What is Global Medical Head Simulator Market?

The Global Medical Head Simulator Market is a specialized segment within the broader medical simulation market, focusing on the development and utilization of head simulators for medical training and research. These simulators are designed to replicate the anatomical and physiological features of the human head, providing a realistic platform for healthcare professionals to practice and refine their skills. The market encompasses a wide range of products, including adult and child head simulators, each tailored to meet specific training needs. These simulators are used in various settings, such as hospitals, medical colleges, and training institutions, to enhance the proficiency of medical practitioners in procedures like intubation, cranial surgery, and dental practices. The growing emphasis on patient safety and the increasing complexity of medical procedures are driving the demand for advanced simulation tools, making the Global Medical Head Simulator Market a vital component of modern medical education and training. The market is characterized by continuous innovation, with manufacturers striving to develop more sophisticated and realistic simulators to meet the evolving needs of the healthcare industry.

Adult Type, Child Type in the Global Medical Head Simulator Market:

In the Global Medical Head Simulator Market, products are broadly categorized into adult type and child type simulators, each serving distinct purposes in medical training and education. Adult type head simulators are designed to mimic the anatomical features and physiological responses of an adult human head. These simulators are extensively used in training scenarios that involve complex procedures such as neurosurgery, cranial trauma management, and advanced airway management techniques. They provide a realistic platform for medical professionals to practice and perfect their skills, thereby reducing the risk of errors in real-life situations. The adult type simulators are equipped with features like realistic skin texture, anatomical landmarks, and functional airways, which allow for a comprehensive training experience. On the other hand, child type head simulators are specifically designed to replicate the unique anatomical and physiological characteristics of a child's head. These simulators are crucial for training healthcare providers in pediatric care, where the anatomical differences between children and adults can significantly impact the approach and techniques used. Child type simulators are used in scenarios such as pediatric intubation, cranial surgery, and trauma management, providing a safe and controlled environment for practitioners to develop their skills. The use of child type simulators is particularly important in pediatric emergency care, where timely and accurate interventions can be life-saving. Both adult and child type head simulators are integral to the Global Medical Head Simulator Market, addressing the diverse training needs of healthcare professionals across different specialties. The continuous advancements in simulation technology are enhancing the realism and functionality of these simulators, making them indispensable tools in medical education and training.

Hospital, College, Training Institutions, Others in the Global Medical Head Simulator Market:

The Global Medical Head Simulator Market finds extensive usage across various settings, including hospitals, colleges, training institutions, and other specialized facilities. In hospitals, medical head simulators are used for training resident doctors, nurses, and other healthcare staff in critical procedures such as intubation, cranial surgeries, and emergency trauma care. These simulators provide a risk-free environment for practitioners to hone their skills, thereby improving patient safety and outcomes. Hospitals also use these simulators for ongoing professional development and competency assessments, ensuring that their staff remains proficient in the latest medical techniques. In medical colleges, head simulators are an essential part of the curriculum, providing students with hands-on experience in a controlled setting. They are used in anatomy classes, surgical training, and emergency response drills, helping students to bridge the gap between theoretical knowledge and practical application. Training institutions, which specialize in medical education and certification, rely heavily on head simulators to provide realistic training scenarios for their participants. These institutions offer specialized courses in areas such as advanced airway management, cranial surgery, and pediatric care, using simulators to ensure that their trainees are well-prepared for real-world challenges. Other specialized facilities, such as research centers and simulation labs, also utilize medical head simulators for various purposes, including the development of new medical techniques, testing of medical devices, and conducting clinical research. The versatility and realism of these simulators make them invaluable tools in the continuous improvement of medical education and practice.

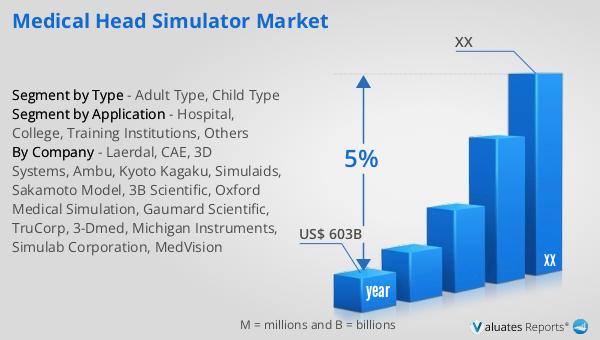

Global Medical Head Simulator Market Outlook:

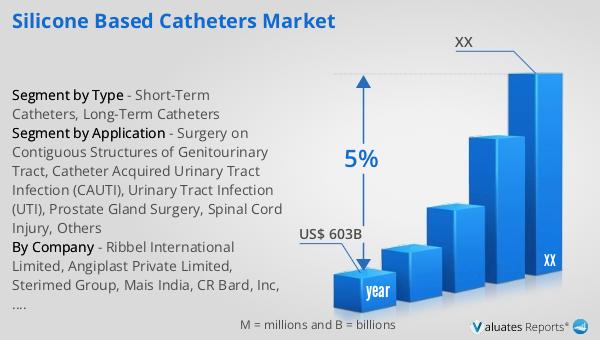

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% CAGR over the next six years. This significant market size underscores the critical role that medical devices play in the healthcare industry, driving advancements in patient care, diagnostics, and treatment. The steady growth rate reflects the increasing demand for innovative medical technologies and the continuous efforts to improve healthcare outcomes worldwide. As the healthcare landscape evolves, the need for advanced medical devices, including simulation tools like medical head simulators, becomes more pronounced. These devices not only enhance the training and proficiency of healthcare professionals but also contribute to better patient safety and care standards. The projected growth of the medical device market highlights the ongoing investment in research and development, aimed at creating more effective and efficient healthcare solutions. This trend is expected to drive further advancements in medical simulation technology, making it an integral part of modern medical education and practice.

| Report Metric | Details |

| Report Name | Medical Head Simulator Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Laerdal, CAE, 3D Systems, Ambu, Kyoto Kagaku, Simulaids, Sakamoto Model, 3B Scientific, Oxford Medical Simulation, Gaumard Scientific, TruCorp, 3-Dmed, Michigan Instruments, Simulab Corporation, MedVision |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |