What is Global Flame Retardant Polypropylene Market?

The Global Flame Retardant Polypropylene Market refers to the worldwide industry focused on the production and distribution of polypropylene materials that are treated with flame retardant additives. Polypropylene is a versatile plastic widely used in various applications due to its durability, chemical resistance, and cost-effectiveness. However, its inherent flammability poses a significant risk in many applications, necessitating the use of flame retardants to enhance safety. The market encompasses a range of products designed to meet stringent fire safety standards across different industries, including electrical appliances, automotive, and construction. These flame retardant polypropylene materials are engineered to reduce the risk of ignition and slow down the spread of fire, thereby providing critical safety benefits. The market is driven by increasing regulatory requirements, growing awareness about fire safety, and the rising demand for safer materials in various applications. As industries continue to prioritize safety and compliance, the Global Flame Retardant Polypropylene Market is expected to witness significant growth, driven by advancements in flame retardant technologies and the development of more effective and environmentally friendly additives.

Halogen Flame Retardant PP, Halogen Free Flame Retardant PP in the Global Flame Retardant Polypropylene Market:

Halogen Flame Retardant Polypropylene (PP) and Halogen-Free Flame Retardant PP are two primary categories within the Global Flame Retardant Polypropylene Market, each with distinct characteristics and applications. Halogen Flame Retardant PP incorporates halogen-based compounds, such as bromine or chlorine, to achieve flame retardancy. These compounds are highly effective in inhibiting the combustion process by releasing halogen radicals that interfere with the chemical reactions occurring during a fire. As a result, Halogen Flame Retardant PP is widely used in applications where high levels of fire resistance are required, such as in electrical appliances and automotive components. However, the use of halogen-based flame retardants has raised environmental and health concerns due to the potential release of toxic gases and persistent organic pollutants during combustion. This has led to increased regulatory scrutiny and a growing demand for safer alternatives. In response to these concerns, Halogen-Free Flame Retardant PP has emerged as a viable alternative. Halogen-Free Flame Retardant PP utilizes non-halogenated compounds, such as phosphorus, nitrogen, or mineral-based additives, to achieve flame retardancy. These additives work by promoting char formation, diluting flammable gases, or creating a protective barrier that slows down the spread of fire. Halogen-Free Flame Retardant PP offers several advantages, including reduced toxicity, lower environmental impact, and compliance with stringent fire safety regulations. It is increasingly preferred in applications where environmental sustainability and human health are paramount, such as in consumer electronics, construction materials, and textiles. The shift towards Halogen-Free Flame Retardant PP is driven by the growing awareness of the environmental and health risks associated with halogenated flame retardants, as well as the increasing adoption of green building standards and eco-friendly practices. Both Halogen and Halogen-Free Flame Retardant PP play crucial roles in enhancing fire safety across various industries, and their continued development and adoption are essential for meeting the evolving demands of the Global Flame Retardant Polypropylene Market.

Electrical Appliances, Automotive, Others in the Global Flame Retardant Polypropylene Market:

The usage of Global Flame Retardant Polypropylene Market spans across several key areas, including electrical appliances, automotive, and other sectors. In the realm of electrical appliances, flame retardant polypropylene is extensively used to enhance the safety of products such as household appliances, consumer electronics, and electrical enclosures. These applications require materials that can withstand high temperatures and prevent the spread of fire, ensuring the safety of users and compliance with stringent fire safety standards. Flame retardant polypropylene provides an ideal solution due to its excellent balance of mechanical properties, cost-effectiveness, and fire resistance. In the automotive industry, flame retardant polypropylene is utilized in various components, including interior parts, under-the-hood applications, and electrical systems. The automotive sector demands materials that can endure harsh conditions, resist ignition, and minimize the risk of fire in the event of an accident or electrical malfunction. Flame retardant polypropylene meets these requirements by offering high thermal stability, low smoke emission, and effective flame retardancy. Its use in automotive applications contributes to the overall safety and reliability of vehicles, addressing the growing emphasis on passenger safety and regulatory compliance. Beyond electrical appliances and automotive, flame retardant polypropylene finds applications in other sectors such as construction, textiles, and packaging. In the construction industry, it is used in building materials, insulation, and wiring systems to enhance fire safety in residential and commercial structures. The textile industry benefits from flame retardant polypropylene in the production of protective clothing, upholstery, and carpets, where fire resistance is crucial. Additionally, flame retardant polypropylene is employed in packaging materials to ensure the safe transportation and storage of flammable goods. The versatility and effectiveness of flame retardant polypropylene make it a valuable material across diverse industries, driving its demand and growth in the Global Flame Retardant Polypropylene Market.

Global Flame Retardant Polypropylene Market Outlook:

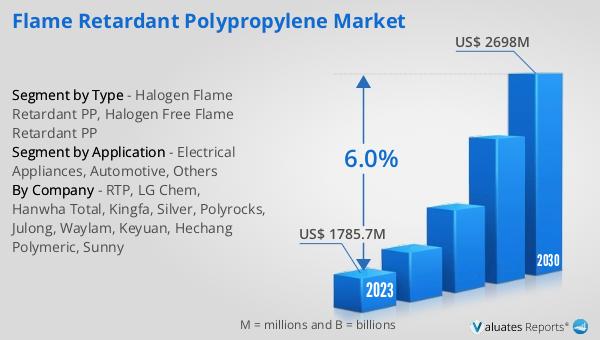

The global Flame Retardant Polypropylene market is anticipated to grow significantly, with projections indicating it will reach approximately US$ 2698 million by 2030, up from an estimated US$ 1902 million in 2024. This growth represents a compound annual growth rate (CAGR) of 6.0% between 2024 and 2030. This upward trend underscores the increasing demand for flame retardant polypropylene materials across various industries, driven by the need for enhanced fire safety and regulatory compliance. The market's expansion is fueled by advancements in flame retardant technologies, the development of more effective and environmentally friendly additives, and the growing awareness of fire safety risks. As industries continue to prioritize safety and sustainability, the demand for flame retardant polypropylene is expected to rise, contributing to the market's robust growth. The projected growth figures highlight the significant opportunities within the Global Flame Retardant Polypropylene Market, emphasizing the importance of continued innovation and investment in this critical area.

| Report Metric | Details |

| Report Name | Flame Retardant Polypropylene Market |

| Accounted market size in 2024 | an estimated US$ 1902 million |

| Forecasted market size in 2030 | US$ 2698 million |

| CAGR | 6.0% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | RTP, LG Chem, Hanwha Total, Kingfa, Silver, Polyrocks, Julong, Waylam, Keyuan, Hechang Polymeric, Sunny |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |