What is Traditional Ceramics - Global Market?

Traditional ceramics refer to materials made from naturally occurring raw materials like clay, silica, and feldspar, which are then shaped and fired at high temperatures to achieve desired properties. These ceramics have been used for thousands of years and include products such as tiles, sanitary ware, tableware, and other items. The global market for traditional ceramics is vast and diverse, encompassing a wide range of applications in both residential and commercial settings. The market is driven by factors such as urbanization, increasing construction activities, and the growing demand for aesthetically pleasing and durable materials. Traditional ceramics are known for their durability, resistance to high temperatures, and aesthetic appeal, making them a popular choice in various industries. The market is also influenced by technological advancements and innovations in manufacturing processes, which have led to the development of new and improved ceramic products. Overall, the traditional ceramics market is a dynamic and evolving sector with significant growth potential in the coming years.

Ceramic Tiles, Ceramic Sanitary Ware, Ceramic Tableware, Others in the Traditional Ceramics - Global Market:

Ceramic tiles are one of the most common products in the traditional ceramics market. They are widely used in residential and commercial buildings for flooring, walls, and countertops due to their durability, ease of maintenance, and aesthetic appeal. Ceramic tiles come in various sizes, colors, and designs, making them a versatile choice for different applications. Ceramic sanitary ware includes products like toilets, sinks, and bathtubs, which are essential components of modern bathrooms. These products are valued for their hygiene, durability, and ease of cleaning. Ceramic sanitary ware is available in various designs and styles, catering to different consumer preferences and needs. Ceramic tableware includes items like plates, bowls, cups, and saucers, which are used for dining purposes. These products are appreciated for their aesthetic appeal, durability, and resistance to stains and scratches. Ceramic tableware is available in a wide range of designs, from traditional to contemporary, catering to different tastes and preferences. Other traditional ceramic products include items like ceramic pots, vases, and decorative pieces, which are used for both functional and decorative purposes. These products are valued for their aesthetic appeal, durability, and versatility. The global market for traditional ceramics is driven by factors such as increasing urbanization, rising disposable incomes, and growing consumer preference for aesthetically pleasing and durable products. Technological advancements and innovations in manufacturing processes have also contributed to the growth of the market by enabling the production of high-quality ceramic products at competitive prices. Overall, the traditional ceramics market is a dynamic and evolving sector with significant growth potential in the coming years.

Residential, Commercial in the Traditional Ceramics - Global Market:

Traditional ceramics are widely used in both residential and commercial settings due to their durability, aesthetic appeal, and versatility. In residential settings, traditional ceramics are commonly used for flooring, walls, countertops, and bathroom fixtures. Ceramic tiles are a popular choice for flooring and walls due to their durability, ease of maintenance, and wide range of designs and colors. They are also used for kitchen countertops and backsplashes, providing a durable and aesthetically pleasing surface that is resistant to stains and scratches. Ceramic sanitary ware, including toilets, sinks, and bathtubs, is an essential component of modern bathrooms, valued for its hygiene, durability, and ease of cleaning. Ceramic tableware, including plates, bowls, cups, and saucers, is widely used in households for dining purposes, appreciated for its aesthetic appeal and durability. In commercial settings, traditional ceramics are used in various applications, including flooring, walls, countertops, and bathroom fixtures in offices, hotels, restaurants, and retail spaces. Ceramic tiles are a popular choice for commercial flooring and walls due to their durability, ease of maintenance, and wide range of designs and colors. They are also used for countertops and backsplashes in commercial kitchens, providing a durable and aesthetically pleasing surface that is resistant to stains and scratches. Ceramic sanitary ware is commonly used in commercial bathrooms, valued for its hygiene, durability, and ease of cleaning. Ceramic tableware is widely used in restaurants and hotels for dining purposes, appreciated for its aesthetic appeal and durability. Overall, the versatility, durability, and aesthetic appeal of traditional ceramics make them a popular choice in both residential and commercial settings.

Traditional Ceramics - Global Market Outlook:

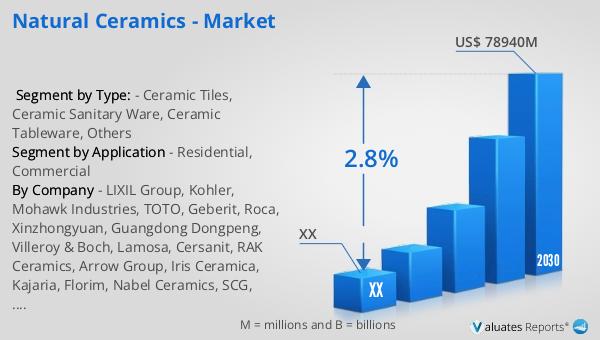

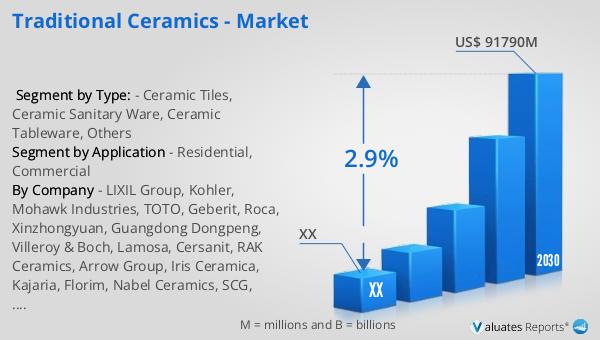

The global market for traditional ceramics was valued at approximately US$ 75,000 million in 2023 and is projected to reach around US$ 91,790 million by 2030, growing at a compound annual growth rate (CAGR) of 2.9% during the forecast period from 2024 to 2030. The Asia-Pacific region is the largest consumer of traditional ceramics, followed by North America and Europe. This growth is driven by factors such as increasing urbanization, rising disposable incomes, and growing consumer preference for aesthetically pleasing and durable products. Technological advancements and innovations in manufacturing processes have also contributed to the growth of the market by enabling the production of high-quality ceramic products at competitive prices. The market is also influenced by factors such as government regulations, environmental concerns, and changing consumer preferences. Overall, the traditional ceramics market is a dynamic and evolving sector with significant growth potential in the coming years.

| Report Metric | Details |

| Report Name | Traditional Ceramics - Market |

| Forecasted market size in 2030 | US$ 91790 million |

| CAGR | 2.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | LIXIL Group, Kohler, Mohawk Industries, TOTO, Geberit, Roca, Xinzhongyuan, Guangdong Dongpeng, Villeroy & Boch, Lamosa, Cersanit, RAK Ceramics, Arrow Group, Iris Ceramica, Kajaria, Florim, Nabel Ceramics, SCG, Fortune Brands Home & Security, Casalgrande Padana, Jinduo, Concorde, Pamesa, Huida, Newpearl, Cooperativa Ceramica d'Imola, Tidiy, Guangdong BODE, Monalisa, Sanfi |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |