What is Global DRIE Deep Silicon Etching Equipment Market?

The Global DRIE Deep Silicon Etching Equipment Market refers to the industry focused on the production and distribution of equipment used for deep reactive ion etching (DRIE) of silicon. DRIE is a highly specialized process used to create deep, precise, and high-aspect-ratio structures in silicon wafers. This technology is crucial for manufacturing various microelectromechanical systems (MEMS), integrated circuits (ICs), and other advanced semiconductor devices. The market encompasses a range of equipment types, including single-chip and multi-chip systems, each designed to meet specific etching requirements. The demand for DRIE equipment is driven by the growing need for miniaturized electronic components, advancements in semiconductor technology, and the increasing adoption of MEMS in various applications. As industries continue to innovate and develop more complex devices, the importance of DRIE technology and its associated equipment is expected to grow, making it a vital segment within the broader semiconductor manufacturing market.

Single-chip, Multi-chip in the Global DRIE Deep Silicon Etching Equipment Market:

The Global DRIE Deep Silicon Etching Equipment Market can be categorized based on the type of systems used, namely single-chip and multi-chip systems. Single-chip systems are designed to etch individual silicon wafers, making them ideal for applications that require high precision and customization. These systems are commonly used in research and development settings, as well as in the production of specialized devices where each wafer may have unique specifications. Single-chip systems offer the advantage of precise control over the etching process, allowing for the creation of intricate patterns and structures with high accuracy. On the other hand, multi-chip systems are designed to etch multiple silicon wafers simultaneously, making them suitable for high-volume production environments. These systems are often used in the manufacturing of standardized devices where uniformity and efficiency are critical. Multi-chip systems can significantly reduce production time and costs by processing several wafers at once, making them a preferred choice for large-scale semiconductor manufacturers. Both single-chip and multi-chip systems play a crucial role in the DRIE market, catering to different needs and applications within the semiconductor industry. The choice between single-chip and multi-chip systems depends on factors such as production volume, precision requirements, and cost considerations. As the demand for advanced semiconductor devices continues to grow, the market for both types of DRIE systems is expected to expand, driven by the need for efficient and precise silicon etching solutions.

MEMS, IC Manufacturing, Optical and Optoelectronic Devices, Biomedical Field, Other in the Global DRIE Deep Silicon Etching Equipment Market:

The Global DRIE Deep Silicon Etching Equipment Market finds extensive usage across various fields, including MEMS, IC manufacturing, optical and optoelectronic devices, the biomedical field, and other applications. In the MEMS sector, DRIE technology is essential for creating micro-scale mechanical structures such as sensors, actuators, and resonators. These components are used in a wide range of applications, from automotive systems to consumer electronics, where their small size and high performance are critical. In IC manufacturing, DRIE equipment is used to etch deep trenches and vias in silicon wafers, which are necessary for creating advanced semiconductor devices with high-density interconnections. This process is crucial for the development of next-generation integrated circuits that require precise and reliable etching techniques. Optical and optoelectronic devices, such as photonic crystals and waveguides, also benefit from DRIE technology. The ability to create deep and precise structures in silicon allows for the development of high-performance optical components used in telecommunications, data centers, and other high-speed communication systems. In the biomedical field, DRIE equipment is used to fabricate microfluidic devices, lab-on-a-chip systems, and other medical devices that require precise and intricate silicon structures. These devices are used in diagnostics, drug delivery, and other medical applications where miniaturization and precision are essential. Additionally, DRIE technology is used in various other applications, including the fabrication of power devices, RF components, and advanced packaging solutions. The versatility and precision of DRIE equipment make it a valuable tool in the development of a wide range of advanced technologies, driving its demand across multiple industries.

Global DRIE Deep Silicon Etching Equipment Market Outlook:

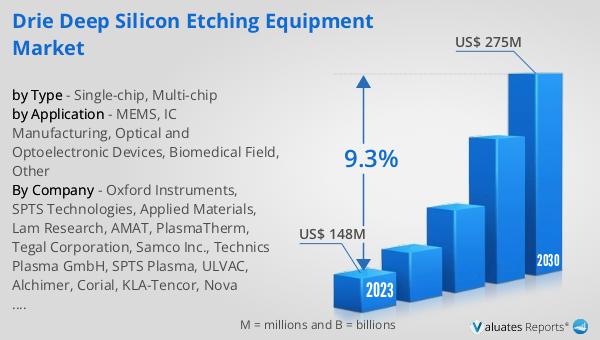

The global DRIE Deep Silicon Etching Equipment market was valued at US$ 148 million in 2023 and is anticipated to reach US$ 275 million by 2030, witnessing a CAGR of 9.3% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for advanced semiconductor devices and the critical role that DRIE technology plays in their production. As industries continue to push the boundaries of miniaturization and performance, the need for precise and efficient silicon etching solutions becomes more pronounced. The market's expansion is driven by the growing adoption of MEMS, the development of next-generation integrated circuits, and the rising demand for high-performance optical and optoelectronic devices. Additionally, advancements in biomedical technology and other emerging applications further contribute to the market's growth. The continuous innovation and development of DRIE equipment are expected to meet the evolving needs of various industries, ensuring the market's sustained growth in the coming years.

| Report Metric | Details |

| Report Name | DRIE Deep Silicon Etching Equipment Market |

| Accounted market size in 2023 | US$ 148 million |

| Forecasted market size in 2030 | US$ 275 million |

| CAGR | 9.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Oxford Instruments, SPTS Technologies, Applied Materials, Lam Research, AMAT, PlasmaTherm, Tegal Corporation, Samco Inc., Technics Plasma GmbH, SPTS Plasma, ULVAC, Alchimer, Corial, KLA-Tencor, Nova Measuring Instruments, Plasmetrex, Hitachi High-Tech Corporation, SEMIFAB, Sentech Instruments, PVA TePla AG |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |