What is Global Food Grade Sodium Propionate Market?

The Global Food Grade Sodium Propionate Market refers to the worldwide industry involved in the production, distribution, and consumption of sodium propionate that meets food-grade standards. Sodium propionate is a salt derived from propionic acid and is widely used as a preservative in various food products. It helps to inhibit the growth of mold and bacteria, thereby extending the shelf life of food items. This market encompasses various regions, including the Americas, Europe, Asia-Pacific, and other parts of the world. The demand for food-grade sodium propionate is driven by its extensive application in the food industry, particularly in bakery products, dairy items, and processed foods. The market is influenced by factors such as increasing consumer awareness about food safety, the rising demand for convenience foods, and stringent food safety regulations. Companies operating in this market focus on product innovation, quality enhancement, and expanding their distribution networks to cater to the growing demand. The market is characterized by the presence of both large multinational corporations and smaller regional players, each contributing to the overall growth and development of the industry.

Granular, Powder in the Global Food Grade Sodium Propionate Market:

In the Global Food Grade Sodium Propionate Market, sodium propionate is available in two primary forms: granular and powder. Granular sodium propionate is characterized by its coarse texture, which makes it suitable for applications where a slower dissolution rate is desired. This form is often preferred in bakery products, where it can be evenly distributed throughout the dough or batter, ensuring consistent preservation and extending the shelf life of the final product. The granular form is also easier to handle and measure, making it a convenient choice for large-scale food production facilities. On the other hand, powder sodium propionate is finely ground, offering a quicker dissolution rate. This form is ideal for applications where rapid integration into the food matrix is required, such as in dairy products and certain processed foods. The fine texture of the powder allows for a more uniform distribution, enhancing its effectiveness as a preservative. Both forms of sodium propionate are valued for their ability to inhibit the growth of mold and bacteria, thereby ensuring the safety and longevity of food products. The choice between granular and powder forms depends on the specific requirements of the food product and the manufacturing process. In the bakery industry, for instance, granular sodium propionate is often used in bread, cakes, and pastries to prevent spoilage and maintain freshness. The granular form's slower dissolution rate ensures that the preservative effect lasts throughout the product's shelf life. In contrast, the powder form is preferred in dairy products like cheese and yogurt, where a quick and even distribution is crucial for preventing microbial growth. The powder form's fine texture allows it to blend seamlessly with other ingredients, ensuring consistent preservation. Additionally, the powder form is often used in processed foods such as sauces, dressings, and ready-to-eat meals, where rapid integration and uniform distribution are essential. The versatility of sodium propionate in both granular and powder forms makes it a valuable ingredient in the food industry, catering to a wide range of applications and ensuring food safety and quality.

Bakery, Candy, Dairy, Others in the Global Food Grade Sodium Propionate Market:

The usage of Global Food Grade Sodium Propionate Market spans several key areas, including bakery, candy, dairy, and other food products. In the bakery sector, sodium propionate is extensively used to prevent mold growth and extend the shelf life of products such as bread, cakes, and pastries. Its effectiveness as a preservative ensures that bakery items remain fresh and safe for consumption over an extended period. The granular form of sodium propionate is particularly favored in this sector due to its ease of handling and consistent distribution throughout the dough or batter. In the candy industry, sodium propionate is used to inhibit microbial growth in products that are prone to spoilage due to their high sugar content. Candies, especially those with moist textures, can benefit from the preservative properties of sodium propionate, ensuring they remain safe and enjoyable for consumers. The powder form of sodium propionate is often preferred in this sector for its quick dissolution and uniform distribution, which are essential for maintaining the quality of the final product. In the dairy industry, sodium propionate plays a crucial role in preserving products such as cheese, yogurt, and other fermented dairy items. The powder form is particularly effective in this sector, as it blends seamlessly with other ingredients, ensuring even distribution and consistent preservation. By inhibiting the growth of mold and bacteria, sodium propionate helps to extend the shelf life of dairy products, maintaining their quality and safety for consumers. Beyond bakery, candy, and dairy, sodium propionate is also used in a variety of other food products, including processed foods, sauces, dressings, and ready-to-eat meals. Its versatility as a preservative makes it a valuable ingredient in ensuring the safety and longevity of a wide range of food items. The choice between granular and powder forms depends on the specific requirements of the product and the manufacturing process, with both forms offering unique advantages in different applications. Overall, the usage of sodium propionate in these key areas highlights its importance in the food industry, contributing to food safety, quality, and shelf life extension.

Global Food Grade Sodium Propionate Market Outlook:

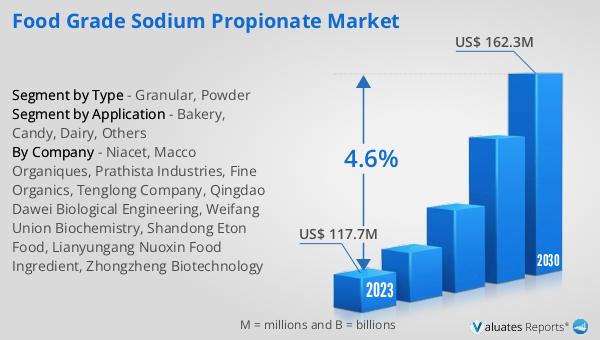

The global Food Grade Sodium Propionate market was valued at US$ 117.7 million in 2023 and is anticipated to reach US$ 162.3 million by 2030, witnessing a CAGR of 4.6% during the forecast period from 2024 to 2030. The Americas hold the largest share of the sodium propionate market, accounting for approximately 39% of the total market share. China follows, with about 24% of the market share. The top three companies in the market collectively occupy around 57% of the market share. This market outlook indicates a steady growth trajectory for the food-grade sodium propionate market, driven by increasing demand for food preservatives and the expanding food industry. The significant market share held by the Americas and China highlights the importance of these regions in the global market landscape. The dominance of the top three companies underscores the competitive nature of the market, with major players focusing on innovation, quality enhancement, and expanding their distribution networks to maintain their market positions. As the market continues to grow, companies will likely invest in research and development to introduce new and improved products, catering to the evolving needs of the food industry. The projected growth in the market value and the steady CAGR reflect the increasing importance of food-grade sodium propionate in ensuring food safety and extending the shelf life of various food products.

| Report Metric | Details |

| Report Name | Food Grade Sodium Propionate Market |

| Accounted market size in 2023 | US$ 117.7 million |

| Forecasted market size in 2030 | US$ 162.3 million |

| CAGR | 4.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Niacet, Macco Organiques, Prathista Industries, Fine Organics, Tenglong Company, Qingdao Dawei Biological Engineering, Weifang Union Biochemistry, Shandong Eton Food, Lianyungang Nuoxin Food Ingredient, Zhongzheng Biotechnology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |