What is Global Specialty Graphite Market?

The Global Specialty Graphite Market is a niche segment within the broader graphite industry, focusing on high-performance graphite materials used in various advanced applications. Specialty graphite is known for its exceptional properties, such as high thermal and electrical conductivity, resistance to thermal shock, and chemical inertness. These characteristics make it indispensable in industries that require materials capable of withstanding extreme conditions. The market encompasses a range of products, including extruded graphite, molded graphite, and isotropic graphite, each tailored to specific industrial needs. The demand for specialty graphite is driven by its critical role in cutting-edge technologies and manufacturing processes, such as those found in the photovoltaic, semiconductor, and metallurgy industries. As industries continue to innovate and seek materials that offer superior performance, the global specialty graphite market is poised for sustained growth. This market is characterized by a high level of competition, with key players investing heavily in research and development to enhance the quality and performance of their graphite products.

Extruded Graphite, Molded Graphite, Isotropic Graphite in the Global Specialty Graphite Market:

Extruded graphite, molded graphite, and isotropic graphite are three primary types of specialty graphite, each with unique properties and applications. Extruded graphite is produced by forcing a mixture of graphite powder and binder through a die to create a specific shape. This type of graphite is known for its excellent machinability and is commonly used in applications where complex shapes and high precision are required, such as in the production of electrodes for electrical discharge machining (EDM) and in the manufacturing of various components for the semiconductor industry. Molded graphite, on the other hand, is created by compressing graphite powder into a mold under high pressure. This process results in a material with high density and strength, making it suitable for applications that demand durability and resistance to wear, such as in the foundry and metallurgy fields. Molded graphite is often used to produce crucibles, molds, and other components that must withstand high temperatures and harsh conditions. Isotropic graphite is a type of specialty graphite that is characterized by its uniform properties in all directions. This is achieved through a meticulous manufacturing process that involves the use of fine-grain graphite powder and isostatic pressing. Isotropic graphite is highly valued for its superior thermal and electrical conductivity, as well as its resistance to thermal shock and chemical corrosion. These properties make it ideal for use in the photovoltaic industry, where it is used to produce components for solar cells, and in the semiconductor industry, where it is used in the production of wafers and other critical components. Additionally, isotropic graphite is used in the aerospace industry for its lightweight and high-strength properties, as well as in the nuclear industry for its ability to withstand extreme conditions. Overall, the global specialty graphite market is driven by the diverse applications and unique properties of extruded, molded, and isotropic graphite, each of which plays a crucial role in advancing technology and industrial processes.

Photovoltaic Industry, Semiconductor Industry, Electrical Discharge Machining, Foundry & Metallurgy Field, Others in the Global Specialty Graphite Market:

The global specialty graphite market finds extensive usage across various industries, including the photovoltaic industry, semiconductor industry, electrical discharge machining (EDM), foundry and metallurgy field, and others. In the photovoltaic industry, specialty graphite is essential for the production of solar cells. Its high thermal conductivity and resistance to thermal shock make it ideal for use in the manufacturing of silicon wafers, which are the building blocks of solar panels. Graphite components are used in the crystal growth process, where they help in the formation of high-purity silicon crystals. In the semiconductor industry, specialty graphite is used in the production of wafers and other critical components. Its excellent electrical conductivity and resistance to high temperatures make it suitable for use in the manufacturing of semiconductors, which are essential for electronic devices. Graphite is used in various stages of semiconductor production, including the growth of silicon crystals, wafer processing, and the fabrication of electronic components. In the field of electrical discharge machining (EDM), specialty graphite is used to produce electrodes that are used to shape and machine hard materials. Graphite electrodes are preferred in EDM due to their high machinability, electrical conductivity, and resistance to wear. They enable precise and efficient machining of complex shapes and are widely used in the aerospace, automotive, and tool and die industries. In the foundry and metallurgy field, specialty graphite is used to produce crucibles, molds, and other components that must withstand high temperatures and harsh conditions. Its high thermal conductivity and resistance to thermal shock make it ideal for use in metal casting and refining processes. Graphite components are used in the production of high-quality metal products, including steel, aluminum, and other alloys. Additionally, specialty graphite finds applications in other industries, such as the aerospace and nuclear industries, where its unique properties are leveraged for advanced applications. In the aerospace industry, graphite is used for its lightweight and high-strength properties, while in the nuclear industry, it is used for its ability to withstand extreme conditions. Overall, the global specialty graphite market plays a crucial role in advancing technology and industrial processes across a wide range of industries.

Global Specialty Graphite Market Outlook:

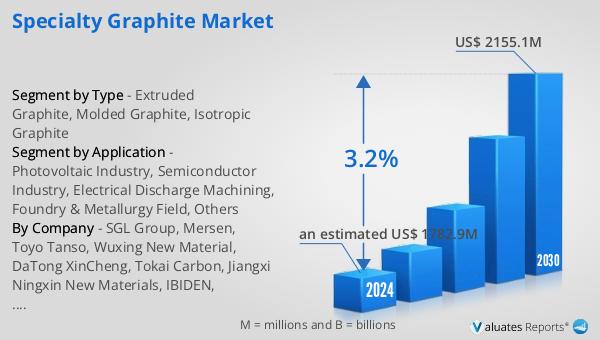

The global specialty graphite market is anticipated to grow from an estimated US$ 1782.9 million in 2024 to US$ 2155.1 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.2% during the period from 2024 to 2030. The market is highly competitive, with the top five players collectively holding over 50% of the market share. The Asia Pacific region dominates the market, accounting for approximately 70% of the total share, followed by North America and Europe, which hold shares of 20% and 10%, respectively. Among the various product types, isotropic graphite stands out as the largest segment, representing about 75% of the market share. This dominance is attributed to its superior properties, such as uniformity in all directions, high thermal and electrical conductivity, and resistance to thermal shock and chemical corrosion. These characteristics make isotropic graphite highly sought after in industries such as photovoltaics, semiconductors, and aerospace, where high performance and reliability are critical. The market's growth is driven by the increasing demand for advanced materials in various high-tech applications, as well as ongoing investments in research and development to enhance the quality and performance of specialty graphite products.

| Report Metric | Details |

| Report Name | Specialty Graphite Market |

| Accounted market size in 2024 | an estimated US$ 1782.9 million |

| Forecasted market size in 2030 | US$ 2155.1 million |

| CAGR | 3.2% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | SGL Group, Mersen, Toyo Tanso, Wuxing New Material, DaTong XinCheng, Tokai Carbon, Jiangxi Ningxin New Materials, IBIDEN, Pingdingshan Oriental Carbon, Nippon Carbon, Fangda Carbon, Pingdingshan Boxiang Carbon, Sinosteel, Dahua Glory Special Graphite, Graphite India Ltd, Entegris, Kaiyuan Special Graphite, Zhongnan Diamond, SEC Carbon, Qingdao Tennry Carbon, Morgan, GrafTech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |