What is Global eReader Market?

The global eReader market is a dynamic and evolving sector that focuses on the production and distribution of electronic reading devices. These devices, commonly known as eReaders, are designed to replicate the experience of reading a physical book while offering the convenience of digital technology. eReaders typically feature e-ink displays, which are easier on the eyes compared to traditional screens, and they often come with features like adjustable font sizes, built-in dictionaries, and the ability to store thousands of books. The market encompasses a wide range of products from various manufacturers, each offering different sizes, features, and price points to cater to diverse consumer needs. The growth of the eReader market is driven by factors such as increasing digital literacy, the convenience of carrying multiple books in one device, and the rising popularity of eBooks. Additionally, the market is influenced by technological advancements, such as improved battery life and enhanced display quality, which make eReaders more appealing to a broader audience. As a result, the global eReader market continues to expand, offering numerous opportunities for both consumers and manufacturers.

Below 5 Inches, 6 Inches, 8 Inches, 9.7 Inches, Above 9.7 Inches in the Global eReader Market:

The global eReader market offers a variety of device sizes to cater to different user preferences and needs. Below 5 inches eReaders are compact and highly portable, making them ideal for users who prioritize mobility and convenience. These smaller devices are perfect for on-the-go reading, fitting easily into pockets or small bags. However, their smaller screen size may not be suitable for extended reading sessions or for users who prefer larger text. The 6 inches eReaders are among the most popular sizes, striking a balance between portability and readability. They are large enough to provide a comfortable reading experience while still being compact enough to carry around easily. This size is often favored by casual readers and those who read during commutes. Moving up, the 8 inches eReaders offer a larger display, which enhances the reading experience by providing more screen real estate for text and images. This size is particularly beneficial for reading graphic novels, magazines, and other visually rich content. The 9.7 inches eReaders are even larger, offering a tablet-like experience. These devices are ideal for users who read extensively and prefer a larger screen to reduce eye strain. They are also suitable for academic and professional use, where detailed diagrams and large documents are common. Finally, eReaders above 9.7 inches cater to niche markets, such as professionals and academics who require a large display for technical documents, blueprints, or detailed illustrations. These devices are less portable but offer unparalleled readability and functionality for specific use cases. Each size category within the global eReader market addresses different user needs, ensuring that there is a suitable device for every type of reader.

Children, Adults in the Global eReader Market:

The usage of eReaders in the global market varies significantly between children and adults, each group having distinct needs and preferences. For children, eReaders serve as an educational tool that can make learning more engaging and interactive. Many eReaders designed for children come with features like parental controls, educational games, and access to a wide range of age-appropriate books. These devices can help foster a love for reading from a young age, offering interactive elements such as read-aloud functions and animated illustrations that capture children's attention. Additionally, eReaders can support children with learning disabilities by providing customizable text sizes, fonts, and background colors to enhance readability. For adults, eReaders offer a convenient and versatile reading experience. They are particularly popular among avid readers who appreciate the ability to carry an entire library in a single device. Features such as adjustable font sizes, built-in dictionaries, and note-taking capabilities enhance the reading experience, making it easier for adults to read comfortably for extended periods. eReaders are also beneficial for professionals and academics who need to read and annotate large volumes of text. The ability to search for specific terms, highlight important sections, and make notes directly on the device streamlines the research and study process. Furthermore, eReaders are environmentally friendly, reducing the need for physical books and contributing to sustainability efforts. In summary, while children benefit from the educational and interactive features of eReaders, adults appreciate the convenience, versatility, and enhanced reading experience these devices offer.

Global eReader Market Outlook:

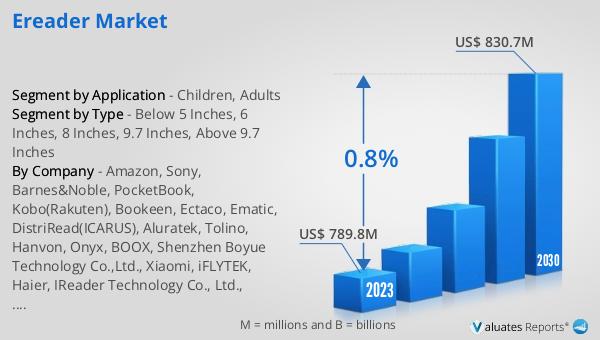

The global eReader market is anticipated to expand from $794.2 million in 2024 to $830.7 million by 2030, reflecting a modest Compound Annual Growth Rate (CAGR) of 0.8% over the forecast period. The top five manufacturers dominate the market, holding a collective share of over 90%. China and North America represent the largest markets, accounting for more than 68% of the global share, followed by Europe with approximately 18%. Among the various product segments, the 8 inches eReaders stand out as the largest, capturing over 45% of the market share. This data underscores the significant role of major manufacturers and key regions in driving the market, as well as the popularity of mid-sized eReaders among consumers.

| Report Metric | Details |

| Report Name | eReader Market |

| Accounted market size in 2024 | US$ 794.2 million |

| Forecasted market size in 2030 | US$ 830.7 million |

| CAGR | 0.8 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Barnes&Noble, PocketBook, Kobo(Rakuten), Bookeen, Ectaco, Ematic, DistriRead(ICARUS), Aluratek, Tolino, Hanvon, Onyx, BOOX, Shenzhen Boyue Technology Co.,Ltd., Xiaomi, iFLYTEK, Haier, IReader Technology Co., Ltd., Huawei |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |