What is Global Plastic Doctor Blade Market?

The Global Plastic Doctor Blade Market refers to the industry that manufactures and distributes plastic doctor blades, which are essential components in various printing processes. Doctor blades are thin, flexible blades used to remove excess ink from the surface of printing cylinders, ensuring a clean and precise print. The market encompasses a wide range of plastic materials used to produce these blades, including polyethylene, polypropylene, and other engineered plastics. These materials are chosen for their durability, flexibility, and resistance to wear and chemicals. The market serves various printing industries, including flexographic, gravure, and offset printing, among others. The demand for plastic doctor blades is driven by the need for high-quality printing, cost-effectiveness, and the growing adoption of advanced printing technologies. As the printing industry continues to evolve, the Global Plastic Doctor Blade Market is expected to grow, offering innovative solutions to meet the changing needs of printers worldwide.

Conventional Doctor Blade, Composite Doctor Blade in the Global Plastic Doctor Blade Market:

Conventional doctor blades are typically made from metal, such as steel, and have been widely used in the printing industry for many years. These blades are known for their durability and ability to maintain a sharp edge, which is crucial for achieving high-quality prints. However, they also have some drawbacks, such as the potential to damage printing cylinders and the need for frequent replacement due to wear and tear. On the other hand, composite doctor blades are made from a combination of materials, including plastics and other engineered materials. These blades offer several advantages over conventional metal blades, such as reduced wear on printing cylinders, longer lifespan, and improved flexibility. In the Global Plastic Doctor Blade Market, composite blades are gaining popularity due to their ability to provide consistent performance and reduce maintenance costs. The use of advanced materials in composite blades also allows for better customization to meet specific printing requirements. As a result, many printers are transitioning from conventional metal blades to composite plastic blades to enhance their printing processes and achieve better results. The shift towards composite blades is also driven by the increasing demand for environmentally friendly and sustainable printing solutions. Composite blades can be designed to minimize waste and reduce the environmental impact of the printing process. Additionally, the development of new composite materials continues to expand the capabilities of plastic doctor blades, making them suitable for a wider range of applications. Overall, the Global Plastic Doctor Blade Market is witnessing a significant transformation as printers adopt composite blades to improve efficiency, reduce costs, and meet the evolving demands of the printing industry.

Flexo, Gravure, Offset Printing, Other in the Global Plastic Doctor Blade Market:

The Global Plastic Doctor Blade Market finds extensive usage in various printing processes, including flexographic, gravure, offset printing, and other specialized applications. In flexographic printing, plastic doctor blades are used to remove excess ink from the anilox roll, ensuring a clean and precise transfer of ink to the printing plate. This process is essential for producing high-quality prints on flexible packaging materials, labels, and other substrates. The flexibility and durability of plastic doctor blades make them ideal for the high-speed and high-volume demands of flexographic printing. In gravure printing, plastic doctor blades play a crucial role in removing excess ink from the engraved cells of the printing cylinder. This ensures that only the desired amount of ink is transferred to the substrate, resulting in sharp and detailed prints. Gravure printing is commonly used for printing on packaging materials, wallpapers, and magazines, where high-quality and consistent prints are required. Plastic doctor blades offer the advantage of reduced wear on the printing cylinder, leading to longer cylinder life and lower maintenance costs. In offset printing, plastic doctor blades are used in the ink fountain to control the amount of ink applied to the printing plate. This process is vital for achieving uniform ink distribution and high-quality prints on paper and other substrates. Offset printing is widely used for producing books, newspapers, brochures, and other printed materials. The use of plastic doctor blades in offset printing helps improve print quality, reduce ink consumption, and minimize downtime due to blade replacement. Additionally, plastic doctor blades are used in other specialized printing applications, such as screen printing and digital printing. In screen printing, plastic doctor blades are used to remove excess ink from the screen, ensuring a clean and precise print. In digital printing, plastic doctor blades are used in various components of the printing system to control ink flow and maintain print quality. The versatility and adaptability of plastic doctor blades make them suitable for a wide range of printing processes, contributing to their growing demand in the Global Plastic Doctor Blade Market.

Global Plastic Doctor Blade Market Outlook:

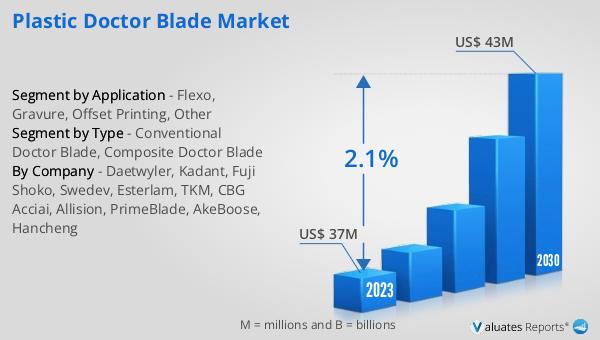

The global Plastic Doctor Blade market was valued at US$ 37 million in 2023 and is anticipated to reach US$ 43 million by 2030, witnessing a CAGR of 2.1% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the industry, driven by the increasing demand for high-quality printing solutions and the adoption of advanced printing technologies. The growth in the market is also supported by the shift towards composite plastic doctor blades, which offer several advantages over conventional metal blades, such as reduced wear on printing cylinders, longer lifespan, and improved flexibility. As printers continue to seek cost-effective and efficient solutions to enhance their printing processes, the demand for plastic doctor blades is expected to rise. The market's growth is further fueled by the expanding applications of plastic doctor blades in various printing processes, including flexographic, gravure, offset, and other specialized printing applications. The versatility and adaptability of plastic doctor blades make them suitable for a wide range of printing needs, contributing to their increasing popularity in the printing industry. Overall, the Global Plastic Doctor Blade Market is poised for steady growth, driven by the ongoing advancements in printing technology and the growing demand for high-quality and sustainable printing solutions.

| Report Metric | Details |

| Report Name | Plastic Doctor Blade Market |

| Accounted market size in 2023 | US$ 37 million |

| Forecasted market size in 2030 | US$ 43 million |

| CAGR | 2.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Daetwyler, Kadant, Fuji Shoko, Swedev, Esterlam, TKM, CBG Acciai, Allision, PrimeBlade, AkeBoose, Hancheng |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |