What is Global Circular Surgical Staplers Market?

The Global Circular Surgical Staplers Market refers to the worldwide industry focused on the production and distribution of circular surgical staplers. These specialized medical devices are used primarily in surgical procedures to close wounds or connect tissues, such as in gastrointestinal surgeries. Unlike traditional suturing methods, circular surgical staplers offer precision, speed, and consistency, which can significantly reduce operation times and improve patient outcomes. The market encompasses a variety of products, including both disposable and reusable staplers, catering to different surgical needs and preferences. Factors driving the growth of this market include advancements in surgical techniques, increasing prevalence of chronic diseases requiring surgical intervention, and a growing aging population. Additionally, the market is influenced by regulatory standards, technological innovations, and the competitive landscape among key players. As healthcare systems globally strive for better efficiency and patient care, the demand for reliable and effective surgical tools like circular staplers continues to rise.

Disposable, Reusable in the Global Circular Surgical Staplers Market:

In the Global Circular Surgical Staplers Market, products are broadly categorized into disposable and reusable staplers. Disposable circular surgical staplers are designed for single-use, ensuring sterility and reducing the risk of cross-contamination between patients. These staplers are particularly favored in settings where infection control is paramount, such as in hospitals with high patient turnover or in surgeries involving immunocompromised patients. The convenience of disposable staplers lies in their ready-to-use nature, eliminating the need for sterilization processes and thus saving time and resources. On the other hand, reusable circular surgical staplers are designed for multiple uses, provided they are properly sterilized between procedures. These staplers are often constructed from more durable materials to withstand repeated sterilization cycles. While the initial cost of reusable staplers is higher, they can be more cost-effective in the long run, especially in high-volume surgical centers. The choice between disposable and reusable staplers often depends on factors such as the healthcare facility's budget, the volume of surgeries performed, and specific patient safety protocols. Both types of staplers play a crucial role in the surgical toolkit, offering flexibility and options to meet diverse clinical needs.

Hospital, ASCs, Other in the Global Circular Surgical Staplers Market:

The usage of circular surgical staplers in hospitals, ambulatory surgical centers (ASCs), and other healthcare settings highlights their versatility and importance in modern surgical practices. In hospitals, circular surgical staplers are extensively used due to the wide range of complex surgeries performed, including gastrointestinal, thoracic, and colorectal procedures. Hospitals benefit from the efficiency and reliability of these staplers, which help reduce operation times and improve patient recovery rates. In ASCs, which focus on providing same-day surgical care, the use of circular surgical staplers is equally critical. These centers prioritize quick turnaround times and high patient throughput, making the speed and precision of circular staplers invaluable. The ability to perform surgeries efficiently without compromising on safety or outcomes is a key advantage in ASCs. Other healthcare settings, such as specialized clinics and outpatient centers, also utilize circular surgical staplers for various procedures. These settings may not have the same volume of surgeries as hospitals or ASCs, but they still require reliable surgical tools to ensure patient safety and successful outcomes. Overall, the adoption of circular surgical staplers across different healthcare environments underscores their essential role in enhancing surgical efficiency and patient care.

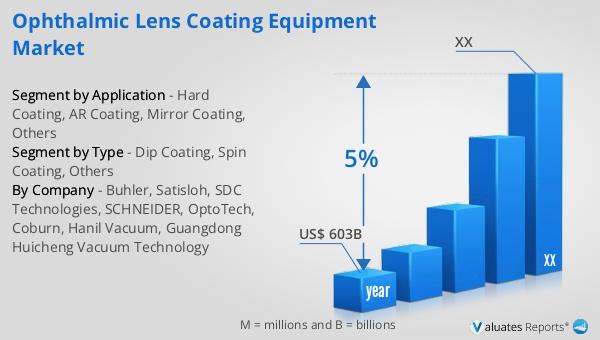

Global Circular Surgical Staplers Market Outlook:

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth trajectory reflects the increasing demand for advanced medical technologies and innovations that improve patient care and outcomes. The medical device industry encompasses a wide range of products, from diagnostic equipment to surgical instruments, each playing a vital role in modern healthcare. Factors contributing to this market expansion include technological advancements, rising healthcare expenditures, and an aging global population that requires more medical interventions. Additionally, the ongoing development of minimally invasive surgical techniques and the integration of digital health solutions are driving the adoption of new medical devices. As healthcare systems worldwide continue to evolve, the need for efficient, reliable, and cutting-edge medical devices will remain a key driver of market growth.

| Report Metric | Details |

| Report Name | Circular Surgical Staplers Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Medtronic, Johnson & Johnson, B. Braun, Meril Life Sciences, Frankenman International, Reach Surgical, Victor Medical Instruments, Changzhou Ankang Medical Instruments, SURKON Medical, Microcure, Zhejiang Geyi Medical Instrument, Panther Healthcare |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |