What is Global Heat Recovery Device Market?

The global Heat Recovery Device market is a rapidly evolving sector that focuses on the development and deployment of technologies designed to capture and reuse waste heat from various industrial processes. These devices are essential for improving energy efficiency and reducing greenhouse gas emissions. By recovering heat that would otherwise be lost, these systems can significantly lower energy costs and enhance the overall sustainability of industrial operations. The market encompasses a wide range of products, including heat exchangers, recuperators, regenerators, and economizers, each tailored to specific applications and industries. The growing emphasis on energy conservation and environmental protection is driving the demand for heat recovery devices across the globe. Industries such as manufacturing, power generation, and chemical processing are increasingly adopting these technologies to optimize their energy use and comply with stringent environmental regulations. As a result, the global Heat Recovery Device market is poised for substantial growth, driven by technological advancements and the rising need for energy-efficient solutions.

Vertical, Horizontal in the Global Heat Recovery Device Market:

In the context of the Global Heat Recovery Device Market, vertical and horizontal classifications refer to the orientation and application of heat recovery systems. Vertical heat recovery devices are typically designed for applications where space is limited, and the system needs to be installed in a vertical configuration. These devices are often used in high-rise buildings, industrial plants, and other settings where floor space is at a premium. Vertical systems are advantageous because they can be integrated into existing infrastructure without requiring significant modifications. They are also easier to maintain and service, as their components are more accessible. On the other hand, horizontal heat recovery devices are designed for applications where there is ample horizontal space for installation. These systems are commonly used in large industrial facilities, commercial buildings, and residential complexes. Horizontal systems are often more efficient than their vertical counterparts because they can accommodate larger heat exchangers and other components, leading to better heat transfer and energy recovery. Additionally, horizontal systems can be more cost-effective to install and operate, as they typically require fewer structural modifications and can be integrated into existing HVAC systems with minimal disruption. Both vertical and horizontal heat recovery devices play a crucial role in enhancing energy efficiency and reducing operational costs across various sectors. The choice between vertical and horizontal systems depends on several factors, including the available space, the specific application, and the desired level of energy recovery. In many cases, a combination of both vertical and horizontal systems may be used to achieve optimal results. For example, a high-rise building might use vertical heat recovery devices for its HVAC system, while also employing horizontal systems for its industrial processes. This integrated approach can maximize energy savings and improve overall system performance. Furthermore, advancements in technology are continually improving the efficiency and versatility of both vertical and horizontal heat recovery devices. Innovations such as advanced heat exchangers, smart controls, and modular designs are making these systems more adaptable and effective in a wider range of applications. As a result, the global Heat Recovery Device market is seeing increased adoption of both vertical and horizontal systems, driven by the need for more sustainable and cost-effective energy solutions. In conclusion, the vertical and horizontal classifications in the Global Heat Recovery Device Market represent two distinct approaches to heat recovery, each with its own set of advantages and applications. By understanding the unique benefits and limitations of each type, businesses and industries can make informed decisions about which systems are best suited to their needs. Whether used individually or in combination, vertical and horizontal heat recovery devices are essential tools for improving energy efficiency and reducing environmental impact in today's increasingly energy-conscious world.

Residential Building, Commercial Building, Industrial Building in the Global Heat Recovery Device Market:

The usage of heat recovery devices in residential, commercial, and industrial buildings varies significantly, reflecting the unique energy needs and operational characteristics of each sector. In residential buildings, heat recovery devices are primarily used to improve the efficiency of heating, ventilation, and air conditioning (HVAC) systems. These devices capture waste heat from exhaust air and use it to preheat incoming fresh air, thereby reducing the energy required to maintain comfortable indoor temperatures. This not only lowers energy bills for homeowners but also enhances indoor air quality by ensuring a constant supply of fresh, filtered air. In commercial buildings, heat recovery devices are employed to optimize the performance of HVAC systems, as well as other energy-intensive processes such as water heating and refrigeration. For example, in office buildings, hotels, and shopping centers, heat recovery systems can capture waste heat from air conditioning units and use it to preheat water for domestic use or space heating. This can lead to significant energy savings and lower operating costs, making commercial buildings more sustainable and cost-effective to operate. Additionally, heat recovery devices can help commercial buildings comply with increasingly stringent energy efficiency standards and regulations. In industrial buildings, the application of heat recovery devices is even more diverse and critical. Industrial processes often generate large amounts of waste heat, which, if not recovered, represents a significant loss of energy and resources. Heat recovery devices in industrial settings can capture this waste heat and reuse it in various ways, such as preheating combustion air for boilers, generating steam for process heating, or producing electricity through waste heat recovery systems. This not only improves the overall energy efficiency of industrial operations but also reduces greenhouse gas emissions and lowers fuel consumption. Industries such as manufacturing, chemical processing, and power generation are particularly well-suited to benefit from heat recovery technologies, given their high energy demands and the potential for substantial energy savings. Moreover, the integration of heat recovery devices in industrial buildings can enhance the reliability and resilience of energy systems. By reducing dependence on external energy sources and improving the efficiency of internal processes, heat recovery systems can help industrial facilities maintain continuous operations even in the face of energy supply disruptions or price fluctuations. This is especially important for industries that require a stable and reliable energy supply to maintain production and ensure product quality. In conclusion, the usage of heat recovery devices in residential, commercial, and industrial buildings plays a vital role in enhancing energy efficiency, reducing operational costs, and minimizing environmental impact. By capturing and reusing waste heat, these devices help to optimize the performance of HVAC systems, water heating, and industrial processes, leading to significant energy savings and improved sustainability. As the demand for energy-efficient solutions continues to grow, the adoption of heat recovery devices across all building types is expected to increase, driven by the need for more sustainable and cost-effective energy management practices.

Global Heat Recovery Device Market Outlook:

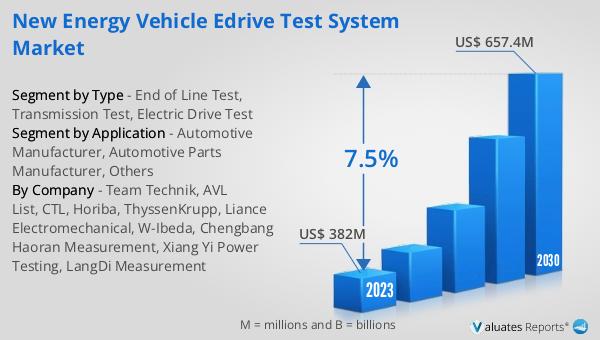

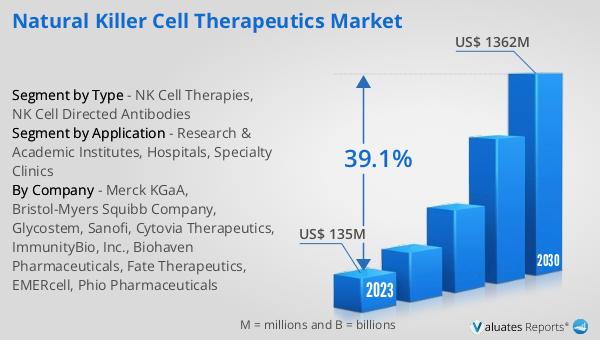

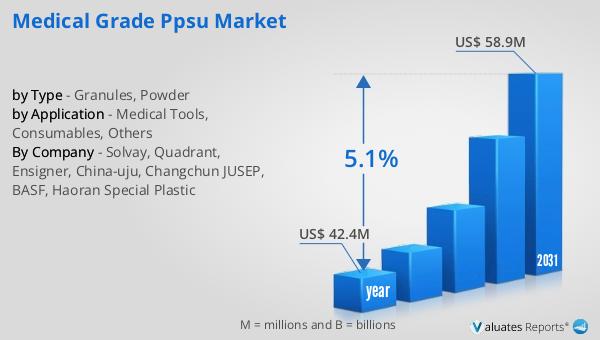

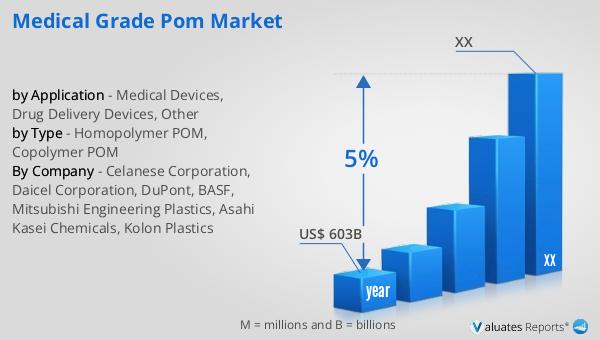

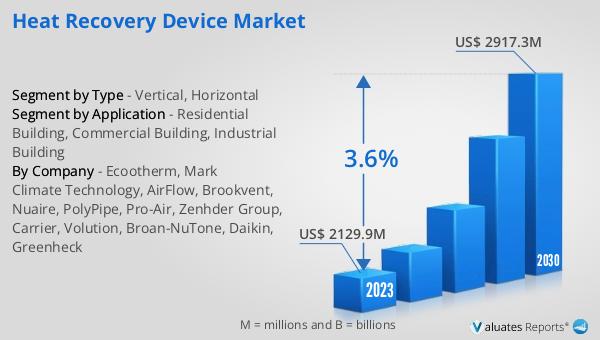

The global Heat Recovery Device market was valued at US$ 2129.9 million in 2023 and is projected to reach US$ 2917.3 million by 2030, experiencing a compound annual growth rate (CAGR) of 3.6% during the forecast period from 2024 to 2030. According to our "Construction Machinery" research center, sales of construction machinery in Europe saw a 24% increase in 2021. In 2022, the revenue from construction machinery in Europe was approximately US$ 22 billion, while the U.S. market recorded sales of about US$ 36 billion in construction machinery for the same year.

| Report Metric | Details |

| Report Name | Heat Recovery Device Market |

| Accounted market size in 2023 | US$ 2129.9 million |

| Forecasted market size in 2030 | US$ 2917.3 million |

| CAGR | 3.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Ecootherm, Mark Climate Technology, AirFlow, Brookvent, Nuaire, PolyPipe, Pro-Air, Zenhder Group, Carrier, Volution, Broan-NuTone, Daikin, Greenheck |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |