What is Global Antiemetic Patch Market?

The Global Antiemetic Patch Market refers to the worldwide market for transdermal patches designed to prevent nausea and vomiting. These patches are particularly useful for patients undergoing chemotherapy, surgery, or those who suffer from motion sickness. The patches work by delivering medication through the skin, providing a steady release of antiemetic drugs into the bloodstream. This method of delivery is advantageous because it bypasses the digestive system, which can be compromised in patients experiencing severe nausea. The market includes various types of antiemetic patches, each formulated with different active ingredients to target specific causes of nausea. The growing prevalence of cancer and the increasing number of surgeries globally are significant factors driving the demand for antiemetic patches. Additionally, the convenience and non-invasive nature of these patches make them a preferred choice for many patients and healthcare providers.

Granisetron, Scopolamine, Others in the Global Antiemetic Patch Market:

Granisetron is one of the key active ingredients used in antiemetic patches within the Global Antiemetic Patch Market. Granisetron is a serotonin 5-HT3 receptor antagonist, which means it works by blocking the action of serotonin, a natural substance that may cause nausea and vomiting. This medication is particularly effective for patients undergoing chemotherapy or radiation therapy, as these treatments often trigger severe nausea. Granisetron patches are designed to provide a controlled release of the drug over several days, ensuring continuous relief from nausea without the need for frequent dosing. This is especially beneficial for patients who may have difficulty swallowing pills or keeping oral medications down due to their condition. Scopolamine is another important active ingredient used in antiemetic patches. It is an anticholinergic drug that works by blocking the action of acetylcholine, a neurotransmitter involved in the vomiting reflex. Scopolamine patches are commonly used to prevent motion sickness and postoperative nausea and vomiting. These patches are typically applied behind the ear, where they can deliver the medication directly into the bloodstream through the skin. The effects of a single scopolamine patch can last up to three days, making it a convenient option for travelers or patients recovering from surgery. Other active ingredients used in antiemetic patches include meclizine, promethazine, and ondansetron. Each of these drugs has a unique mechanism of action and is chosen based on the specific needs of the patient. Meclizine, for example, is an antihistamine that is effective in treating motion sickness and vertigo. Promethazine is another antihistamine that is often used to treat nausea and vomiting associated with surgery, chemotherapy, and other medical conditions. Ondansetron, like granisetron, is a serotonin 5-HT3 receptor antagonist and is commonly used to prevent nausea and vomiting caused by cancer treatments. The availability of different active ingredients allows healthcare providers to tailor antiemetic therapy to the individual needs of each patient, improving the overall effectiveness of treatment.

Hospital, Radiology Center, Others in the Global Antiemetic Patch Market:

The usage of antiemetic patches in hospitals is widespread due to their effectiveness and ease of use. In a hospital setting, patients undergoing chemotherapy, radiation therapy, or surgery are at high risk of experiencing nausea and vomiting. Antiemetic patches provide a reliable and non-invasive method of delivering medication to these patients, ensuring continuous relief from symptoms. The patches are particularly useful for patients who may have difficulty swallowing pills or keeping oral medications down due to their condition. Additionally, the controlled release of medication provided by the patches helps maintain consistent drug levels in the bloodstream, reducing the need for frequent dosing and minimizing the risk of side effects. Radiology centers also make extensive use of antiemetic patches, particularly for patients undergoing radiation therapy. Radiation therapy can cause severe nausea and vomiting, which can significantly impact a patient's quality of life and ability to continue treatment. Antiemetic patches offer a convenient and effective solution for managing these symptoms, allowing patients to complete their treatment with minimal discomfort. The patches are easy to apply and can be worn discreetly, making them a preferred choice for many patients. In addition to hospitals and radiology centers, antiemetic patches are also used in other healthcare settings, such as outpatient clinics and home care. For patients receiving treatment at home, antiemetic patches provide a convenient and effective way to manage nausea and vomiting without the need for frequent visits to a healthcare facility. This is particularly beneficial for patients with chronic conditions, such as cancer, who may require long-term antiemetic therapy. The patches are easy to use and can be applied by the patient or a caregiver, ensuring continuous relief from symptoms and improving the overall quality of life. The versatility and effectiveness of antiemetic patches make them a valuable tool in the management of nausea and vomiting across a wide range of healthcare settings.

Global Antiemetic Patch Market Outlook:

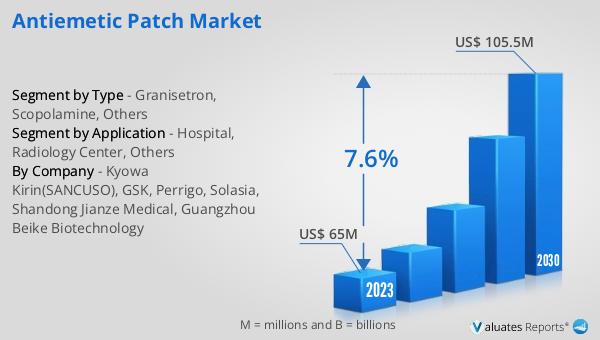

The global Antiemetic Patch market was valued at US$ 65 million in 2023 and is anticipated to reach US$ 105.5 million by 2030, witnessing a CAGR of 7.6% during the forecast period 2024-2030. The global pharmaceutical market was valued at 1475 billion USD in 2022, growing at a CAGR of 5% over the next six years. In comparison, the chemical drug market was estimated to increase from 1005 billion USD in 2018 to 1094 billion USD in 2022. This growth in the pharmaceutical and chemical drug markets highlights the increasing demand for effective and convenient treatment options, such as antiemetic patches. The steady growth of the antiemetic patch market reflects the rising prevalence of conditions that cause nausea and vomiting, as well as the growing recognition of the benefits of transdermal drug delivery systems. The convenience, effectiveness, and non-invasive nature of antiemetic patches make them an attractive option for both patients and healthcare providers, driving their adoption across various healthcare settings.

| Report Metric | Details |

| Report Name | Antiemetic Patch Market |

| Accounted market size in 2023 | US$ 65 million |

| Forecasted market size in 2030 | US$ 105.5 million |

| CAGR | 7.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Kyowa Kirin(SANCUSO), GSK, Perrigo, Solasia, Shandong Jianze Medical, Guangzhou Beike Biotechnology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |