What is Global New Energy Vehicle Speed Reducer Market?

The Global New Energy Vehicle Speed Reducer Market refers to the industry focused on the production and distribution of speed reducers specifically designed for new energy vehicles (NEVs). NEVs include electric vehicles (EVs), plug-in hybrid electric vehicles (PHEVs), and other vehicles that utilize alternative energy sources instead of traditional internal combustion engines. Speed reducers are crucial components in these vehicles as they help manage the speed and torque of the electric motor, ensuring efficient power transmission to the wheels. This market is driven by the increasing demand for environmentally friendly transportation solutions, advancements in electric vehicle technology, and supportive government policies promoting the adoption of NEVs. The market encompasses various types of speed reducers, including single-stage and multi-stage types, each catering to different performance requirements and vehicle specifications. As the global automotive industry shifts towards sustainable mobility, the New Energy Vehicle Speed Reducer Market is expected to witness significant growth, driven by the rising adoption of electric and hybrid vehicles worldwide.

Single Stage Type, Multi Stage Type in the Global New Energy Vehicle Speed Reducer Market:

In the Global New Energy Vehicle Speed Reducer Market, speed reducers are categorized into two main types: Single Stage Type and Multi Stage Type. Single Stage Type speed reducers are designed to provide a single reduction in speed and are typically used in applications where a moderate reduction ratio is sufficient. These speed reducers are simpler in design, lighter in weight, and generally more cost-effective compared to their multi-stage counterparts. They are suitable for electric vehicles that require a straightforward and efficient transmission system, offering a balance between performance and cost. On the other hand, Multi Stage Type speed reducers involve multiple stages of gear reduction, providing higher reduction ratios and greater torque output. These speed reducers are more complex in design, heavier, and often more expensive, but they offer superior performance in terms of torque management and efficiency. Multi Stage Type speed reducers are ideal for high-performance electric vehicles and applications where precise control over speed and torque is critical. The choice between Single Stage and Multi Stage speed reducers depends on various factors, including the specific requirements of the vehicle, desired performance characteristics, and cost considerations. As the demand for new energy vehicles continues to grow, manufacturers are investing in the development of advanced speed reducer technologies to meet the diverse needs of the market. This includes innovations in materials, design, and manufacturing processes to enhance the efficiency, durability, and overall performance of speed reducers. The ongoing advancements in electric vehicle technology and the increasing focus on sustainable transportation solutions are expected to drive the growth and evolution of the Global New Energy Vehicle Speed Reducer Market in the coming years.

PHEV, BEV in the Global New Energy Vehicle Speed Reducer Market:

The usage of speed reducers in the Global New Energy Vehicle Speed Reducer Market is particularly significant in Plug-in Hybrid Electric Vehicles (PHEVs) and Battery Electric Vehicles (BEVs). In PHEVs, speed reducers play a crucial role in managing the power transmission between the electric motor and the wheels. PHEVs combine an internal combustion engine with an electric motor, and the speed reducer ensures that the electric motor operates efficiently, providing the necessary torque and speed reduction for optimal performance. This is essential for maintaining the balance between the electric and combustion power sources, enhancing the overall efficiency and driving experience of the vehicle. In BEVs, which rely solely on electric power, speed reducers are even more critical. They help in converting the high-speed, low-torque output of the electric motor into a lower-speed, higher-torque output suitable for driving the wheels. This conversion is vital for the smooth and efficient operation of the vehicle, ensuring that the electric motor can deliver the required performance while maintaining energy efficiency. The use of speed reducers in BEVs contributes to the overall range and performance of the vehicle, making them a key component in the design and development of electric drivetrains. As the adoption of PHEVs and BEVs continues to rise, the demand for advanced speed reducer technologies is expected to grow, driving innovation and development in the Global New Energy Vehicle Speed Reducer Market.

Global New Energy Vehicle Speed Reducer Market Outlook:

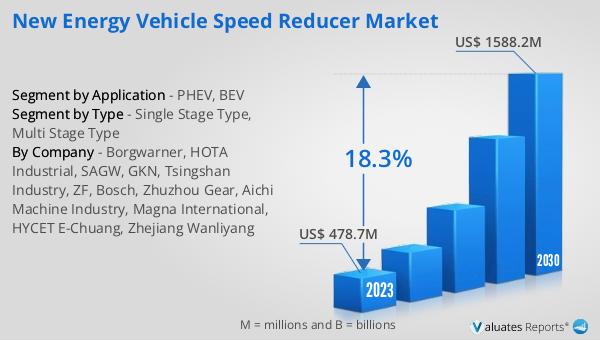

The global New Energy Vehicle Speed Reducer market was valued at US$ 478.7 million in 2023 and is anticipated to reach US$ 1588.2 million by 2030, witnessing a CAGR of 18.3% during the forecast period from 2024 to 2030. The market is dominated by the top three companies, which collectively hold a share of about 40%. China is the largest market for new energy vehicle speed reducers, accounting for over 50% of the global market share. This is followed by Europe and North America, which hold shares of approximately 20% and 10%, respectively. The significant market share in China can be attributed to the country's strong focus on promoting electric vehicles and sustainable transportation solutions. The European and North American markets are also experiencing growth, driven by increasing consumer awareness and supportive government policies. As the global automotive industry continues to shift towards electric and hybrid vehicles, the demand for efficient and reliable speed reducers is expected to rise, further propelling the growth of the Global New Energy Vehicle Speed Reducer Market.

| Report Metric | Details |

| Report Name | New Energy Vehicle Speed Reducer Market |

| Accounted market size in 2023 | US$ 478.7 million |

| Forecasted market size in 2030 | US$ 1588.2 million |

| CAGR | 18.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Borgwarner, HOTA Industrial, SAGW, GKN, Tsingshan Industry, ZF, Bosch, Zhuzhou Gear, Aichi Machine Industry, Magna International, HYCET E-Chuang, Zhejiang Wanliyang |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |