What is Global Women's Oncology Detection Solutions Market?

The Global Women's Oncology Detection Solutions Market focuses on technologies and methods used to detect cancers that predominantly affect women, such as breast, ovarian, and cervical cancers. This market encompasses a range of diagnostic tools and solutions designed to identify cancer at its earliest stages, thereby improving treatment outcomes and survival rates. These solutions include advanced imaging techniques, molecular diagnostics, and various types of biopsies. The market is driven by the increasing prevalence of cancer among women, advancements in medical technology, and a growing awareness of the importance of early detection. Additionally, government initiatives and funding for cancer research and screening programs contribute to the market's growth. The ultimate goal of these detection solutions is to provide accurate, timely, and non-invasive methods for diagnosing cancer, which can lead to more effective treatment plans and better patient outcomes. As the demand for early and precise cancer detection continues to rise, the Global Women's Oncology Detection Solutions Market is expected to expand, offering new opportunities for innovation and development in the healthcare sector.

Tissue Test, Blood Test, Others in the Global Women's Oncology Detection Solutions Market:

In the Global Women's Oncology Detection Solutions Market, various diagnostic methods are employed to detect cancer, including tissue tests, blood tests, and other innovative techniques. Tissue tests, also known as biopsies, involve the removal of a small sample of tissue from the suspected area, which is then examined under a microscope by a pathologist. This method is considered the gold standard for cancer diagnosis as it provides detailed information about the type and stage of cancer. There are different types of biopsies, such as needle biopsies, surgical biopsies, and endoscopic biopsies, each suited for specific situations and types of cancer. Blood tests, on the other hand, are less invasive and can provide valuable information about the presence of cancer through the detection of specific biomarkers or genetic mutations associated with cancer. These tests can include complete blood counts (CBC), tumor marker tests, and liquid biopsies, which analyze circulating tumor DNA (ctDNA) in the blood. Blood tests are particularly useful for monitoring cancer progression and response to treatment. Other diagnostic methods in the market include imaging techniques like mammography, ultrasound, MRI, and PET scans, which help visualize tumors and assess their size and spread. Additionally, advancements in molecular diagnostics and genetic testing have paved the way for personalized medicine, allowing for more targeted and effective treatment plans based on an individual's genetic makeup. These innovative approaches are crucial in the early detection and management of cancer, ultimately improving patient outcomes and survival rates. As technology continues to evolve, the Global Women's Oncology Detection Solutions Market is expected to see further advancements in diagnostic methods, offering more accurate, efficient, and less invasive options for cancer detection.

Hospital, Third-party Medical Examination Institution, Others in the Global Women's Oncology Detection Solutions Market:

The usage of Global Women's Oncology Detection Solutions Market spans various healthcare settings, including hospitals, third-party medical examination institutions, and other specialized facilities. In hospitals, these detection solutions are integral to the oncology departments, where they are used for screening, diagnosing, and monitoring cancer in female patients. Hospitals often have access to a wide range of diagnostic tools, including advanced imaging equipment, laboratory services for tissue and blood tests, and specialized personnel such as oncologists, radiologists, and pathologists. The comprehensive nature of hospital-based care allows for a multidisciplinary approach to cancer detection and treatment, ensuring that patients receive timely and accurate diagnoses followed by appropriate treatment plans. Third-party medical examination institutions, such as diagnostic labs and imaging centers, also play a crucial role in the market. These institutions often provide specialized diagnostic services that may not be available in smaller healthcare facilities. They offer a range of tests, including genetic and molecular diagnostics, which are essential for early cancer detection and personalized treatment plans. These third-party institutions often collaborate with hospitals and clinics to provide comprehensive diagnostic services, ensuring that patients have access to the latest technologies and expertise. Other specialized facilities, such as cancer research centers and women's health clinics, also utilize oncology detection solutions to focus on specific aspects of cancer care. These facilities often engage in clinical trials and research studies to develop and validate new diagnostic methods and treatments. They play a vital role in advancing the field of oncology by contributing to the development of innovative detection solutions and improving the overall quality of cancer care. The widespread use of oncology detection solutions across various healthcare settings highlights the importance of early and accurate cancer detection in improving patient outcomes and survival rates. As the demand for these solutions continues to grow, the Global Women's Oncology Detection Solutions Market is expected to expand, offering new opportunities for innovation and development in the healthcare sector.

Global Women's Oncology Detection Solutions Market Outlook:

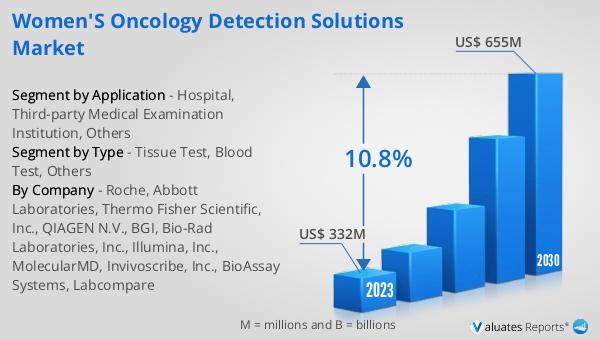

The global Women's Oncology Detection Solutions market was valued at US$ 332 million in 2023 and is anticipated to reach US$ 655 million by 2030, witnessing a CAGR of 10.8% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for advanced diagnostic tools and technologies that can accurately detect cancers affecting women at an early stage. The market's expansion is driven by several factors, including the rising prevalence of cancer among women, advancements in medical technology, and growing awareness of the importance of early detection. Additionally, government initiatives and funding for cancer research and screening programs contribute to the market's growth. As more healthcare providers adopt these advanced detection solutions, the market is expected to see continued innovation and development, leading to more effective and less invasive diagnostic methods. The ultimate goal of these solutions is to improve patient outcomes by providing timely and accurate diagnoses, enabling more targeted and effective treatment plans. As the market continues to grow, it will offer new opportunities for healthcare providers, researchers, and technology developers to collaborate and advance the field of oncology detection.

| Report Metric | Details |

| Report Name | Women's Oncology Detection Solutions Market |

| Accounted market size in 2023 | US$ 332 million |

| Forecasted market size in 2030 | US$ 655 million |

| CAGR | 10.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Roche, Abbott Laboratories, Thermo Fisher Scientific, Inc., QIAGEN N.V., BGI, Bio-Rad Laboratories, Inc., Illumina, Inc., MolecularMD, Invivoscribe, Inc., BioAssay Systems, Labcompare |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |