What is Global Electric Ion Therapy Machines Market?

The Global Electric Ion Therapy Machines Market is a rapidly evolving sector within the broader medical device industry. These machines utilize electric ions to treat various medical conditions, offering a non-invasive and effective alternative to traditional therapies. The technology behind electric ion therapy involves the use of charged particles to stimulate cellular activity, promote healing, and reduce pain. This market is gaining traction due to the increasing prevalence of chronic diseases, advancements in medical technology, and a growing preference for non-invasive treatment options. The machines are used in various medical fields, including dermatology, surgery, dentistry, ENT (ear, nose, and throat), and gynecology. As healthcare providers and patients alike seek more efficient and less painful treatment methods, the demand for electric ion therapy machines is expected to rise. The market is characterized by continuous innovation, with manufacturers focusing on improving the efficacy, safety, and user-friendliness of these devices.

With Power, Without Power in the Global Electric Ion Therapy Machines Market:

Electric ion therapy machines can be broadly categorized into two types: with power and without power. Machines with power are typically more advanced and offer a range of features that enhance their therapeutic capabilities. These devices are powered by electricity and often come with adjustable settings, allowing healthcare providers to tailor treatments to individual patient needs. They are commonly used in clinical settings where precise control over treatment parameters is crucial. For instance, in dermatology, powered electric ion therapy machines can be used to treat conditions like acne, eczema, and psoriasis by delivering targeted ion therapy to affected areas. In surgery, these machines help in wound healing and reducing post-operative pain by stimulating tissue regeneration and reducing inflammation. In dentistry, powered machines are used for procedures like root canal treatments and gum disease management, providing pain relief and promoting faster healing. In ENT, they assist in treating conditions such as sinusitis and tonsillitis by reducing inflammation and promoting tissue repair. In gynecology, powered electric ion therapy machines are used for treating conditions like endometriosis and pelvic inflammatory disease, offering pain relief and promoting healing. On the other hand, electric ion therapy machines without power are simpler devices that rely on manual operation or passive ion generation. These machines are often more affordable and easier to use, making them suitable for home use or in settings where advanced features are not necessary. In dermatology, non-powered machines can be used for basic skin treatments, such as improving skin texture and reducing minor blemishes. In surgery, they can be used for post-operative care, helping to reduce swelling and promote healing through passive ion therapy. In dentistry, non-powered machines are useful for maintaining oral hygiene and managing minor dental issues. In ENT, they can be used for basic treatments like reducing nasal congestion and soothing sore throats. In gynecology, non-powered electric ion therapy machines can be used for general wellness and managing minor gynecological issues. While these machines may not offer the same level of precision and control as their powered counterparts, they still provide significant therapeutic benefits and are a valuable addition to the global electric ion therapy machines market.

Dermatology, Surgery, Dentistry, ENT, Department of Gynaecology in the Global Electric Ion Therapy Machines Market:

The usage of Global Electric Ion Therapy Machines Market spans across various medical fields, including dermatology, surgery, dentistry, ENT, and gynecology. In dermatology, these machines are used to treat a range of skin conditions such as acne, eczema, and psoriasis. The electric ions help to reduce inflammation, promote healing, and improve skin texture. Patients benefit from non-invasive treatments that offer effective results with minimal side effects. In surgery, electric ion therapy machines are used to enhance wound healing and reduce post-operative pain. The ions stimulate tissue regeneration and reduce inflammation, leading to faster recovery times and improved patient outcomes. Surgeons can use these machines during and after surgical procedures to ensure optimal healing and pain management. In dentistry, electric ion therapy machines are used for various procedures, including root canal treatments, gum disease management, and oral hygiene maintenance. The ions help to reduce pain, promote healing, and improve overall oral health. Dentists can use these machines to provide more comfortable and effective treatments for their patients. In the field of ENT, electric ion therapy machines are used to treat conditions such as sinusitis, tonsillitis, and nasal congestion. The ions help to reduce inflammation, promote tissue repair, and alleviate symptoms, providing patients with relief from their ENT issues. These machines offer a non-invasive and effective treatment option for patients suffering from chronic ENT conditions. In the department of gynecology, electric ion therapy machines are used to treat conditions such as endometriosis, pelvic inflammatory disease, and general gynecological wellness. The ions help to reduce pain, promote healing, and improve overall reproductive health. Gynecologists can use these machines to provide effective and non-invasive treatments for their patients, improving their quality of life. Overall, the usage of electric ion therapy machines in these medical fields highlights their versatility and effectiveness in treating a wide range of conditions. As the demand for non-invasive and effective treatment options continues to grow, the global electric ion therapy machines market is expected to expand, offering new opportunities for healthcare providers and patients alike.

Global Electric Ion Therapy Machines Market Outlook:

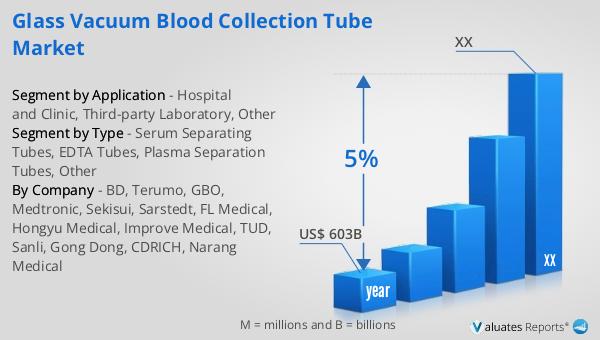

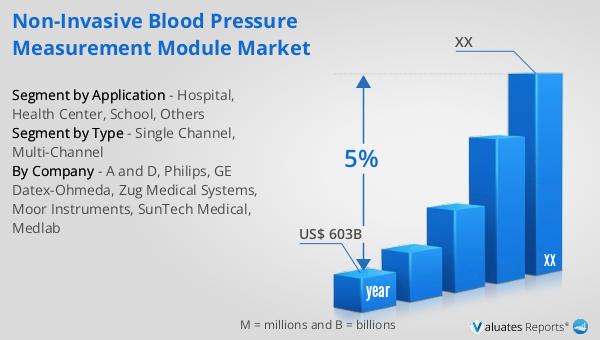

The global pharmaceutical market was valued at approximately 1,475 billion USD in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 5% over the next six years. In comparison, the chemical drug market has shown significant growth as well. It was estimated to increase from 1,005 billion USD in 2018 to 1,094 billion USD in 2022. This growth in both markets underscores the increasing demand for pharmaceutical and chemical drug products worldwide. The pharmaceutical market encompasses a wide range of products, including prescription medications, over-the-counter drugs, and biologics, all of which contribute to its substantial market size. The chemical drug market, on the other hand, focuses on synthetic compounds used in the treatment of various medical conditions. The steady growth in these markets can be attributed to factors such as advancements in medical research, an aging global population, and the rising prevalence of chronic diseases. As healthcare needs continue to evolve, both the pharmaceutical and chemical drug markets are expected to play a crucial role in meeting the growing demand for effective and innovative treatments.

| Report Metric | Details |

| Report Name | Electric Ion Therapy Machines Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Intuitive Surgical, Hubei YJT Technology, Shenzhen Sunray Technology, ICEN Technology Company Limited, Health&Health (Group), WBL Medical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |