What is Global Vehicle Grade LiDAR Scanner Market?

The Global Vehicle Grade LiDAR Scanner Market refers to the worldwide industry focused on the development, production, and application of LiDAR (Light Detection and Ranging) technology specifically designed for vehicles. LiDAR scanners use laser beams to create high-resolution 3D maps of the environment, which are crucial for the functioning of autonomous vehicles and advanced driver-assistance systems (ADAS). These scanners help in detecting obstacles, measuring distances, and identifying objects around the vehicle, thereby enhancing safety and navigation. The market encompasses various stakeholders, including manufacturers, suppliers, and end-users, who are involved in the production and utilization of these advanced sensors. The increasing demand for autonomous driving technology and the need for improved vehicle safety are driving the growth of this market. Additionally, advancements in LiDAR technology, such as the development of solid-state LiDAR, are contributing to the market's expansion. The global vehicle grade LiDAR scanner market is characterized by rapid technological advancements, strategic partnerships, and significant investments in research and development.

Mechanical Lidar, Solid State Lidar in the Global Vehicle Grade LiDAR Scanner Market:

Mechanical LiDAR and Solid-State LiDAR are two primary types of LiDAR technologies used in the Global Vehicle Grade LiDAR Scanner Market. Mechanical LiDAR systems use rotating mirrors or other mechanical means to direct laser beams across the environment. These systems are known for their high resolution and wide field of view, making them suitable for applications requiring detailed environmental mapping. However, mechanical LiDAR systems are often bulky, expensive, and have moving parts that can wear out over time, leading to potential reliability issues. On the other hand, Solid-State LiDAR systems use electronic means to steer the laser beams, eliminating the need for moving parts. This makes them more compact, robust, and potentially cheaper to produce. Solid-State LiDAR systems can be further categorized into different types, such as MEMS (Micro-Electro-Mechanical Systems) LiDAR, Flash LiDAR, and Optical Phased Array (OPA) LiDAR. MEMS LiDAR uses tiny mirrors to direct the laser beams, offering a balance between performance and cost. Flash LiDAR illuminates the entire scene with a single laser pulse, capturing a 3D image in one go, which is ideal for high-speed applications. OPA LiDAR uses an array of tiny antennas to steer the laser beams electronically, providing high precision and reliability. Both Mechanical and Solid-State LiDAR systems have their advantages and limitations, and the choice between them depends on the specific requirements of the application. For instance, Mechanical LiDAR might be preferred for applications needing high resolution and wide coverage, while Solid-State LiDAR might be chosen for its compactness and durability. The ongoing advancements in LiDAR technology are aimed at improving performance, reducing costs, and enhancing the integration of these systems into vehicles. As the demand for autonomous vehicles and advanced driver-assistance systems continues to grow, both Mechanical and Solid-State LiDAR technologies are expected to play a crucial role in shaping the future of the Global Vehicle Grade LiDAR Scanner Market.

OEM, Research in the Global Vehicle Grade LiDAR Scanner Market:

The usage of Global Vehicle Grade LiDAR Scanner Market in Original Equipment Manufacturer (OEM) and Research sectors is significant and multifaceted. In the OEM sector, LiDAR scanners are integrated into vehicles during the manufacturing process to enhance safety features and enable autonomous driving capabilities. OEMs use LiDAR technology to develop advanced driver-assistance systems (ADAS) that can detect obstacles, pedestrians, and other vehicles, thereby preventing accidents and improving overall road safety. LiDAR scanners provide high-resolution 3D maps of the vehicle's surroundings, allowing for precise navigation and real-time decision-making. This technology is crucial for the development of self-driving cars, as it enables the vehicle to perceive and understand its environment accurately. OEMs are investing heavily in LiDAR technology to stay competitive in the rapidly evolving automotive industry and to meet the growing demand for safer and more autonomous vehicles. In the Research sector, LiDAR scanners are used extensively for various applications, including environmental monitoring, urban planning, and infrastructure development. Researchers use LiDAR technology to create detailed topographic maps, study vegetation and forest structures, and monitor changes in the environment over time. In the context of vehicle grade LiDAR, researchers focus on improving the technology's performance, reliability, and cost-effectiveness. They conduct experiments and simulations to test new LiDAR designs, algorithms, and integration methods. Research institutions and universities collaborate with OEMs and LiDAR manufacturers to develop innovative solutions that can be applied in real-world scenarios. The insights gained from research activities help in advancing the technology and addressing the challenges associated with its implementation in vehicles. Overall, the usage of Global Vehicle Grade LiDAR Scanner Market in OEM and Research sectors is driving innovation and contributing to the development of safer, more efficient, and autonomous transportation systems.

Global Vehicle Grade LiDAR Scanner Market Outlook:

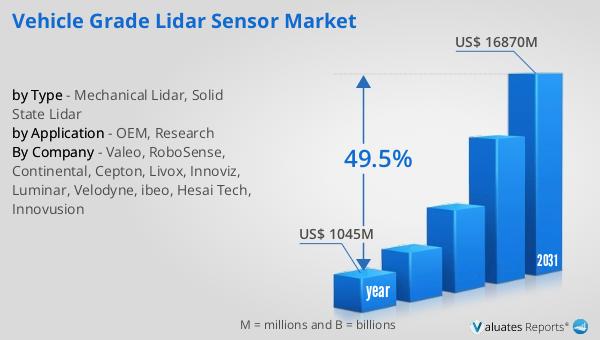

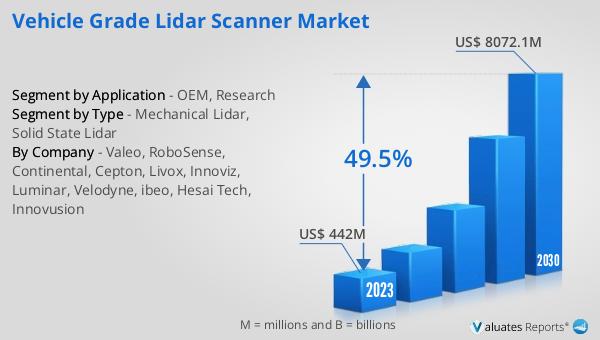

The global Vehicle Grade LiDAR Scanner market was valued at US$ 442 million in 2023 and is anticipated to reach US$ 8072.1 million by 2030, witnessing a CAGR of 49.5% during the forecast period 2024-2030. This remarkable growth is driven by the increasing demand for autonomous vehicles and advanced driver-assistance systems (ADAS) that rely on LiDAR technology for accurate environmental mapping and obstacle detection. The market's expansion is also fueled by continuous advancements in LiDAR technology, such as the development of solid-state LiDAR, which offers improved performance, compactness, and cost-effectiveness compared to traditional mechanical LiDAR systems. Additionally, strategic partnerships, significant investments in research and development, and the growing adoption of LiDAR technology by OEMs and research institutions are contributing to the market's rapid growth. As the automotive industry continues to evolve towards greater automation and safety, the Global Vehicle Grade LiDAR Scanner Market is expected to play a crucial role in shaping the future of transportation.

| Report Metric | Details |

| Report Name | Vehicle Grade LiDAR Scanner Market |

| Accounted market size in 2023 | US$ 442 million |

| Forecasted market size in 2030 | US$ 8072.1 million |

| CAGR | 49.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Valeo, RoboSense, Continental, Cepton, Livox, Innoviz, Luminar, Velodyne, ibeo, Hesai Tech, Innovusion |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |