What is Global Electric Nutrunner Market?

The Global Electric Nutrunner Market refers to the worldwide industry focused on the production, distribution, and utilization of electric nutrunners. These are specialized tools used for tightening or loosening nuts and bolts with precision and efficiency. Electric nutrunners are preferred over traditional manual tools due to their ability to provide consistent torque, reduce operator fatigue, and enhance productivity. They are widely used in various industries such as automotive, aerospace, machinery manufacturing, and construction. The market encompasses a range of products, including handheld and fixtured electric nutrunners, each designed to meet specific application requirements. The growth of this market is driven by the increasing demand for automation in manufacturing processes, the need for high precision in assembly operations, and the rising adoption of electric tools over pneumatic ones due to their environmental benefits and ease of use.

Handheld Electric Nutrunner, Fixtured Electric Nutrunner in the Global Electric Nutrunner Market:

Handheld electric nutrunners are portable tools that are easy to maneuver and are commonly used in applications where flexibility and mobility are crucial. These tools are ideal for tasks that require the operator to move around or reach tight spaces. Handheld electric nutrunners are equipped with ergonomic designs to reduce operator fatigue and improve efficiency. They are widely used in the automotive industry for assembling vehicle components, in machinery manufacturing for assembling parts, and in various other industries where precision and mobility are essential. On the other hand, fixtured electric nutrunners are stationary tools that are mounted on a fixture or a robotic arm. These tools are used in applications that require high precision and repeatability. Fixtured electric nutrunners are commonly used in automated assembly lines where consistent torque and speed are critical. They are ideal for high-volume production environments where the same task needs to be repeated multiple times with high accuracy. The use of fixtured electric nutrunners helps in reducing human error, increasing production speed, and ensuring consistent quality. Both handheld and fixtured electric nutrunners play a crucial role in the global electric nutrunner market, catering to different needs and applications across various industries.

Automotive, Transportation, Machinery Manufacturing, Others in the Global Electric Nutrunner Market:

The global electric nutrunner market finds extensive usage in several key areas, including automotive, transportation, machinery manufacturing, and others. In the automotive industry, electric nutrunners are essential for assembling various components of vehicles, such as engines, transmissions, and chassis. They ensure that each part is tightened to the correct torque, which is crucial for the safety and performance of the vehicle. In the transportation sector, electric nutrunners are used for assembling and maintaining transportation equipment, such as trains, buses, and airplanes. They help in ensuring that all components are securely fastened, which is vital for the safety and reliability of the transportation systems. In machinery manufacturing, electric nutrunners are used for assembling different types of machinery and equipment. They provide the precision and consistency needed to ensure that each part is correctly assembled, which is essential for the proper functioning of the machinery. Other industries that use electric nutrunners include construction, aerospace, and electronics, where precision and efficiency are critical. The versatility and efficiency of electric nutrunners make them an indispensable tool in various industries, contributing to the growth and development of the global electric nutrunner market.

Global Electric Nutrunner Market Outlook:

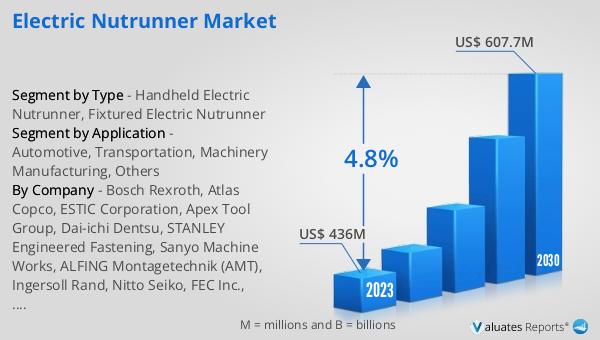

The global electric nutrunner market is anticipated to grow significantly, reaching an estimated value of US$ 607.7 million by 2030, up from US$ 458.7 million in 2024, with a compound annual growth rate (CAGR) of 4.8% during the period from 2024 to 2030. Europe currently holds the largest share of the market, accounting for approximately 43%, followed by North America, which represents about 24% of the market share. The top three companies in the market collectively occupy around 40% of the market share. This growth is driven by the increasing demand for automation and precision in various industries, as well as the advantages offered by electric nutrunners over traditional tools. The market is expected to continue expanding as more industries adopt electric nutrunners for their assembly and manufacturing processes.

| Report Metric | Details |

| Report Name | Electric Nutrunner Market |

| Accounted market size in 2024 | an estimated US$ 458.7 million |

| Forecasted market size in 2030 | US$ 607.7 million |

| CAGR | 4.8% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Bosch Rexroth, Atlas Copco, ESTIC Corporation, Apex Tool Group, Dai-ichi Dentsu, STANLEY Engineered Fastening, Sanyo Machine Works, ALFING Montagetechnik (AMT), Ingersoll Rand, Nitto Seiko, FEC Inc., Maschinenfabrik Wagner, Tone, HYTORC, AIMCO, Desoutter Industrial Tools, CORETEC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |