What is Global Anti-counterfeit Package Market?

The Global Anti-counterfeit Package Market is a rapidly growing sector focused on combating the proliferation of counterfeit goods across various industries. Counterfeit products pose significant risks to consumer safety, brand reputation, and economic stability. This market encompasses a wide range of technologies and solutions designed to authenticate products and ensure their traceability throughout the supply chain. These solutions include holograms, watermarks, RFID tags, and barcodes, among others. The primary goal is to provide a secure and reliable means of verifying the authenticity of products, thereby protecting both consumers and manufacturers from the adverse effects of counterfeit goods. As global trade continues to expand and e-commerce becomes increasingly prevalent, the demand for robust anti-counterfeit packaging solutions is expected to rise, driving innovation and growth within this market.

Authentication, Track and Trace in the Global Anti-counterfeit Package Market:

Authentication and Track and Trace are two critical components of the Global Anti-counterfeit Package Market. Authentication involves verifying the legitimacy of a product through various techniques and technologies. This can include the use of holograms, watermarks, and special inks that are difficult to replicate. These features are often integrated into the packaging or the product itself, providing a visible and immediate means of verification for consumers and retailers. For instance, holograms can be embedded in labels or packaging materials, offering a unique visual identifier that is challenging for counterfeiters to duplicate. Similarly, watermarks and special inks can be used to create patterns or images that are only visible under certain conditions, such as UV light, adding an extra layer of security. Track and Trace, on the other hand, focuses on monitoring the movement of products through the supply chain. This involves the use of technologies like RFID tags, barcodes, and QR codes to record and track the journey of a product from the manufacturer to the end consumer. Each product is assigned a unique identifier, which is scanned and recorded at various points along the supply chain. This data is then stored in a centralized database, allowing manufacturers, distributors, and retailers to verify the product's authenticity and trace its history. For example, RFID tags can be embedded in packaging or attached to products, enabling real-time tracking and monitoring. Barcodes and QR codes can be scanned using handheld devices or smartphones, providing instant access to information about the product's origin, manufacturing date, and distribution history. The integration of Authentication and Track and Trace technologies provides a comprehensive solution for combating counterfeiting. By combining visible security features with digital tracking capabilities, manufacturers can create a multi-layered defense against counterfeiters. This not only helps in identifying and removing counterfeit products from the market but also deters counterfeiters by making it more difficult and costly to replicate genuine products. Additionally, these technologies enable better inventory management and supply chain transparency, reducing the risk of product recalls and ensuring that consumers receive safe and authentic products. In the context of the Global Anti-counterfeit Package Market, these technologies are being increasingly adopted across various industries, including pharmaceuticals, food and beverages, electronics, and luxury goods. The pharmaceutical industry, for example, faces significant challenges with counterfeit drugs, which can have serious health implications for consumers. By implementing Authentication and Track and Trace solutions, pharmaceutical companies can ensure that their products are genuine and safe for consumption. Similarly, in the food and beverage industry, these technologies can help prevent the distribution of counterfeit or substandard products, protecting consumers from potential health risks and preserving brand integrity. Overall, the combination of Authentication and Track and Trace technologies represents a powerful tool in the fight against counterfeiting. As the Global Anti-counterfeit Package Market continues to evolve, these solutions will play a crucial role in safeguarding consumer safety, protecting brand reputation, and ensuring the integrity of global supply chains.

Food and Beverages, Pharmaceutical and Healthcare, Industrial and Automotive, Consumer Electronics, Cosmetics and Personal Care, Clothing and Apparel, Others in the Global Anti-counterfeit Package Market:

The Global Anti-counterfeit Package Market finds extensive applications across various sectors, including Food and Beverages, Pharmaceutical and Healthcare, Industrial and Automotive, Consumer Electronics, Cosmetics and Personal Care, Clothing and Apparel, and others. In the Food and Beverages sector, anti-counterfeit packaging solutions are crucial for ensuring the safety and authenticity of products. Counterfeit food and beverages can pose significant health risks to consumers, and the use of technologies such as holograms, RFID tags, and QR codes helps in verifying the authenticity of these products. For instance, QR codes on packaging can be scanned by consumers to access information about the product's origin, ingredients, and manufacturing process, providing assurance of its authenticity. In the Pharmaceutical and Healthcare sector, the importance of anti-counterfeit packaging cannot be overstated. Counterfeit drugs and medical devices can have severe consequences for patient health and safety. Anti-counterfeit technologies such as holograms, special inks, and RFID tags are used to secure pharmaceutical products and ensure their traceability throughout the supply chain. These solutions help in preventing the distribution of counterfeit drugs and enable healthcare providers and consumers to verify the authenticity of medications, thereby reducing the risk of adverse health outcomes. The Industrial and Automotive sector also benefits from anti-counterfeit packaging solutions. Counterfeit automotive parts can compromise vehicle safety and performance, leading to potential accidents and costly repairs. Anti-counterfeit technologies such as holograms, barcodes, and RFID tags are used to authenticate automotive parts and ensure their traceability from the manufacturer to the end consumer. This helps in preventing the distribution of counterfeit parts and ensures that consumers receive genuine and high-quality products. In the Consumer Electronics sector, anti-counterfeit packaging solutions are essential for protecting brand reputation and ensuring product quality. Counterfeit electronics can pose safety risks and result in poor performance, leading to customer dissatisfaction. Anti-counterfeit technologies such as holograms, QR codes, and RFID tags are used to secure electronic products and verify their authenticity. These solutions help in preventing the distribution of counterfeit electronics and enable consumers to verify the authenticity of their purchases, ensuring that they receive genuine and reliable products. The Cosmetics and Personal Care sector also faces challenges with counterfeit products, which can pose health risks to consumers and damage brand reputation. Anti-counterfeit packaging solutions such as holograms, special inks, and RFID tags are used to secure cosmetic products and ensure their authenticity. These technologies help in preventing the distribution of counterfeit cosmetics and enable consumers to verify the authenticity of their purchases, ensuring that they receive safe and high-quality products. In the Clothing and Apparel sector, anti-counterfeit packaging solutions are used to protect brand reputation and ensure product authenticity. Counterfeit clothing and accessories can result in poor quality and customer dissatisfaction. Anti-counterfeit technologies such as holograms, QR codes, and RFID tags are used to secure clothing and apparel products and verify their authenticity. These solutions help in preventing the distribution of counterfeit clothing and enable consumers to verify the authenticity of their purchases, ensuring that they receive genuine and high-quality products. Overall, the Global Anti-counterfeit Package Market plays a crucial role in ensuring the authenticity and safety of products across various sectors. By implementing advanced anti-counterfeit technologies, manufacturers can protect their brand reputation, ensure product quality, and safeguard consumer health and safety.

Global Anti-counterfeit Package Market Outlook:

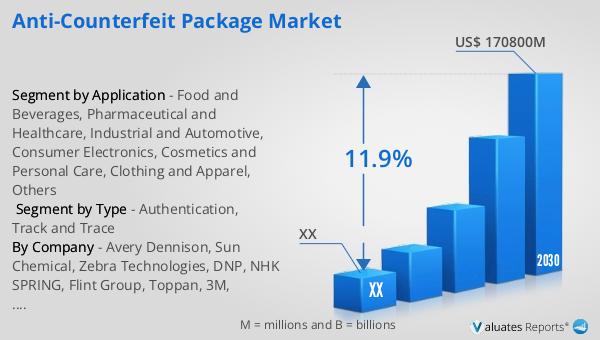

The global market for Anti-counterfeit Package was valued at approximately US$ 77,050 million in 2023 and is projected to reach an adjusted size of US$ 170,800 million by 2030, with a compound annual growth rate (CAGR) of 11.9% during the forecast period from 2024 to 2030. Leading manufacturers in this industry include Avery Dennison, Sun Chemical, and Zebra Technologies, which contribute 2.98%, 1.68%, and 1.57% of the revenue, respectively. In terms of regional distribution, the Asia Pacific region held the largest share of income in 2019, accounting for more than 33.5 percent.

| Report Metric | Details |

| Report Name | Anti-counterfeit Package Market |

| Forecasted market size in 2030 | US$ 170800 million |

| CAGR | 11.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Avery Dennison, Sun Chemical, Zebra Technologies, DNP, NHK SPRING, Flint Group, Toppan, 3M, Essentra, Alien Technology Corp, KURZ, OpSec Security, Lipeng, Shiner, Taibao, Invengo, De La Rue, Schreiner ProSecure, CFC, UPM Raflatac, Techsun, Impinj, G&D, Catalent Pharma Solution, SICPA, CCL |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |