What is Global Resin Based Composites for Dental Market?

Global Resin Based Composites for Dental Market refers to the worldwide industry focused on the production and distribution of resin-based composite materials used in dental procedures. These composites are primarily utilized for restorative purposes, such as filling cavities, repairing chipped teeth, and improving the overall aesthetics of a patient's smile. The market encompasses a variety of products, including different types of composites like microfilled, macrofilled, hybrids (universal), and nanocomposites, each designed to meet specific dental needs. The demand for these materials is driven by the increasing prevalence of dental issues, advancements in dental technology, and a growing awareness of oral health. Dental professionals prefer resin-based composites due to their durability, aesthetic appeal, and ease of application. The market is also influenced by regulatory standards and innovations aimed at enhancing the performance and safety of these materials. As dental care continues to evolve, the Global Resin Based Composites for Dental Market is expected to expand, offering new opportunities for manufacturers and healthcare providers alike.

Microfilled Composites, Macrofilled Composites, Hybrids (Universal) Composites, Nanocomposites in the Global Resin Based Composites for Dental Market:

Microfilled composites, macrofilled composites, hybrids (universal) composites, and nanocomposites are various types of resin-based composites used in dental applications, each with unique properties and benefits. Microfilled composites contain very small filler particles, typically around 0.04 micrometers in size, which provide a smooth and highly polishable surface. These composites are ideal for anterior restorations where aesthetics are paramount, as they can mimic the natural translucency and gloss of tooth enamel. However, their smaller filler size can result in lower strength compared to other types of composites, making them less suitable for load-bearing areas. Macrofilled composites, on the other hand, have larger filler particles, usually ranging from 1 to 3 micrometers. These composites offer greater strength and durability, making them suitable for posterior restorations where the material must withstand significant chewing forces. However, the larger filler particles can make the surface rougher and more prone to wear over time. Hybrids, or universal composites, combine both small and large filler particles to offer a balance between strength and aesthetics. These composites are versatile and can be used for both anterior and posterior restorations. They provide good polishability and wear resistance, making them a popular choice among dental professionals. Nanocomposites represent the latest advancement in composite technology, featuring filler particles that are less than 100 nanometers in size. These composites offer exceptional polishability, strength, and wear resistance, making them suitable for a wide range of dental applications. The small particle size allows for a smooth surface finish that closely resembles natural tooth enamel, while the high filler content provides the necessary strength for both anterior and posterior restorations. Each type of composite has its own set of advantages and limitations, and the choice of material often depends on the specific clinical situation and the desired outcome.

Hospitals, Dental Clinics, Others in the Global Resin Based Composites for Dental Market:

Global Resin Based Composites for Dental Market finds extensive usage in various healthcare settings, including hospitals, dental clinics, and other specialized facilities. In hospitals, these composites are often used in emergency dental procedures and complex restorative treatments. Hospitals typically handle a wide range of dental cases, from trauma-related injuries to intricate surgical interventions, and the versatility of resin-based composites makes them an invaluable resource. The ability to quickly and effectively restore damaged teeth using these materials can significantly improve patient outcomes and reduce recovery times. Dental clinics, on the other hand, are the primary users of resin-based composites, given their focus on routine dental care and cosmetic procedures. Dentists in these settings frequently use composites for filling cavities, repairing chipped or broken teeth, and performing aesthetic enhancements such as veneers and bonding. The ease of application, combined with the ability to match the natural color of teeth, makes resin-based composites a preferred choice for many dental practitioners. Additionally, the advancements in composite technology have led to the development of materials that offer improved durability and resistance to wear, further enhancing their appeal in clinical practice. Other specialized facilities, such as orthodontic and pediatric dental offices, also utilize resin-based composites for various applications. In orthodontics, composites are used to bond brackets and other appliances to teeth, ensuring a secure and stable fit. Pediatric dentists often rely on these materials for their minimally invasive properties and the ability to provide aesthetically pleasing results for young patients. The use of resin-based composites in these settings underscores their versatility and effectiveness in addressing a wide range of dental needs. Overall, the widespread adoption of resin-based composites across different healthcare environments highlights their importance in modern dentistry and their role in improving patient care and satisfaction.

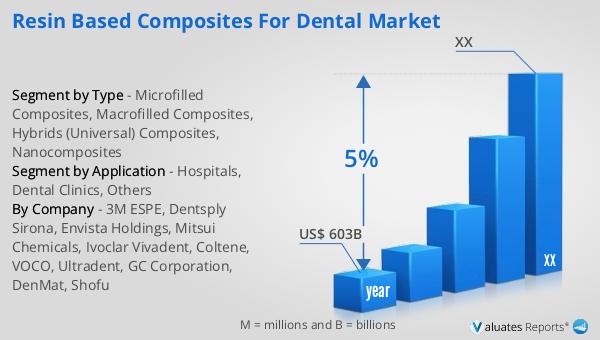

Global Resin Based Composites for Dental Market Outlook:

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This substantial market size reflects the increasing demand for advanced medical technologies and innovations aimed at improving patient care and outcomes. The steady growth rate indicates a robust and expanding industry, driven by factors such as an aging population, rising prevalence of chronic diseases, and ongoing advancements in medical research and development. As healthcare systems worldwide continue to evolve and adapt to new challenges, the demand for cutting-edge medical devices is expected to remain strong. This growth trajectory also underscores the importance of continuous investment in research and development to drive innovation and meet the evolving needs of patients and healthcare providers. The global medical device market's expansion presents significant opportunities for manufacturers, investors, and stakeholders to contribute to the advancement of healthcare and improve the quality of life for patients around the world.

| Report Metric | Details |

| Report Name | Resin Based Composites for Dental Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | 3M ESPE, Dentsply Sirona, Envista Holdings, Mitsui Chemicals, Ivoclar Vivadent, Coltene, VOCO, Ultradent, GC Corporation, DenMat, Shofu |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |