What is Global Recombinant Carboxypeptidase B Market?

The Global Recombinant Carboxypeptidase B Market is a specialized segment within the broader biotechnology and pharmaceutical industries. Recombinant Carboxypeptidase B is an enzyme that plays a crucial role in protein processing and modification. It is produced using recombinant DNA technology, which involves inserting the gene responsible for the enzyme into a host organism, typically bacteria or yeast, to produce the enzyme in large quantities. This enzyme is essential in various applications, including the production of insulin, where it helps in the removal of specific amino acids from the insulin precursor to produce the active form of the hormone. The market for recombinant Carboxypeptidase B is driven by the increasing demand for biopharmaceuticals, advancements in biotechnology, and the growing need for efficient and cost-effective enzyme production methods. The market is characterized by the presence of several key players who are continuously investing in research and development to improve the efficiency and yield of recombinant Carboxypeptidase B production. Additionally, the market is witnessing a growing trend towards the use of recombinant enzymes in various industrial applications, further driving its growth.

>90%, >95%, Others in the Global Recombinant Carboxypeptidase B Market:

In the Global Recombinant Carboxypeptidase B Market, products are often categorized based on their purity levels, such as >90%, >95%, and others. These purity levels indicate the percentage of the enzyme that is free from contaminants or other proteins. The >90% purity level is typically used in applications where a high degree of purity is not critical, but the enzyme still needs to be relatively free from impurities to function effectively. This level of purity is often sufficient for certain industrial applications where the presence of minor contaminants does not significantly impact the overall process. On the other hand, the >95% purity level is used in more sensitive applications, such as pharmaceutical manufacturing, where even small amounts of impurities can affect the quality and efficacy of the final product. This higher purity level ensures that the enzyme performs its intended function without introducing unwanted variables into the process. The "others" category includes products with varying purity levels that do not fall into the >90% or >95% categories. These products may be used in specialized applications where specific purity requirements are needed, or in research settings where different levels of enzyme purity are required for experimental purposes. The choice of purity level depends on the specific requirements of the application and the desired outcome. For instance, in the production of biopharmaceuticals, higher purity levels are often necessary to meet stringent regulatory standards and ensure patient safety. In contrast, industrial applications may have more flexibility in terms of purity requirements, allowing for the use of enzymes with lower purity levels. The market for recombinant Carboxypeptidase B is thus segmented based on these purity levels, with each segment catering to different needs and applications. Companies operating in this market focus on producing enzymes with varying purity levels to meet the diverse demands of their customers. They invest in advanced purification technologies and quality control measures to ensure that their products meet the required standards. Additionally, the market is influenced by factors such as regulatory requirements, technological advancements, and the availability of raw materials. As the demand for recombinant Carboxypeptidase B continues to grow, companies are likely to focus on improving their production processes and expanding their product portfolios to include enzymes with different purity levels. This will enable them to cater to a wider range of applications and maintain a competitive edge in the market.

Functional Studies, SDS-PAGE, HPLC, Others in the Global Recombinant Carboxypeptidase B Market:

The Global Recombinant Carboxypeptidase B Market finds extensive usage in various areas, including functional studies, SDS-PAGE, HPLC, and others. In functional studies, recombinant Carboxypeptidase B is used to investigate the role and function of specific proteins in biological processes. By selectively removing certain amino acids from proteins, researchers can study the effects of these modifications on protein function, stability, and interactions. This helps in understanding the underlying mechanisms of various diseases and developing targeted therapies. In SDS-PAGE (Sodium Dodecyl Sulfate-Polyacrylamide Gel Electrophoresis), recombinant Carboxypeptidase B is used to analyze protein samples by breaking down proteins into smaller fragments. This technique is widely used in molecular biology and biochemistry to separate and identify proteins based on their size and charge. The enzyme helps in generating specific protein fragments that can be easily analyzed, providing valuable information about the protein's structure and composition. In HPLC (High-Performance Liquid Chromatography), recombinant Carboxypeptidase B is used to purify and analyze proteins and peptides. HPLC is a powerful analytical technique that separates, identifies, and quantifies components in a mixture. The enzyme aids in the digestion of proteins into smaller peptides, which can then be separated and analyzed using HPLC. This is particularly useful in the pharmaceutical industry for quality control and ensuring the purity of biopharmaceutical products. Other applications of recombinant Carboxypeptidase B include its use in the production of recombinant proteins and peptides, where it helps in the removal of specific amino acids to generate the desired protein product. It is also used in the food and beverage industry for protein modification and in the development of diagnostic assays for detecting specific proteins or peptides. The versatility of recombinant Carboxypeptidase B makes it an essential tool in various fields, driving its demand in the global market.

Global Recombinant Carboxypeptidase B Market Outlook:

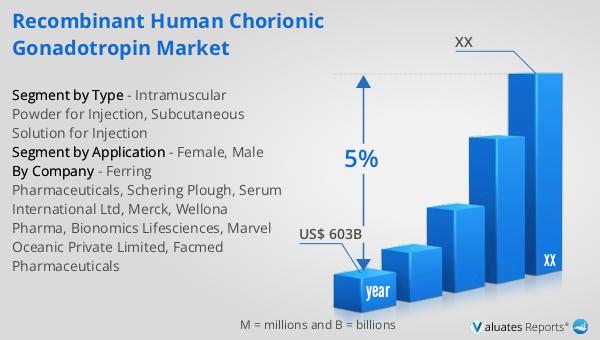

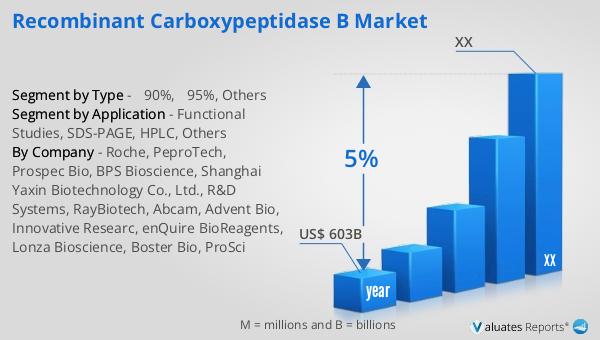

According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% during the next six years. This indicates a robust growth trajectory for the medical device industry, driven by factors such as technological advancements, increasing healthcare expenditure, and the rising prevalence of chronic diseases. The growing aging population and the increasing demand for minimally invasive procedures are also contributing to the market's expansion. Companies operating in this market are focusing on innovation and the development of new products to meet the evolving needs of healthcare providers and patients. Additionally, regulatory changes and the increasing emphasis on patient safety and quality are shaping the market dynamics. The medical device industry is characterized by intense competition, with key players continuously striving to enhance their product offerings and expand their market presence. The market's growth is also supported by the increasing adoption of digital health technologies and the integration of artificial intelligence and machine learning in medical devices. These advancements are expected to improve patient outcomes and streamline healthcare delivery, further driving the market's growth. Overall, the global medical device market is poised for significant growth in the coming years, offering numerous opportunities for companies to innovate and expand their market share.

| Report Metric | Details |

| Report Name | Recombinant Carboxypeptidase B Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Roche, PeproTech, Prospec Bio, BPS Bioscience, Shanghai Yaxin Biotechnology Co., Ltd., R&D Systems, RayBiotech, Abcam, Advent Bio, Innovative Researc, enQuire BioReagents, Lonza Bioscience, Boster Bio, ProSci |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |