What is Global Medical Pressure Sensitive Adhesive Tape Market?

The Global Medical Pressure Sensitive Adhesive Tape Market refers to the worldwide industry focused on the production and distribution of adhesive tapes specifically designed for medical applications. These tapes are crucial in healthcare settings for tasks such as securing dressings, bandages, and medical devices to the skin. They are engineered to adhere firmly yet gently, minimizing skin irritation and ensuring patient comfort. The market encompasses a variety of tape types, including single-sided and double-sided tapes, each serving different medical needs. Factors driving the market include the increasing prevalence of chronic diseases, the aging population, and the rising demand for advanced wound care products. Additionally, technological advancements in adhesive materials and the growing emphasis on infection control in healthcare facilities contribute to the market's expansion. The market is highly competitive, with numerous manufacturers striving to innovate and improve the performance and safety of their products.

Single Sided, Double Sided in the Global Medical Pressure Sensitive Adhesive Tape Market:

Single-sided and double-sided tapes are two primary categories within the Global Medical Pressure Sensitive Adhesive Tape Market, each serving distinct purposes in medical applications. Single-sided tapes have adhesive on one side only, making them ideal for securing dressings, bandages, and medical devices directly to the skin. These tapes are designed to provide a strong yet gentle hold, ensuring that they stay in place without causing discomfort or skin damage. They are commonly used in wound care, surgical procedures, and everyday medical applications where a reliable adhesive is needed. On the other hand, double-sided tapes have adhesive on both sides, allowing them to bond two surfaces together. In medical settings, double-sided tapes are often used for attaching medical devices, such as sensors or electrodes, to the skin or other surfaces. They provide a secure and stable connection, which is crucial for the accurate functioning of these devices. Both single-sided and double-sided tapes are made from various materials, including paper, fabric, and plastic, each offering different levels of breathability, flexibility, and strength. The choice of material depends on the specific medical application and the requirements for patient comfort and safety. For instance, fabric tapes are often preferred for their flexibility and breathability, making them suitable for long-term use on the skin. Plastic tapes, on the other hand, offer higher strength and are often used in situations where a more robust adhesive is needed. The development of advanced adhesive technologies has also led to the creation of hypoallergenic tapes, which are designed to minimize the risk of allergic reactions and skin irritation. These tapes are particularly important for patients with sensitive skin or those who require frequent tape changes. In addition to their adhesive properties, medical tapes must also meet stringent regulatory standards to ensure their safety and effectiveness. Manufacturers must conduct rigorous testing to demonstrate that their products are biocompatible, non-toxic, and capable of maintaining their adhesive properties under various conditions. This includes testing for factors such as adhesion strength, moisture resistance, and the ability to withstand sterilization processes. The global market for medical pressure-sensitive adhesive tapes is characterized by continuous innovation, with manufacturers constantly seeking to improve the performance and safety of their products. This includes the development of new adhesive formulations, the use of advanced materials, and the incorporation of antimicrobial properties to reduce the risk of infection. As a result, healthcare providers have access to a wide range of high-quality adhesive tapes that can meet the diverse needs of patients and medical professionals.

Hospitals, Clinics, Home Care in the Global Medical Pressure Sensitive Adhesive Tape Market:

The usage of Global Medical Pressure Sensitive Adhesive Tape Market products spans across various healthcare settings, including hospitals, clinics, and home care environments. In hospitals, these tapes are indispensable for a multitude of applications. They are used to secure dressings and bandages over surgical incisions and wounds, ensuring that they stay in place and protect the area from contamination. Medical tapes are also used to attach medical devices such as catheters, IV lines, and monitoring equipment to the patient's body, providing a secure and stable connection that is crucial for accurate monitoring and treatment. The ability of these tapes to adhere firmly yet gently is particularly important in hospital settings, where patients may have sensitive or compromised skin due to their medical conditions. In clinics, medical pressure-sensitive adhesive tapes are used for similar purposes, albeit on a smaller scale. Clinics often handle minor surgical procedures, wound care, and routine medical examinations, all of which require the use of reliable adhesive tapes. These tapes help secure dressings and medical devices, ensuring that they remain in place during the patient's visit and any subsequent follow-up appointments. The convenience and effectiveness of these tapes make them a staple in clinical settings, where quick and efficient patient care is paramount. Home care is another significant area where medical pressure-sensitive adhesive tapes play a crucial role. As more patients receive medical treatment and care at home, the demand for easy-to-use and effective adhesive tapes has increased. These tapes are used to secure dressings, bandages, and medical devices for patients who are managing chronic conditions, recovering from surgery, or receiving palliative care. The ability to apply and remove these tapes without causing discomfort or skin damage is particularly important in home care settings, where caregivers may not have the same level of training as medical professionals. Additionally, the availability of hypoallergenic and gentle adhesive tapes ensures that patients with sensitive skin can receive the care they need without experiencing adverse reactions. The versatility and reliability of medical pressure-sensitive adhesive tapes make them an essential component of patient care across hospitals, clinics, and home care environments. Their ability to provide secure adhesion while minimizing skin irritation and discomfort ensures that patients receive the best possible care, regardless of the setting.

Global Medical Pressure Sensitive Adhesive Tape Market Outlook:

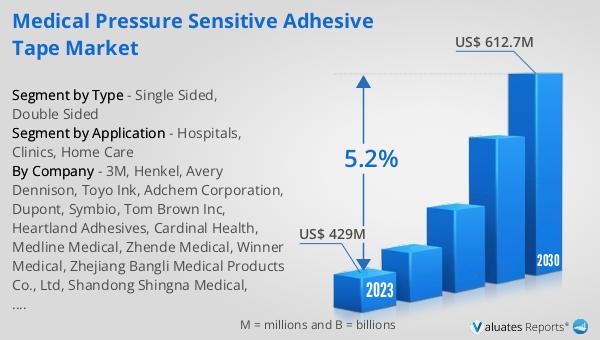

The global Medical Pressure Sensitive Adhesive Tape market was valued at US$ 429 million in 2023 and is anticipated to reach US$ 612.7 million by 2030, witnessing a CAGR of 5.2% during the forecast period from 2024 to 2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% over the next six years. This growth is driven by the increasing demand for advanced medical products and technologies, as well as the rising prevalence of chronic diseases and the aging population. The market for medical pressure-sensitive adhesive tapes is expected to benefit from these trends, as they are essential components in a wide range of medical applications. The continuous innovation and development of new adhesive materials and technologies will further support the market's growth, ensuring that healthcare providers have access to high-quality and reliable adhesive tapes for patient care.

| Report Metric | Details |

| Report Name | Medical Pressure Sensitive Adhesive Tape Market |

| Accounted market size in 2023 | US$ 429 million |

| Forecasted market size in 2030 | US$ 612.7 million |

| CAGR | 5.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | 3M, Henkel, Avery Dennison, Toyo Ink, Adchem Corporation, Dupont, Symbio, Tom Brown Inc, Heartland Adhesives, Cardinal Health, Medline Medical, Zhende Medical, Winner Medical, Zhejiang Bangli Medical Products Co., Ltd, Shandong Shingna Medical, Zhejiang Dingtai Pharmaceutical Co., Ltd., Haishi Hainuo Group, Jianerkang Medical Co.,Ltd., Wuhan Huawei Technology Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |