What is Global Industrial 3D Printing Materials Market?

The Global Industrial 3D Printing Materials Market refers to the worldwide industry focused on the production and distribution of materials used in 3D printing for industrial applications. These materials are essential for creating three-dimensional objects through additive manufacturing processes. The market encompasses a variety of materials, including plastics, metals, ceramics, and others, each offering unique properties suitable for different industrial needs. The demand for these materials is driven by their ability to produce complex and customized parts with high precision, reduced waste, and lower production costs. Industries such as automotive, aerospace, healthcare, consumer goods, and construction are increasingly adopting 3D printing technologies, thereby fueling the growth of the market. The market is characterized by continuous innovation and advancements in material science, leading to the development of new and improved 3D printing materials that enhance performance and expand application possibilities. As a result, the Global Industrial 3D Printing Materials Market is poised for significant growth, driven by the increasing adoption of 3D printing technologies across various industries and the ongoing advancements in material capabilities.

Plastic, Metal, Ceramic, Others in the Global Industrial 3D Printing Materials Market:

In the Global Industrial 3D Printing Materials Market, plastics, metals, ceramics, and other materials play crucial roles, each offering distinct advantages and applications. Plastics are the most commonly used materials in 3D printing due to their versatility, affordability, and ease of use. They are available in various forms, such as thermoplastics, photopolymers, and bioplastics, each catering to different industrial needs. Thermoplastics like ABS and PLA are popular for their durability and flexibility, making them ideal for prototyping and end-use parts. Photopolymers, on the other hand, are used in stereolithography (SLA) and digital light processing (DLP) technologies, providing high-resolution and detailed prints suitable for intricate designs and molds. Bioplastics, derived from renewable sources, offer an eco-friendly alternative for industries focusing on sustainability. Metals are another significant category in the 3D printing materials market, known for their strength, durability, and ability to withstand high temperatures. Commonly used metals include stainless steel, titanium, aluminum, and cobalt-chrome alloys. These materials are essential for producing high-performance parts in industries such as aerospace, automotive, and healthcare. For instance, titanium is favored in aerospace and medical applications due to its lightweight and biocompatibility properties. Stainless steel and aluminum are widely used in automotive and industrial manufacturing for their robustness and corrosion resistance. Metal 3D printing technologies, such as selective laser melting (SLM) and electron beam melting (EBM), enable the production of complex geometries and customized components that are difficult to achieve with traditional manufacturing methods. Ceramics are gaining traction in the 3D printing materials market due to their unique properties, including high heat resistance, hardness, and biocompatibility. These materials are used in applications requiring high thermal stability and wear resistance, such as aerospace components, medical implants, and electronic devices. Advanced ceramics, like zirconia and alumina, are particularly valued for their mechanical strength and chemical inertness. The use of ceramics in 3D printing allows for the creation of intricate and precise parts that can withstand extreme conditions, making them suitable for specialized industrial applications. In addition to plastics, metals, and ceramics, the market also includes other materials such as composites, resins, and bio-inks. Composites combine the properties of different materials to enhance performance, offering benefits like increased strength, reduced weight, and improved thermal conductivity. Resins, used in vat photopolymerization processes, provide high detail and smooth surface finishes, making them ideal for applications like jewelry, dental models, and prototypes. Bio-inks, composed of living cells and biomaterials, are used in bioprinting to create tissue and organ structures for medical research and regenerative medicine. Overall, the diversity of materials available in the Global Industrial 3D Printing Materials Market enables industries to choose the most suitable options for their specific needs, driving innovation and expanding the possibilities of additive manufacturing. The continuous development of new materials and improvements in existing ones are expected to further enhance the capabilities and applications of 3D printing technologies, contributing to the market's growth and evolution.

Automotive, Aerospace & defense, Healthcare, Consumer Goods, Construction, Others (Electronics, Education, Food, etc.) in the Global Industrial 3D Printing Materials Market:

The usage of Global Industrial 3D Printing Materials Market spans across various industries, each leveraging the unique advantages of 3D printing to enhance their operations and product offerings. In the automotive industry, 3D printing materials are used to produce prototypes, custom parts, and tooling components. The ability to quickly create and test prototypes accelerates the design and development process, allowing manufacturers to bring new models to market faster. Custom parts, such as lightweight components and complex geometries, improve vehicle performance and fuel efficiency. Additionally, 3D printing enables the production of specialized tools and fixtures, reducing lead times and costs associated with traditional manufacturing methods. In the aerospace and defense sector, 3D printing materials are critical for producing lightweight, high-strength components that meet stringent performance and safety standards. Metals like titanium and aluminum are commonly used to manufacture parts such as engine components, brackets, and structural elements. The precision and customization offered by 3D printing allow for the creation of complex geometries that enhance the performance and efficiency of aerospace systems. In defense applications, 3D printing enables the rapid production of mission-critical parts and equipment, ensuring readiness and reducing downtime. The healthcare industry benefits significantly from the Global Industrial 3D Printing Materials Market, particularly in the areas of medical devices, implants, and prosthetics. Biocompatible materials like titanium and advanced polymers are used to create custom implants and prosthetics tailored to individual patients. This customization improves patient outcomes and comfort. Additionally, 3D printing is used to produce surgical guides, dental models, and anatomical models for pre-surgical planning and training. The ability to create complex, patient-specific structures enhances the precision and effectiveness of medical procedures. Consumer goods manufacturers leverage 3D printing materials to produce customized products, prototypes, and small-batch production runs. The flexibility of 3D printing allows for the creation of unique and personalized items, such as jewelry, eyewear, and home decor. This customization appeals to consumers seeking one-of-a-kind products. Additionally, 3D printing enables rapid prototyping, allowing designers to iterate and refine their products quickly. This accelerates the product development cycle and reduces time-to-market. In the construction industry, 3D printing materials are used to create building components, architectural models, and even entire structures. Concrete and other construction materials can be 3D printed to produce complex shapes and designs that are difficult to achieve with traditional methods. This technology offers the potential for faster, more cost-effective construction processes, reducing labor and material costs. Additionally, 3D printing allows for the creation of sustainable and energy-efficient building designs, contributing to the industry's efforts to reduce its environmental impact. Other industries, such as electronics, education, and food, also utilize 3D printing materials for various applications. In electronics, 3D printing is used to produce custom enclosures, circuit boards, and components with intricate designs. Educational institutions use 3D printing to enhance learning experiences, allowing students to create physical models and prototypes. In the food industry, 3D printing materials are used to create intricate and customized food items, offering new possibilities for culinary creativity and presentation. Overall, the Global Industrial 3D Printing Materials Market plays a vital role in enabling innovation and efficiency across a wide range of industries. The ability to produce customized, high-quality parts and products with reduced lead times and costs makes 3D printing an attractive option for manufacturers and businesses. As the technology continues to evolve and new materials are developed, the applications and benefits of 3D printing are expected to expand further, driving growth and transformation in various sectors.

Global Industrial 3D Printing Materials Market Outlook:

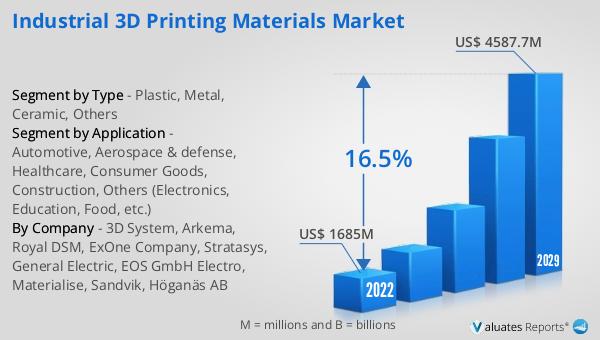

The global Industrial 3D Printing Materials market, valued at US$ 1685 million in 2023, is projected to reach US$ 4587.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 16.5% during the forecast period from 2024 to 2030. This significant growth underscores the increasing adoption of 3D printing technologies across various industries, driven by the need for efficient, cost-effective, and customizable manufacturing solutions. The market's expansion is fueled by continuous advancements in material science, leading to the development of new and improved 3D printing materials that enhance performance and broaden application possibilities. As industries such as automotive, aerospace, healthcare, consumer goods, and construction increasingly integrate 3D printing into their operations, the demand for high-quality materials is expected to rise. This growth trajectory highlights the transformative potential of 3D printing technologies in revolutionizing traditional manufacturing processes and driving innovation across multiple sectors. The market's robust growth prospects are indicative of the ongoing shift towards additive manufacturing and the increasing recognition of its benefits in terms of efficiency, precision, and sustainability.

| Report Metric | Details |

| Report Name | Industrial 3D Printing Materials Market |

| Accounted market size in 2023 | US$ 1685 million |

| Forecasted market size in 2030 | US$ 4587.7 million |

| CAGR | 16.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | 3D System, Arkema, Royal DSM, ExOne Company, Stratasys, General Electric, EOS GmbH Electro, Materialise, Sandvik, Höganäs AB |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |