.2 million |

| Forecasted market size in 2030 | US$ 793.2 million |

| CAGR | 6.0 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | 3M, GE Healthcare, The Surgical Company, Baxter International, Barkey, Inspiration Healthcare Group, Belmont(Audax Group), Stihler Electronic, Biegler, Zhongzhu Healthcare, Emit Corporation, Foshan Keewell, Sino Medical-Device Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |