What is Global Organic Rice Starch Market?

The Global Organic Rice Starch Market refers to the worldwide trade and consumption of rice starch that is produced organically, meaning it is grown without the use of synthetic pesticides, fertilizers, or genetically modified organisms (GMOs). Organic rice starch is derived from rice grains and is used as a natural thickening agent, stabilizer, and texturizer in various industries. This market is driven by the increasing consumer demand for organic and clean-label products, as well as the growing awareness of the health benefits associated with organic foods. The market encompasses a wide range of applications, including food and beverages, pharmaceuticals, cosmetics, and industrial uses. The global organic rice starch market is characterized by a diverse range of products, including different grades and types of rice starch, catering to the specific needs of various industries. The market is also influenced by factors such as changing consumer preferences, regulatory standards, and advancements in production technologies.

Food Grade, Industrial Grade in the Global Organic Rice Starch Market:

In the Global Organic Rice Starch Market, there are two primary grades of rice starch: Food Grade and Industrial Grade. Food Grade organic rice starch is specifically processed to meet the stringent safety and quality standards required for human consumption. It is widely used in the food and beverage industry as a natural thickening agent, stabilizer, and texturizer. Food Grade organic rice starch is preferred for its clean-label attributes, as it is free from synthetic additives and GMOs. It is commonly used in products such as baby foods, dairy products, sauces, soups, and gluten-free baked goods. The demand for Food Grade organic rice starch is driven by the increasing consumer preference for organic and natural ingredients, as well as the growing awareness of the health benefits associated with organic foods. On the other hand, Industrial Grade organic rice starch is used in various non-food applications, including the pharmaceutical, cosmetic, and chemical industries. In the pharmaceutical industry, it is used as a binder and disintegrant in tablet formulations, as well as a stabilizer in liquid medications. In the cosmetic industry, it is used in products such as powders, creams, and lotions for its absorbent and texturizing properties. In the chemical industry, it is used as a biodegradable and eco-friendly alternative to synthetic chemicals in various applications, including adhesives, coatings, and packaging materials. The demand for Industrial Grade organic rice starch is driven by the increasing focus on sustainability and the growing preference for natural and biodegradable ingredients in various industrial applications. Both Food Grade and Industrial Grade organic rice starch are subject to strict regulatory standards to ensure their safety and quality. The production of organic rice starch involves careful selection of organic rice varieties, as well as adherence to organic farming practices and processing methods. The market for both grades of organic rice starch is influenced by factors such as changing consumer preferences, regulatory standards, and advancements in production technologies. The growing demand for organic and clean-label products, coupled with the increasing awareness of the health and environmental benefits associated with organic foods, is expected to drive the growth of the Global Organic Rice Starch Market in the coming years.

Food and Drinks, Chemical Industry, Other in the Global Organic Rice Starch Market:

The Global Organic Rice Starch Market finds extensive usage in various areas, including Food and Drinks, the Chemical Industry, and other sectors. In the Food and Drinks sector, organic rice starch is widely used as a natural thickening agent, stabilizer, and texturizer. It is preferred for its clean-label attributes, as it is free from synthetic additives and GMOs. Organic rice starch is commonly used in baby foods, dairy products, sauces, soups, and gluten-free baked goods. It helps improve the texture, consistency, and shelf life of these products, while also providing a natural and healthy alternative to synthetic ingredients. The demand for organic rice starch in the Food and Drinks sector is driven by the increasing consumer preference for organic and natural ingredients, as well as the growing awareness of the health benefits associated with organic foods. In the Chemical Industry, organic rice starch is used as a biodegradable and eco-friendly alternative to synthetic chemicals in various applications. It is used in the production of adhesives, coatings, and packaging materials, where it provides excellent binding, film-forming, and stabilizing properties. The use of organic rice starch in the Chemical Industry is driven by the increasing focus on sustainability and the growing preference for natural and biodegradable ingredients. In addition to the Food and Drinks and Chemical Industry sectors, organic rice starch is also used in other areas, including the pharmaceutical and cosmetic industries. In the pharmaceutical industry, it is used as a binder and disintegrant in tablet formulations, as well as a stabilizer in liquid medications. In the cosmetic industry, it is used in products such as powders, creams, and lotions for its absorbent and texturizing properties. The demand for organic rice starch in these sectors is driven by the increasing focus on natural and sustainable ingredients, as well as the growing awareness of the health and environmental benefits associated with organic products. Overall, the Global Organic Rice Starch Market is characterized by a diverse range of applications, catering to the specific needs of various industries. The market is influenced by factors such as changing consumer preferences, regulatory standards, and advancements in production technologies. The growing demand for organic and clean-label products, coupled with the increasing awareness of the health and environmental benefits associated with organic foods, is expected to drive the growth of the Global Organic Rice Starch Market in the coming years.

Global Organic Rice Starch Market Outlook:

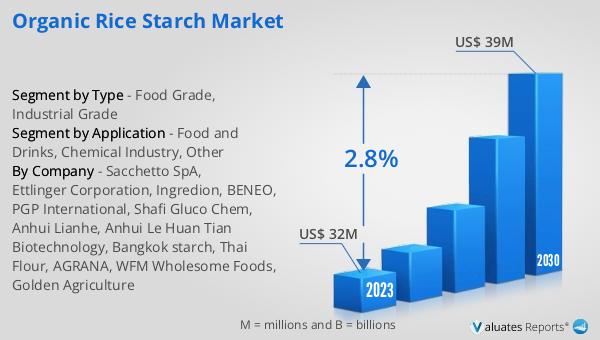

The global Organic Rice Starch market was valued at US$ 32 million in 2023 and is anticipated to reach US$ 39 million by 2030, witnessing a CAGR of 2.8% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the organic rice starch industry over the next several years. The valuation of US$ 32 million in 2023 reflects the current demand and market penetration of organic rice starch products across various sectors. The projected increase to US$ 39 million by 2030 signifies a growing acceptance and preference for organic rice starch, driven by factors such as rising consumer awareness about the benefits of organic products, increasing demand for clean-label ingredients, and the expanding application of organic rice starch in diverse industries. The compound annual growth rate (CAGR) of 2.8% underscores the market's potential for consistent growth, supported by ongoing advancements in production technologies, regulatory support for organic farming practices, and the continuous shift towards sustainable and eco-friendly products. This market outlook provides a positive indication of the future prospects for the Global Organic Rice Starch Market, highlighting the opportunities for stakeholders to capitalize on the growing demand for organic and natural ingredients.

| Report Metric | Details |

| Report Name | Organic Rice Starch Market |

| Accounted market size in 2023 | US$ 32 million |

| Forecasted market size in 2030 | US$ 39 million |

| CAGR | 2.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Sacchetto SpA, Ettlinger Corporation, Ingredion, BENEO, PGP International, Shafi Gluco Chem, Anhui Lianhe, Anhui Le Huan Tian Biotechnology, Bangkok starch, Thai Flour, AGRANA, WFM Wholesome Foods, Golden Agriculture |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |