What is Global Aprotinin Market?

The global Aprotinin market is a specialized segment within the pharmaceutical and biotechnology industries, focusing on the production and distribution of Aprotinin, a protease inhibitor derived from bovine lung tissue. Aprotinin is primarily used to reduce bleeding during complex surgeries, such as cardiac procedures, by inhibiting enzymes that break down blood clots. The market for Aprotinin has seen significant growth due to its critical role in surgical settings, where minimizing blood loss is paramount. Additionally, advancements in biotechnology have led to the development of recombinant Aprotinin, which is produced using genetically engineered cells, offering a more consistent and potentially safer alternative to the bovine-derived version. The global demand for Aprotinin is driven by the increasing number of surgical procedures, advancements in medical technology, and the growing emphasis on patient safety and outcomes. The market is characterized by a few key players who dominate the production and distribution channels, ensuring the availability of high-quality Aprotinin for medical use.

Aprotinin (From bovine lung), Recombinant Aprotinin in the Global Aprotinin Market:

Aprotinin, originally derived from bovine lung tissue, has been a cornerstone in the medical field for its ability to inhibit proteolytic enzymes, thereby reducing blood loss during surgeries. This bovine-derived Aprotinin works by blocking the activity of enzymes like trypsin and plasmin, which are involved in the breakdown of blood clots. However, the reliance on animal sources has raised concerns about variability in product quality and the potential for allergic reactions. To address these issues, recombinant Aprotinin has been developed. Recombinant Aprotinin is produced using genetically modified cells, typically yeast or bacteria, which are engineered to produce the Aprotinin protein. This method offers several advantages, including a more consistent product, reduced risk of contamination, and the elimination of animal-derived impurities. The recombinant version has gained traction in the global market due to these benefits, making it a preferred choice for many medical applications. The production process involves inserting the gene responsible for Aprotinin production into the host cells, which then express the protein. The protein is subsequently harvested, purified, and formulated for medical use. This biotechnological advancement has not only improved the safety profile of Aprotinin but also ensured a stable supply to meet the growing demand. The global Aprotinin market, therefore, includes both bovine-derived and recombinant products, catering to different needs and preferences within the medical community. The choice between the two often depends on factors such as cost, availability, and specific clinical requirements. As the market continues to evolve, ongoing research and development efforts aim to further enhance the efficacy and safety of Aprotinin, ensuring its continued relevance in modern medicine.

Pharmaceuticals, Scientific Research and Experiment in the Global Aprotinin Market:

The global Aprotinin market finds extensive applications in various fields, including pharmaceuticals, scientific research, and experimental studies. In the pharmaceutical industry, Aprotinin is primarily used as a hemostatic agent during surgeries to reduce blood loss. Its ability to inhibit proteolytic enzymes makes it invaluable in complex surgical procedures, particularly in cardiac surgeries where controlling bleeding is crucial. The use of Aprotinin in these settings has been shown to improve patient outcomes by minimizing the need for blood transfusions and reducing the risk of postoperative complications. In scientific research, Aprotinin is employed as a tool to study protease activity and enzyme inhibition. Researchers use it to investigate the mechanisms of proteolytic enzymes and their role in various physiological and pathological processes. This research is essential for developing new therapeutic strategies for diseases involving protease dysregulation, such as cancer and inflammatory conditions. Aprotinin's ability to inhibit a broad spectrum of proteases makes it a versatile reagent in biochemical and molecular biology experiments. In experimental studies, Aprotinin is used to explore its potential therapeutic applications beyond its traditional use in surgery. For instance, researchers are investigating its role in treating conditions like acute pancreatitis, where protease inhibition could mitigate tissue damage. Additionally, Aprotinin is being studied for its potential in preserving organs for transplantation by reducing protease-mediated tissue degradation. These experimental applications highlight the versatility of Aprotinin and its potential to address unmet medical needs. Overall, the global Aprotinin market serves as a critical component in advancing medical science and improving patient care across various domains.

Global Aprotinin Market Outlook:

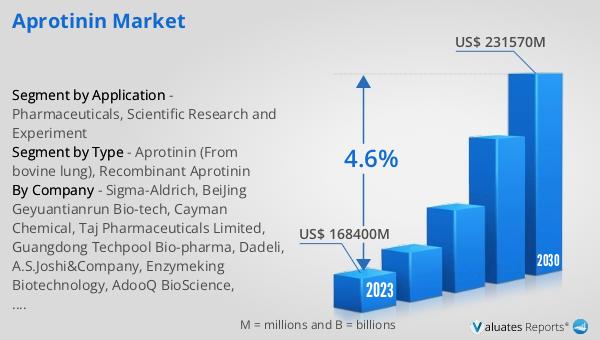

The global Aprotinin market is anticipated to expand from USD 176.8 billion in 2024 to USD 231.57 billion by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 4.6% throughout the forecast period. The top four global manufacturers collectively hold a market share exceeding 25%. India emerges as the largest market, accounting for approximately 20% of the total share, followed by China and North America, each contributing around 35%. In terms of product segmentation, Aprotinin derived from bovine lung represents the largest segment, comprising nearly 80% of the market share. This growth trajectory underscores the increasing demand for Aprotinin, driven by its critical role in surgical procedures and its expanding applications in pharmaceuticals and scientific research. The dominance of bovine-derived Aprotinin highlights its established efficacy and widespread acceptance in the medical community. However, the market dynamics are also influenced by the growing adoption of recombinant Aprotinin, which offers a more consistent and potentially safer alternative. As the market continues to evolve, the interplay between these two product types will shape the future landscape of the global Aprotinin market.

| Report Metric | Details |

| Report Name | Aprotinin Market |

| Accounted market size in 2024 | US$ 176800 in million |

| Forecasted market size in 2030 | US$ 231570 million |

| CAGR | 4.6 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Cayman Chemical, Taj Pharmaceuticals Limited, Guangdong Techpool Bio-pharma, Dadeli, A.S.Joshi&Company, Enzymeking Biotechnology, AdooQ BioScience, ProSpec, Yaxin Biotechnology, AMRESCO, PanReac AppliChem, Runhao |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |