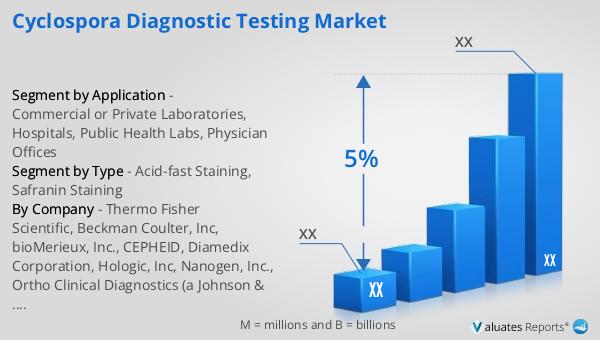

What is Global Cyclospora Diagnostic Testing Market?

The Global Cyclospora Diagnostic Testing Market is a specialized segment within the broader diagnostic testing industry, focusing on the detection and identification of Cyclospora, a protozoan parasite that causes cyclosporiasis. This market encompasses various diagnostic methods and technologies used to identify the presence of Cyclospora in human samples, primarily stool specimens. The importance of this market is underscored by the need for accurate and timely diagnosis of cyclosporiasis, which can lead to severe gastrointestinal illness if left untreated. The market includes a range of products and services, from traditional microscopy techniques to advanced molecular diagnostics, catering to different healthcare settings such as hospitals, public health labs, and private laboratories. The growth of this market is driven by factors such as increasing awareness of foodborne illnesses, advancements in diagnostic technologies, and the rising incidence of Cyclospora infections globally. As a result, the Global Cyclospora Diagnostic Testing Market plays a crucial role in public health by enabling effective disease management and control.

Acid-fast Staining, Safranin Staining in the Global Cyclospora Diagnostic Testing Market:

Acid-fast staining and safranin staining are two critical techniques used in the Global Cyclospora Diagnostic Testing Market to identify Cyclospora oocysts in clinical samples. Acid-fast staining, specifically the modified Ziehl-Neelsen stain, is a widely used method due to its ability to differentiate Cyclospora oocysts from other similar organisms. This technique involves staining the sample with a primary stain, such as carbol fuchsin, which binds to the waxy cell wall of the oocysts. The sample is then decolorized with an acid-alcohol solution, which removes the stain from non-acid-fast organisms, leaving the Cyclospora oocysts stained red. A counterstain, typically methylene blue, is then applied to provide a contrasting background, making the oocysts easily identifiable under a microscope. Safranin staining, on the other hand, is used as a counterstain in some staining protocols to enhance the visibility of Cyclospora oocysts. Safranin is a basic dye that stains the oocysts a reddish-orange color, providing a clear contrast against the background. This technique is particularly useful in differentiating Cyclospora from other coccidian parasites, such as Cryptosporidium and Isospora, which may appear similar under a microscope. Both acid-fast staining and safranin staining are essential tools in the diagnostic arsenal for Cyclospora, enabling accurate and reliable identification of the parasite in clinical samples. These staining techniques are complemented by other diagnostic methods, such as molecular assays and immunoassays, which provide additional layers of specificity and sensitivity in detecting Cyclospora infections. The integration of these diagnostic techniques into routine laboratory workflows ensures that healthcare providers can quickly and accurately diagnose cyclosporiasis, leading to timely treatment and improved patient outcomes.

Commercial or Private Laboratories, Hospitals, Public Health Labs, Physician Offices in the Global Cyclospora Diagnostic Testing Market:

The Global Cyclospora Diagnostic Testing Market finds extensive usage across various healthcare settings, including commercial or private laboratories, hospitals, public health labs, and physician offices. In commercial or private laboratories, advanced diagnostic technologies such as molecular assays and immunoassays are commonly employed to detect Cyclospora oocysts with high sensitivity and specificity. These laboratories often serve as reference centers, providing specialized testing services that may not be available in smaller healthcare facilities. The use of automated systems and high-throughput platforms in these laboratories ensures rapid turnaround times and accurate results, which are critical for effective disease management. Hospitals, on the other hand, rely on a combination of traditional microscopy techniques and modern molecular diagnostics to identify Cyclospora infections. Hospital laboratories play a crucial role in the initial diagnosis and management of cyclosporiasis, particularly in acute care settings where timely diagnosis is essential for patient care. Public health labs are instrumental in monitoring and controlling the spread of Cyclospora infections at the community level. These labs conduct surveillance testing, outbreak investigations, and epidemiological studies to track the incidence and distribution of cyclosporiasis. By providing accurate and timely diagnostic data, public health labs support efforts to implement effective public health interventions and prevent the spread of the disease. Physician offices also utilize Cyclospora diagnostic testing, particularly in cases where patients present with symptoms of gastrointestinal illness. Point-of-care testing and rapid diagnostic kits are increasingly being used in these settings to provide immediate results, enabling physicians to make informed decisions about patient management and treatment. The availability of Cyclospora diagnostic testing across these diverse healthcare settings ensures comprehensive coverage and accessibility, facilitating early detection and prompt treatment of cyclosporiasis.

Global Cyclospora Diagnostic Testing Market Outlook:

The global pharmaceutical market was valued at 1475 billion USD in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 5% over the next six years. In comparison, the chemical drug market has shown a steady increase, rising from 1005 billion USD in 2018 to an estimated 1094 billion USD in 2022. This growth reflects the ongoing demand for pharmaceutical products and the continuous advancements in drug development and manufacturing. The pharmaceutical market encompasses a wide range of products, including prescription medications, over-the-counter drugs, and biologics, catering to various therapeutic areas such as oncology, cardiology, and infectious diseases. The chemical drug market, a significant subset of the broader pharmaceutical market, focuses on the development and production of small-molecule drugs, which are typically synthesized through chemical processes. The steady growth in the chemical drug market highlights the sustained demand for these traditional pharmaceuticals, even as the industry increasingly embraces biologics and other advanced therapies. The robust growth in both the global pharmaceutical market and the chemical drug market underscores the critical role of pharmaceuticals in healthcare and the ongoing efforts to address unmet medical needs through innovative drug development.

| Report Metric | Details |

| Report Name | Cyclospora Diagnostic Testing Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Thermo Fisher Scientific, Beckman Coulter, Inc, bioMerieux, Inc., CEPHEID, Diamedix Corporation, Hologic, Inc, Nanogen, Inc., Ortho Clinical Diagnostics (a Johnson & Johnson company), DiaSorin S.p.A., Roche Diagnostics (a division of Hoffmann-La Roche), Siemens Healthcare, QIAGEN N.V., Wako Chemicals USA, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |