What is Global Filtered Pipette Tips Market?

The global filtered pipette tips market is a specialized segment within the broader laboratory equipment industry. Filtered pipette tips are essential tools used in various scientific and medical laboratories to ensure precision and accuracy in liquid handling tasks. These tips are designed with built-in filters that prevent contamination by blocking aerosols and liquids from entering the pipette shaft. This feature is particularly crucial in applications where cross-contamination can compromise the integrity of experiments or diagnostic results. The market for filtered pipette tips is driven by the increasing demand for high-quality laboratory consumables, advancements in biotechnology, and the growing emphasis on maintaining sterile conditions in research and clinical settings. As laboratories worldwide continue to adopt stringent quality control measures, the need for reliable and contamination-free pipette tips is expected to rise, making the global filtered pipette tips market a vital component of the scientific community.

Manual LH Systems Pipette Tips, Automated LH Systems Pipette Tips in the Global Filtered Pipette Tips Market:

Manual liquid handling (LH) systems pipette tips and automated liquid handling systems pipette tips are two primary categories within the global filtered pipette tips market. Manual LH systems pipette tips are designed for use with handheld pipettes, which are commonly employed in laboratories for tasks requiring precision and control. These tips are favored for their ease of use, affordability, and versatility in various applications, including sample preparation, reagent dispensing, and serial dilutions. Manual pipette tips are often used in smaller laboratories or in situations where the volume of liquid handling tasks does not justify the investment in automated systems. On the other hand, automated LH systems pipette tips are engineered for use with robotic pipetting systems, which are increasingly being adopted in high-throughput laboratories. These tips are designed to work seamlessly with automated platforms, ensuring consistent and accurate liquid handling across numerous samples. Automated pipette tips are essential in applications that require high precision, such as genomic research, drug discovery, and clinical diagnostics. The use of automated systems reduces the risk of human error, increases throughput, and enhances reproducibility, making them indispensable in large-scale research and industrial settings. Both manual and automated pipette tips are available in various sizes and materials to cater to different laboratory needs. They are typically made from high-quality polypropylene and are available in sterile and non-sterile versions. The choice between manual and automated pipette tips depends on factors such as the volume of liquid handling tasks, the level of precision required, and the available budget. As the demand for high-quality and contamination-free pipette tips continues to grow, manufacturers are focusing on developing innovative products that meet the evolving needs of the scientific community. This includes the introduction of low-retention tips, which minimize sample loss, and eco-friendly tips made from recyclable materials. The global filtered pipette tips market is characterized by intense competition, with numerous players vying for market share. Leading companies are investing in research and development to introduce advanced products that offer superior performance and reliability. Additionally, strategic collaborations and partnerships are common in this market, as companies seek to expand their product portfolios and enhance their market presence. Overall, the global filtered pipette tips market is poised for significant growth, driven by the increasing demand for high-quality laboratory consumables and the ongoing advancements in biotechnology and life sciences research.

Industrials, Research Institutions, Hospital, Others in the Global Filtered Pipette Tips Market:

The usage of filtered pipette tips in various sectors such as industrials, research institutions, hospitals, and others highlights their versatility and importance in maintaining the integrity of scientific and medical work. In industrial settings, filtered pipette tips are crucial for quality control and assurance processes. Industries such as pharmaceuticals, food and beverage, and chemicals rely on precise liquid handling to ensure product consistency and safety. Filtered pipette tips help prevent contamination during sample preparation and analysis, thereby maintaining the accuracy of test results and ensuring compliance with regulatory standards. In research institutions, filtered pipette tips are indispensable tools for a wide range of scientific investigations. They are used in molecular biology, biochemistry, and microbiology labs for tasks such as PCR setup, DNA/RNA extraction, and enzyme assays. The built-in filters in these tips prevent cross-contamination between samples, which is critical for obtaining reliable and reproducible results. Researchers depend on the precision and reliability of filtered pipette tips to advance scientific knowledge and develop new technologies. Hospitals and clinical laboratories also heavily rely on filtered pipette tips for diagnostic and therapeutic purposes. In clinical diagnostics, these tips are used for handling patient samples, preparing reagents, and conducting various assays. The prevention of contamination is paramount in clinical settings to ensure accurate diagnosis and effective treatment. Filtered pipette tips help maintain the sterility of samples and reagents, thereby reducing the risk of diagnostic errors and improving patient outcomes. Additionally, filtered pipette tips are used in other sectors such as environmental testing, forensic science, and academic laboratories. In environmental testing, they are used for analyzing water, soil, and air samples to detect pollutants and contaminants. Forensic scientists use filtered pipette tips for handling evidence samples, ensuring that the integrity of the samples is preserved for accurate analysis. Academic laboratories use these tips for teaching and research purposes, providing students and researchers with reliable tools for their experiments. Overall, the usage of filtered pipette tips across various sectors underscores their importance in ensuring the accuracy, reliability, and reproducibility of scientific and medical work. As the demand for high-quality laboratory consumables continues to grow, the global filtered pipette tips market is expected to expand, driven by the need for contamination-free liquid handling solutions in diverse applications.

Global Filtered Pipette Tips Market Outlook:

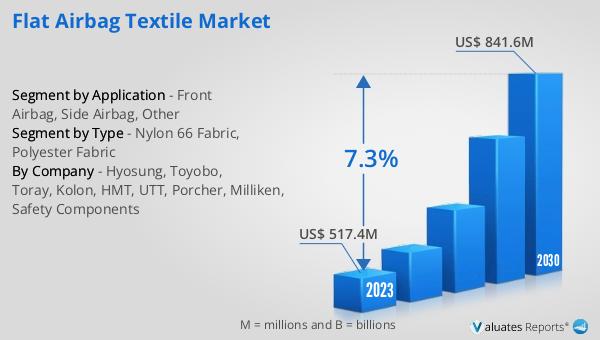

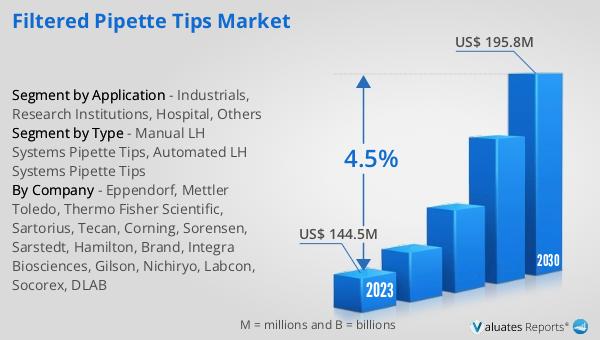

The global filtered pipette tips market was valued at $144.5 million in 2023 and is projected to reach $195.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2024 to 2030. This growth trajectory underscores the increasing demand for high-quality, contamination-free pipette tips across various sectors, including industrials, research institutions, hospitals, and others. The market's expansion is driven by the rising emphasis on maintaining sterile conditions in laboratories, advancements in biotechnology, and the growing need for precision and accuracy in liquid handling tasks. As laboratories worldwide adopt more stringent quality control measures, the demand for reliable and high-performance pipette tips is expected to rise. The market outlook indicates a robust growth potential, with manufacturers focusing on developing innovative products to meet the evolving needs of the scientific community. The projected growth also highlights the importance of filtered pipette tips in ensuring the integrity of scientific and medical work, making them a vital component of the laboratory equipment industry.

| Report Metric | Details |

| Report Name | Filtered Pipette Tips Market |

| Accounted market size in 2023 | US$ 144.5 million |

| Forecasted market size in 2030 | US$ 195.8 million |

| CAGR | 4.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Eppendorf, Mettler Toledo, Thermo Fisher Scientific, Sartorius, Tecan, Corning, Sorensen, Sarstedt, Hamilton, Brand, Integra Biosciences, Gilson, Nichiryo, Labcon, Socorex, DLAB |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |