What is Global Anaesthesia Ventilator Market?

The global anaesthesia ventilator market is a specialized segment within the broader medical device industry, focusing on equipment designed to provide respiratory support to patients under anaesthesia. These ventilators are crucial in surgical settings, ensuring that patients receive a controlled supply of oxygen and anaesthetic gases while maintaining adequate ventilation. The market encompasses a variety of ventilator types, including both mobile and fixed units, each tailored to specific medical environments and patient needs. Technological advancements have led to the development of more sophisticated and user-friendly ventilators, enhancing patient safety and operational efficiency. The demand for anaesthesia ventilators is driven by the increasing number of surgical procedures worldwide, the rising prevalence of chronic respiratory diseases, and the growing geriatric population. Additionally, the market is influenced by stringent regulatory standards and the need for compliance with safety protocols, which necessitate continuous innovation and quality improvements. Overall, the global anaesthesia ventilator market plays a vital role in modern healthcare, supporting critical surgical interventions and improving patient outcomes.

Mobile, Fixed in the Global Anaesthesia Ventilator Market:

Mobile anaesthesia ventilators are designed for flexibility and ease of transport, making them ideal for use in various medical settings, including emergency rooms, intensive care units, and during patient transfers. These portable units are equipped with advanced features such as battery backup, compact design, and user-friendly interfaces, allowing healthcare professionals to provide consistent respiratory support even in challenging environments. Mobile ventilators are particularly beneficial in scenarios where immediate and reliable ventilation is required, such as during emergency surgeries or in remote locations with limited access to medical facilities. On the other hand, fixed anaesthesia ventilators are typically installed in operating rooms and intensive care units, offering robust performance and a wide range of functionalities. These stationary units are integrated with hospital infrastructure, providing continuous and precise ventilation support during complex surgical procedures. Fixed ventilators often come with advanced monitoring systems, customizable settings, and enhanced safety features, ensuring optimal patient care. The choice between mobile and fixed ventilators depends on the specific needs of the healthcare facility, the nature of the surgical procedures, and the patient population being served. Both types of ventilators are essential components of the global anaesthesia ventilator market, addressing diverse clinical requirements and contributing to improved patient outcomes.

Hospital, Clinic, Others in the Global Anaesthesia Ventilator Market:

In hospitals, anaesthesia ventilators are indispensable tools used during a wide range of surgical procedures, from minor operations to major surgeries. These ventilators ensure that patients receive a steady supply of oxygen and anaesthetic gases, maintaining proper ventilation and preventing complications such as hypoxia. Hospitals often invest in both mobile and fixed ventilators to cater to different surgical needs and patient conditions. In clinics, anaesthesia ventilators are used for outpatient surgeries and minor procedures that require anaesthesia. Clinics typically prefer mobile ventilators due to their portability and ease of use, allowing for quick setup and efficient patient management. The use of anaesthesia ventilators in clinics helps enhance patient safety and comfort, ensuring that even minor procedures are conducted with the highest standards of care. Other settings where anaesthesia ventilators are used include ambulatory surgical centers, dental offices, and veterinary clinics. In these environments, the ventilators provide essential respiratory support during procedures that require sedation or anaesthesia. The versatility and reliability of anaesthesia ventilators make them valuable assets across various medical settings, contributing to the overall efficiency and effectiveness of healthcare delivery.

Global Anaesthesia Ventilator Market Outlook:

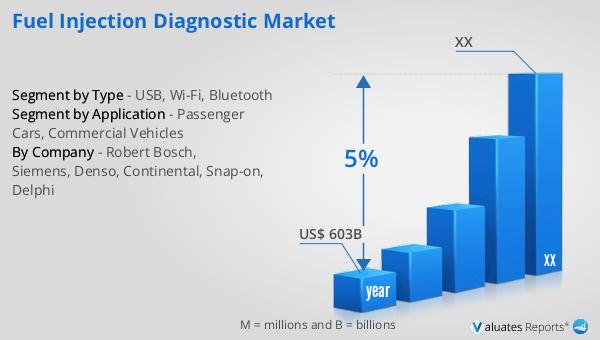

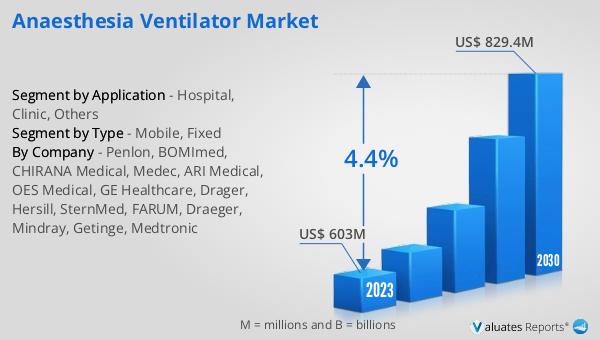

The global anaesthesia ventilator market was valued at US$ 603 million in 2023 and is anticipated to reach US$ 829.4 million by 2030, witnessing a CAGR of 4.4% during the forecast period 2024-2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023, and will be growing at a CAGR of 5% during the next six years. This growth is driven by the increasing demand for advanced medical technologies, the rising prevalence of chronic diseases, and the expanding geriatric population. The anaesthesia ventilator market, in particular, is expected to benefit from these trends, as the need for reliable and efficient respiratory support continues to grow. The market's steady growth reflects the ongoing advancements in medical technology and the critical role that anaesthesia ventilators play in modern healthcare.

| Report Metric | Details |

| Report Name | Anaesthesia Ventilator Market |

| Accounted market size in 2023 | US$ 603 million |

| Forecasted market size in 2030 | US$ 829.4 million |

| CAGR | 4.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Penlon, BOMImed, CHIRANA Medical, Medec, ARI Medical, OES Medical, GE Healthcare, Drager, Hersill, SternMed, FARUM, Draeger, Mindray, Getinge, Medtronic |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

https://reports.valuates.com/market-reports/QYRE-Auto-6T17609/global-99-8-ammonium-nitrate-pure

https://reports.valuates.com/market-reports/QYRE-Auto-6T17609/global-99-8-ammonium-nitrate-pure