What is Global Obese Patient Medical Chair Market?

The Global Obese Patient Medical Chair Market is a specialized segment within the broader medical furniture industry, focusing on chairs designed to accommodate obese patients. These chairs are engineered to provide comfort, support, and safety for individuals with higher body weights, often featuring reinforced frames, wider seats, and enhanced cushioning. The market for these chairs is driven by the increasing prevalence of obesity worldwide, which has led to a growing demand for medical equipment that can cater to the needs of larger patients. These chairs are used in various healthcare settings, including hospitals, clinics, and home care environments, to ensure that obese patients receive the necessary medical attention without compromising their comfort or safety. The market is characterized by a range of products, from basic manual adjustment chairs to advanced models with automatic adjustment features, catering to different needs and budgets. As healthcare providers continue to recognize the importance of specialized equipment for obese patients, the demand for these medical chairs is expected to grow, making it a significant area of focus within the medical furniture industry.

Manual Adjustment, Automatic Adjustment in the Global Obese Patient Medical Chair Market:

Manual adjustment and automatic adjustment are two key features in the Global Obese Patient Medical Chair Market, each offering distinct benefits and catering to different user needs. Manual adjustment chairs are typically more affordable and straightforward, relying on mechanical levers or knobs that allow caregivers or patients to adjust the chair's position. These chairs are designed to be durable and easy to use, making them a popular choice in settings where budget constraints are a concern. They offer basic functionalities such as reclining backrests, adjustable footrests, and height adjustments, which can be manually controlled to provide the necessary comfort and support for obese patients. On the other hand, automatic adjustment chairs are equipped with motorized mechanisms that enable effortless adjustments at the push of a button. These chairs often come with advanced features such as programmable positions, memory settings, and remote controls, providing a higher level of convenience and customization. Automatic adjustment chairs are particularly beneficial in settings where frequent adjustments are needed, such as in hospitals or long-term care facilities, as they reduce the physical strain on caregivers and enhance patient comfort. Additionally, these chairs may include safety features like weight sensors and emergency stop functions to ensure the well-being of the patient. While automatic adjustment chairs tend to be more expensive, their advanced functionalities and ease of use make them a valuable investment for healthcare providers aiming to improve patient care and operational efficiency. Both manual and automatic adjustment chairs play a crucial role in the Global Obese Patient Medical Chair Market, addressing the diverse needs of obese patients and the healthcare professionals who care for them. As the market continues to evolve, innovations in both manual and automatic adjustment technologies are expected to enhance the functionality and accessibility of these medical chairs, further improving the quality of care for obese patients.

Hospital, Clinic, Household, Others in the Global Obese Patient Medical Chair Market:

The usage of Global Obese Patient Medical Chairs spans across various settings, including hospitals, clinics, households, and other healthcare environments. In hospitals, these chairs are essential for providing comfortable seating and support for obese patients during medical examinations, treatments, and recovery periods. They are often used in emergency rooms, surgical wards, and outpatient departments, where the need for durable and adjustable seating solutions is critical. The chairs help in minimizing the risk of pressure sores and other complications associated with prolonged sitting, ensuring that patients receive the best possible care. In clinics, obese patient medical chairs are used in consultation rooms, diagnostic centers, and therapy sessions, where they provide a stable and comfortable seating option for patients undergoing various medical procedures. These chairs are designed to accommodate the specific needs of obese patients, offering features such as reinforced frames and wider seats to ensure their safety and comfort. In household settings, these chairs are used by individuals who require specialized seating solutions due to their weight and medical conditions. They provide a comfortable and supportive seating option for daily activities, helping to improve the quality of life for obese individuals. Additionally, these chairs are used in other healthcare environments such as nursing homes, rehabilitation centers, and bariatric clinics, where they play a crucial role in providing specialized care for obese patients. The versatility and functionality of these chairs make them an indispensable part of the healthcare infrastructure, ensuring that obese patients receive the necessary support and comfort in various settings.

Global Obese Patient Medical Chair Market Outlook:

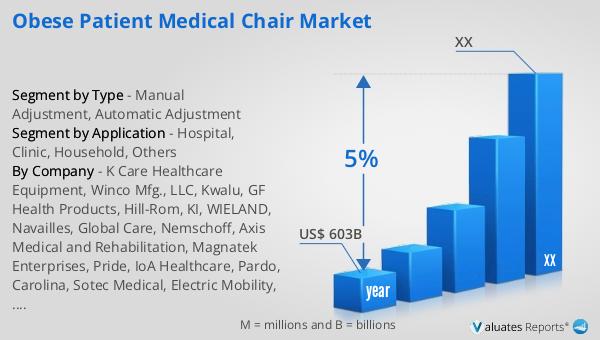

Based on our research, the global market for medical devices is projected to reach approximately $603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This significant market size underscores the increasing demand for medical devices across various healthcare sectors, driven by advancements in medical technology, an aging population, and the rising prevalence of chronic diseases. The steady growth rate reflects the ongoing investments in healthcare infrastructure, research and development, and the adoption of innovative medical solutions. As healthcare providers and patients continue to seek more efficient and effective medical devices, the market is expected to expand, offering numerous opportunities for manufacturers and stakeholders in the industry. The robust growth trajectory of the medical device market highlights the critical role these devices play in improving patient outcomes, enhancing the quality of care, and addressing the evolving needs of the global healthcare system. This growth is also indicative of the increasing focus on personalized medicine, minimally invasive procedures, and the integration of digital technologies in healthcare, which are driving the demand for advanced medical devices. Overall, the projected market size and growth rate reflect the dynamic nature of the medical device industry and its pivotal role in shaping the future of healthcare.

| Report Metric | Details |

| Report Name | Obese Patient Medical Chair Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | K Care Healthcare Equipment, Winco Mfg., LLC, Kwalu, GF Health Products, Hill-Rom, KI, WIELAND, Navailles, Global Care, Nemschoff, Axis Medical and Rehabilitation, Magnatek Enterprises, Pride, IoA Healthcare, Pardo, Carolina, Sotec Medical, Electric Mobility, Teal, Gardhen Bilance, Stance Healthcare, Excel Medical, Krug, Benmor Medical, Trinity Furniture |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |